Automotive Water Pump Market: Strategic Imperatives for 2026

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present a synthesis of our latest Automotive Water Pump Market study — a forward-looking, practitioner-focused briefing designed to inform executive decision-making throughout 2026. This article highlights the research’s strategic value while intentionally preserving the granular segmentation and proprietary datapoints that reside in the full report. Think of this as the trailer: enough insight to shape immediate choices, and a clear invitation to obtain the full intelligence package for implementation-ready detail.

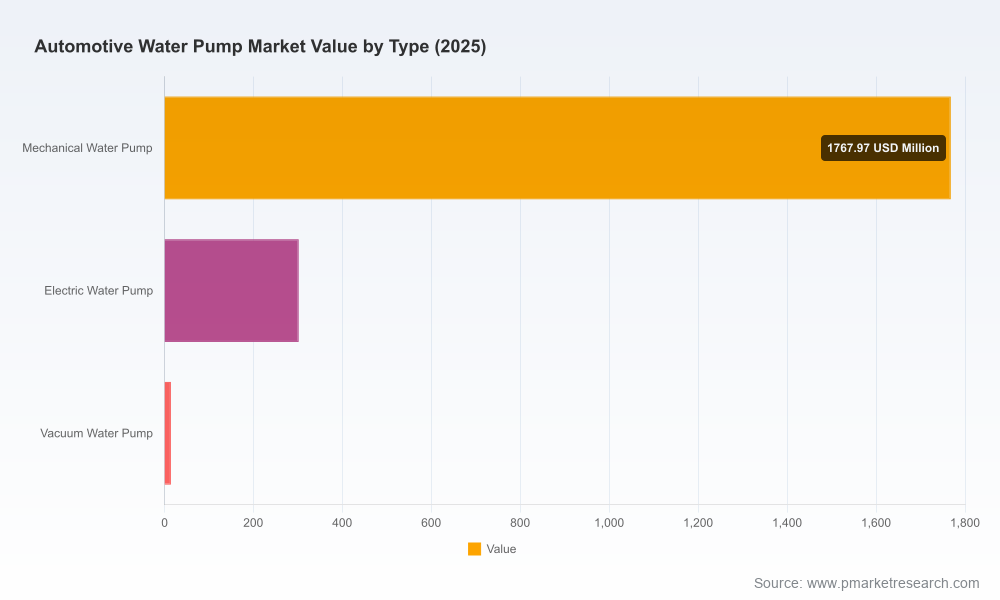

Automotive Water Pump Market

Market trajectory at a glance

The automotive water pump market has moved beyond simple replacement cycles and is now a bellwether for broader powertrain thermal-management trends. On an aggregate basis, the market expanded meaningfully over the early 2020s, rising from the low‑billion range in 2020 to an established base year in 2025. Our modelling shows continued expansion through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 5.3%, with the market approaching the high‑end of its current decade potential by 2032.

Automotive Water Pump Market

That mid-single-digit CAGR masks structural shifts that matter to strategy teams: electrification and hybridization of powertrains, increasing complexity in thermal management control (including ECU-driven electric water pumps), aftermarket dynamics driven by vehicle parc growth in mature markets, and persistent demand in commercial and off‑highway segments. These forces combine to create distinct windows of opportunity for product innovation, aftermarket positioning, and supply‑chain optimization.

Automotive Water Pump Market

Dynamics shaping 2026 decisions

- Thermal-management complexity: Electric and switchable pumps are no longer optional R&D projects — they are core components of electrified powertrains. Requirements for ECU activation, variable speed control, and precise coolant flow are shaping product roadmaps and test protocols.

- Quality and testing expectations: OEM and aftermarket standards increasingly mandate 100% functional and leakage testing for premium alloy components and seals. This raises capital intensity for suppliers that aim to serve late‑model and hybrid vehicle segments.

- Regulatory and certification shifts: Changes to certifications for personnel working on water‑based systems (notably updates to ASSE qualification paths) affect service networks, warranty execution, and aftermarket installation economics.

- Materials and supply volatility: Premium alloys that improve durability in high‑temperature environments require rigorous supplier qualification and testing. Sourcing strategies must balance cost, availability, and traceability.

- Workforce and installer competency: Evolving standards for professional installers require investment in training, certification programs, and standardized repair kits to reduce warranty exposure and speed repair throughput.

Strategic implications by corporate role

- OEMs: Integrate thermal‑management modules earlier in powertrain design cycles. Specify test protocols that reduce end‑of‑line failures and harmonize interfaces for third‑party serviceability to control lifecycle costs.

- Tier‑1 suppliers: Prioritize modular architectures that can be configured for mechanical, electric, and hybrid applications. Invest selectively in 100% testing capability and digital traceability to meet OEM expectations.

- Aftermarket players: Differentiate on coverage and reliability assurances by certifying installers and offering bundled kits. Consider hybrid go‑to‑market models that blend direct online channels with professional distribution.

- Investors and M&A teams: Look for targets that combine testing capabilities, ECU expertise for electric pumps, and durable supplier relationships; synergies in quality assurance and aftermarket reach are high‑value levers.

Competitive landscape — what to watch in 2026

The market exhibits moderate concentration among established suppliers, with leading firms maintaining meaningful positions while room remains for niche specialists and regional champions. Below I summarize the strategic positioning of key market participants and the implications for competitors and partners.

