ERP Software Market 2026 — Strategic Preview for Decision Makers

As PW Consulting’s Senior Strategy Advisor and Lead Industry Analyst, I present a concise, forward-looking preview of our full Enterprise Resource Planning (ERP) Software Market study — designed to inform the critical platform, procurement, and investment decisions you must make in 2026. This piece demonstrates the analytical depth and practical orientation of the research while preserving the proprietary segment-level detail that makes the full report indispensable for operational execution.

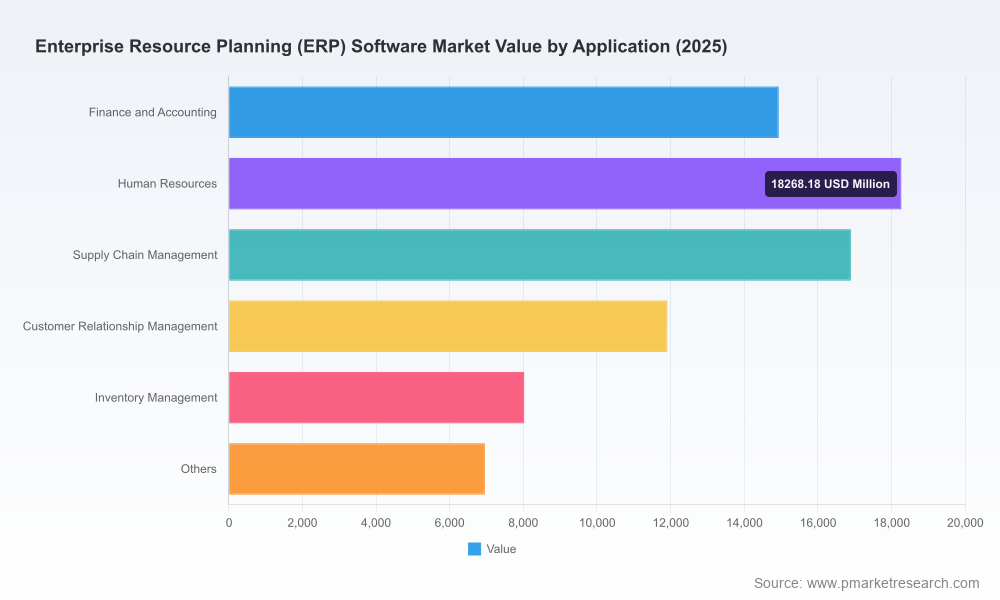

Enterprise Resource Planning (ERP) Software Market

Market snapshot: the macro story

The ERP market is in the midst of a multi-year expansion driven by cloud migration, embedded AI, and an accelerating need for end‑to‑end operational visibility. Using 2025 as our base year, the market stands on the order of magnitude of tens of billions of USD and is forecast to expand at a compound annual growth rate (CAGR) of approximately 9.5% through the 2026–2032 horizon. Under that trajectory, total market value is on course to roughly double from early‑decade levels by the end of the forecast window — reflecting a structural reshaping rather than a short cyclical spike.

Enterprise Resource Planning (ERP) Software Market

Importantly, market structure shows moderate concentration: the top three vendors control a meaningful share of revenue, and the top five capture a clear majority of market value. That balance — dominant global platforms plus a vibrant specialist mid‑market — drives both competitive intensity and partnership opportunities.

Enterprise Resource Planning (ERP) Software Market

Why this research matters for 2026 decisions

2026 is the year many enterprises will move from “proof” to “scale” with cloud ERP and AI-driven workflows. The strategic choices you make now will determine TCO profiles, change‑management burden, supplier dependency, and the speed at which new capabilities (especially agent‑style AI) deliver measurable business outcomes. Our study is built to do more than explain trends: it is an operational toolkit for executives, CIOs, and procurement teams tasked with execution in 2026.

- Align platform selection with business transformation timelines (not merely feature checklists).

- Quantify the long‑term TCO implications of SaaS subscription economics versus legacy on‑premise investments.

- Translate vendor roadmaps for AI, compliance, and industry‑specific functionality into procurement levers and negotiation targets.

- Calibrate M&A and partnership bets using unbiased market concentration, growth, and capability overlays.

Key market dynamics shaping 2026 choices

- Cloud economics and implementation tradeoffs: While cloud ERP implementations reduce upfront capital on hardware and data center procurement, ongoing subscription and hosting fees change the cash‑flow and Total Cost of Ownership profile. For many organizations, the migration also concentrates operational risk in software and hosting providers and requires new procurement and exit strategies.

- AI as a deployment and value lever: Vendors are embedding agent frameworks and developer toolchains that shift ERP from static back‑office suites to adaptive, task‑oriented systems. Recent launches demonstrate that vendor roadmaps now include agent‑ready tooling for HR, finance, and IT — creating new opportunities for automation and new governance challenges.

