Global Oxide Dispersion Strengthened Alloys Market to Reach USD 3.1 Billion by 2032, Driven by Rising Demand in Aerospace and Energy Sectors VISUAL

Other |

2026-06-05 10:20:00

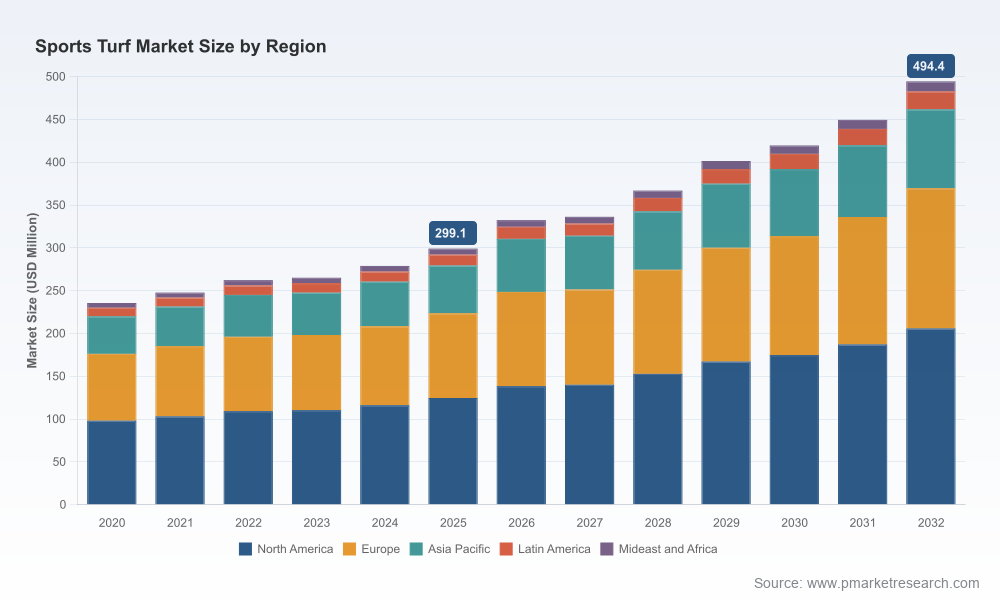

As sports venues, municipalities, and private operators recommit to premium playing surfaces, 2026 will be a pivotal year for executives and investors shaping the sports turf landscape. PW Consulting’s latest Sports Turf Market study—anchored on a 2025 base year and a forward-looking 2026–2032 forecast horizon—translates market dynamics into practical decision tools. With the global market having expanded steadily through 2020–2025 and a clear trajectory into the next decade (our model projects robust growth at a compound annual growth rate of 7.45% over the 2026–2032 forecast window), the choices made this year will determine competitive positioning, margin capture, and risk exposure for the next cycle of capital allocation.

Sports Turf Market

The market recorded consistent expansion during the historical review period, reflecting recovery from pandemic-era shocks and reinvestment in public- and private-sector sporting assets.

Sports Turf Market

Our forecast shows sustained acceleration through 2032 driven by equipment electrification, the adoption of autonomous maintenance platforms, and an expanding services & aftermarket opportunity tied to venue-level performance and sustainability certification.

Sports Turf Market

Market concentration is meaningful but not prohibitive—our concentration metrics indicate the top three vendors account for a substantial share of the market, with the leading five representing a clear majority footprint—creating both competitive pressure and consolidation opportunity for mid-sized challengers.

Leaders face competing demands in 2026: accelerate product and service innovation, defend margin against inflationary inputs, and navigate new standards that raise the bar on operational and environmental performance. This study is designed to serve as a decision-grade input for those exact tradeoffs. Specifically, it helps executive teams to:

Calibrate capital allocation—prioritizing electrification and automation pilots versus traditional equipment refresh.

Structure procurement and supplier strategies to limit exposure to near-term raw-material inflation and battery cell supply constraints.

Define aftermarket and service propositions that monetize data and maintenance-as-a-service while improving customer retention.

Inform M&A and partnership screening—including where to pursue tuck-ins that broaden service capability or add robotic/EV competencies.

Navigate compliance, certification, and sustainability credentials that increasingly drive venue procurement decisions.

The study is intentionally operational and structured to support implementation. Highlights include:

Interactive top-line forecast model (2026–2032), including scenario toggles for raw material price paths, labor-cost deflation via automation, and regulatory tightening.

Executive dashboard with forward-looking KPIs for revenue, margin, and service penetration tailored to corporate and product-level planning.

Go-to-market playbooks for three strategic archetypes—scale incumbents, specialized innovators, and distributor-led players—complete with route-to-market options and channel economics templates.

Capex and Opex planning templates that model trade-offs between fleet electrification, robotic adoption, and traditional maintenance equipment replacements.