- Gates Corporation (Indianapolis, USA): Known for premium alloy pumps and rigorous 100% functional/leakage testing, Gates is positioned to serve late‑model, hybrid and vintage vehicle segments where reliability and provenance command a premium. Its testing standards set a quality bar that drives supplier qualification across the value chain.

- Carter Fuel Systems (Grand Rapids, USA): Carter’s engineered pumps emphasize OEM‑level performance and aftermarket reliability. Their strength is broad vehicle coverage and reliability messaging — an attractive profile for distributors and multi‑brand service networks.

- US Motor Works (Santa Fe Springs, USA): Focused on heavy‑duty, professional‑series pumps for commercial applications, with ISO 9001:2015 manufacturing credentials. Their updated catalogs reflect a continued commitment to commercial‑vehicle programs where certification and parts depth matter most.

- Aisin Corporation (Nagakute, Japan): Aisin remains a dominant OE supplier with deep expertise in aluminum die‑cast pump production and a clear push into electric pump technology for EV thermal management. Their presence in OEM programs makes them a partner of choice for automakers looking for integrated systems.

- Continental AG (Hannover, Germany): Offering standalone pumps and modular kits for thermal management, Continental is balancing cost‑effective repair options with advanced variants — a dual track that targets both aftermarket and OEM service segments.

- Setco Automotive (Pune, India): A rising regional supplier expanding its thermal‑management portfolio. Recent product launches indicate ambition to capture passenger and light commercial vehicle opportunities in high‑growth markets.

- Valéo S.A. (Paris, France): Provides integrated electric and mechanical pumps for diverse vehicle categories, underscoring a platform approach that supports OEMs’ electrification roadmaps.

- SKF Group (Gothenburg, Sweden) and Bosch GmbH (Gerlingen, Germany): Both bring precision engineering and strong aftermarket catalogues; Bosch’s move into switchable and control‑unit integrated variants is particularly relevant for modern engine systems.

- Padmini VNA Mechatronics (Pune, India): Focused on electric water pumps for EVs and partnerships with local OEMs, representing a case study in adapting domestic manufacturing strengths to global EV trends.

Recent product activity underscores the strategic pivots in the industry: product launches expanding portfolios, AR demonstrations at trade shows emphasizing digital customer engagement, and catalog updates for heavy‑duty applications. These events demonstrate that incumbents are scaling both product breadth and digital touchpoints to capture aftermarket and OEM demand.

What the full PW Consulting report delivers (operational, actionable)

- Market sizing and forward‑looking forecasts (historical baseline 2020–2025; detailed scenarios 2026–2032).

- Segmentation frameworks across region, pump type (mechanical/electric/other) and application — with drill‑downs and interactive datapacks for client use.

- Supplier benchmarking and capability heatmaps, including manufacturing certifications, testing capacity, and product roadmaps.

- Value‑chain and cost‑to‑serve analyses highlighting margin pools and outsourcing tradeoffs.

- Regulatory and standards impact assessment (personnel certification changes, testing standards, EV thermal system rules) with compliance roadmaps.

- M&A and partnership playbooks with target screening criteria and synergy quantification templates.

- Commercial playbooks for aftermarket growth: go‑to‑market levers, installer certification programs, and warranty management approaches.

- Scenario modelling tools and sensitivity analyses to stress test strategies against raw‑material volatility, regulatory tightening, and accelerated EV adoption.

- Primary interview insights from OEMs, tier suppliers, and aftermarket distributors to validate market dynamics and supplier positioning.

Methodology and data integrity

The report uses 2025 as the base year, with historical analysis from 2020–2025 and a forecast period spanning 2026–2032. Our approach triangulates primary interviews, proprietary supplier audits, aftermarket channel checks, and public data sources. All forecasts are produced using bottom‑up models aligned with vehicle parc evolution, powertrain mix scenarios, and validated against supplier production capacity and industry orders. Where critical, we provide high/low scenarios and sensitivity matrices to support risk‑aware decision making.

How PW Consulting can support your 2026 agenda

- Rapid strategic briefings for executive teams that translate market sizing into prioritized investments and timebound milestones.

- Custom diligence and integration roadmaps for M&A or JV activity, focusing on testing assets, ECU expertise, and aftermarket reach.

- Operational readiness programs to implement 100% testing protocols, certification pathways, and installer upskilling at scale.

- Commercial go‑to‑market design for aftermarket players, including channel segmentation, bundled service kits, and digital parts platforms.

In short, the market’s mid‑single‑digit CAGR masks rich, actionable segmentation: winners in 2026 will be those who combine technical excellence (testing, ECU control, materials), distribution strength (service networks and certified installers), and the strategic flexibility to serve both OEM programs and aftermarket demand. The full PW Consulting study provides the granular datasets, competitor scorecards, and implementation templates your team needs to move from strategy to execution — with confidence and speed.

To access the complete report, interactive datapacks, and advisory options, visit our research portal or contact PW Consulting for a briefing tailored to your strategic priorities. The trailer is meant to orient; the full intelligence empowers decisions.

For detailed analysis of this topic, please visit the official page:Automotive Water Pump Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com