Supplier risk maps and hedging strategies for steel and lithium-ion battery supply, and a procurement checklist to shorten lead times and stabilize margins.

Customer segmentation and willingness-to-pay frameworks (presented as anonymized archetypes) that support pricing and bundling decisions.

Regulatory and standards playbook—an actionable readout on the latest ISO workstreams and industry best practices that affect certification, safety, and environmental credentials.

Risk register and mitigation playbook covering supply chain, labor disruption, technological obsolescence, and reputational risk tied to sustainability performance.

Competitive benchmarking modules and M&A screening filters to accelerate diligence and integration planning.

To preserve strategic advantage for clients and motivate direct engagement, this preview omits the granular segmentation tables and proprietary unit economics that are available in the full report and companion data pack.

The competitive landscape blends global OEMs, specialized turf equipment manufacturers, and distribution-focused players. Key market participants we profile in the study include established OEMs with deep installed bases and aftermarket channels, robotics and electric drivetrain innovators, and distributors that bridge manufacturer capabilities to local operators.

The Toro Company: A legacy turf-equipment incumbent that has broadened into electrified rollers and operator-efficiency solutions. Recent product introductions underscore a push into all-electric field equipment optimized for consistent surface performance while lowering operating emissions.

Deere & Company: Leveraging scale in agricultural and turf machinery, Deere’s sports-turf arsenal is focused on robustness and dealer-backed service networks—an advantage for customers prioritizing uptime and trusted maintenance capability.

Husqvarna Group: Emphasizing commercial platforms and robotic automation, Husqvarna presents a product-led threat in autonomy for professional turf management.

STIHL: A strong presence in handheld and backpack segments, with a channel breadth that supports first-level maintenance across venue types.

Smithco and Sportsfield Specialties: Niche specialists that pair construction-grade equipment and field optimization tools with consultative services for institutional buyers.

Progressive Turf Equipment, MTD Products, Kubota, and distributor partners such as Turf Equipment and Supply Company: A mix of rotary mowing specialists, compact tractor suppliers, and channel-focused players that collectively shape local availability and aftermarket reach.

Strategically, incumbents are pushing electrification and aftermarket subscription models, while nimble innovators are exploiting autonomy and data services to displace labor-heavy contracts. Given that the top three companies control a material portion of the market and the five largest suppliers represent a clear majority, there is both defensive urgency for incumbents and fertile opportunity for consolidation and carve-out plays.

Notable recent development: a leading OEM expanded its all-electric greens roller portfolio in early 2026, signaling rapid acceleration of electrified field equipment at professional and premium amateur venues—an indicator that early-mover advantage in EV field platforms will be decisive for service revenue capture.

Raw-material inflation: Components such as steel and lithium-ion battery cells are exerting near-term pressure on manufacturing input costs. Strategic procurement and supplier partnerships are essential to protect margins.

Labor-cost compression via robotics: Ride-on robotic mowers and autonomous maintenance systems are reshaping field operations economics, shortening payback periods for capital-intensive automation in high-utilization venues.

Standards and best practices: ISO workstreams and industry associations are codifying operational, safety, and environmental expectations for sports and recreational facilities. Venue certification and adherence to best-practice maintenance standards are increasingly procurement filters for large buyers.

Aftermarket and services: Data-enabled maintenance, performance warranties, and environmental-compliance services are emerging as high-margin, recurring revenue streams.

Prioritize dual-track product roadmaps that balance near-term electrified replacements with medium-term investments in autonomy and fleet management software—protect both hardware and recurring service economics.

Establish supply-side hedges for steel and battery cells, including multi-sourcing, strategic inventory, and contractual indexation where possible to dampen margin volatility.

Pilot outcome-based service offerings (e.g., field-performance SLAs, turf-health-as-a-service) in 6–12 month windows to test pricing, cost-to-serve, and warranty exposure.

Invest in dealer and service networks to capture aftermarket revenue from electric and autonomous platforms—service capability is the moat that converts equipment sales into lifetime value.

Embed regulatory and certification readiness into product development cycles to accelerate procurement approvals by venue owners and public agencies following evolving ISO and association standards.

Use the study’s M&A screening filters to identify targets that add essential capabilities (autonomy, software, local service footprint) rather than incremental product lines.

For 2026, sports turf market participants must balance rapid technology adoption with disciplined risk management. PW Consulting’s Sports Turf Market study is built to convert market trends into operational action—providing the forecasting, playbooks, and diligence support to make confident commercial and investment decisions. This article highlights our core findings and their implications while reserving the report’s granular segmentation tables, transaction-ready financial models, and interactive dashboards for the full report package.

Decision-makers ready to operationalize these insights and obtain the full dataset, segmented analytics, and access to scenario-modeling tools should consult the complete PW Consulting Sports Turf Market report. It contains the data and templates you need to translate 2026 strategic intent into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Sports Turf Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com