- Regulatory and policy inflection points: The regulatory environment is evolving: deregulatory proposals and harmonization efforts in major jurisdictions are reducing some compliance friction for cloud ERP, while sectoral rules (healthcare, finance) retain strict obligations. Continuous compliance capabilities — automated updates, audit trails, and built‑in controls — are now table stakes.

- SME implementation realities: Implementation cost drivers remain highly practical: customization, training, and upgrade disruption are recurring sources of project slippage. Industry surveys indicate customization and training remain prominent pain points in a substantial portion of SME projects; addressing these through modular deployments and pre‑configured vertical packs materially reduces risk.

Competitive landscape — what to watch in 2026

The competitive set combines global enterprise suites with specialist and mid‑market players. Each vendor’s strategy determines where they will win and what customers should expect from product roadmaps and commercial models. High‑level positioning of the core competitors covered in our study:

- SAP SE (Walldorf, Germany) — Strong enterprise footprint built on S/4HANA and Business One; deep capabilities in finance, manufacturing, and complex supply chains. SAP remains the strategic choice for heavy‑industrial and global rollouts where process depth and localization are critical.

- Oracle Corporation (Austin, Texas) — Oracle Fusion Cloud and NetSuite emphasize cloud‑native scale and global compliance features, with a strong push into supply chain resiliency and converged finance/operations suites.

- Microsoft Corporation (Redmond, Washington) — Dynamics 365 and Business Central pair ERP with Microsoft’s AI and platform ecosystem, making it attractive for organizations seeking integrations with productivity, identity, and data platforms.

- Workday, Inc. (Pleasanton, California) — Traditionally HCM‑centric, Workday’s expansion into finance and its recent rollout of developer‑grade AI agent tools underscore a strategy to deliver enterprise operations via AI‑augmented workflows.

- Infor (New York) — Specializes in industry‑specific CloudSuites for manufacturing and distribution; appeals when out‑of‑the‑box vertical functionality reduces custom work.

- QAD, Epicor, Sage, Acumatica, Odoo — These vendors compete across manufacturing, distribution, and SMB markets with varying tradeoffs on configurability, pricing transparency, and community support. Notably, consolidation activity (e.g., a significant private‑equity acquisition in 2025) signals continued M&A interest in the mid‑market.

Two recent events exemplify market direction: a 2025 acquisition in the cloud ERP mid‑market, and a 2026 product launch focused on AI agent tooling for enterprise workflows. Together they highlight consolidation in the mid‑market and the rapid incorporation of agent paradigms in vendor roadmaps.

What the full PW Consulting ERP report contains (practical, actionable deliverables)

Our full study goes beyond narrative to provide the execution assets that CIOs, program leads, and CFOs need in 2026. Highlights include:

- Proprietary demand and supply forecasts with sensitivity bands and scenario planning based on adoption, regulation, and macroeconomic inputs.

- Vendor scorecards and fit‑for‑purpose matrices that map capabilities (finance, manufacturing, SCM, HCM, CRM) to typical buyer archetypes.

- TCO and ROI models (including subscription vs capital comparisons), plus interactive calculators you can run against your own data.

- Implementation playbooks and phased migration templates to manage customization, training, and upgrade risk.

- Contract and SLA negotiation benchmarks, procurement checklists, and an outcomes‑based contracting framework tailored to cloud ERP engagements.

- Regulatory compliance checklists and an actionable watchlist for evolving jurisdictional policy changes impacting cloud hosted ERP.

- Deal flow and M&A maps with valuation multiples, consolidation risks, and partner ecosystem overlays for alliance strategies.

Note: To preserve competitive integrity and deliver a compelling value proposition, the full report includes granular segmentation, regional and application splits, and vendor‑level revenue benchmarks that we do not reproduce in this preview. Those datasets power the proprietary models and scorecards referenced above.

Strategic recommendations for leaders making ERP decisions in 2026

- Adopt a modular migration strategy: prioritize high‑value processes (finance close, core supply chain) for early cloud deployment, deferring lower‑value or highly customized modules until common standards and ecosystems mature.

- Build an AI integration playbook now: evaluate vendor agent toolchains for developer experience, governance controls, and auditability before committing to deep automation designs.

- Insist on outcome‑based commercial constructs: push for SLAs and success metrics tied to business outcomes (cycle time reduction, FTE redeployment, error rates) rather than purely technical uptime.

- Quantify concentration and vendor lock‑in risk: use multi‑scenario TCO analysis to stress‑test the impact of supplier outages, pricing shifts, or accelerated upgrades.

- Mitigate SME implementation pain points: demand pre‑packaged vertical configurations, training bundles, and upgrade roadmaps that limit customization and reduce long‑term maintenance.

- Maintain an active regulatory watchlist: embed compliance automation in procurement criteria and ensure continuous delivery pipelines account for auditability and data residency needs.

- Evaluate mid‑market consolidation for strategic acquisition or partnership opportunities: M&A can be a fast route to acquiring pre‑configured vertical IP or expanding geographies — but perform rigorous integration earn‑out modeling.

How PW Consulting accelerates your 2026 agenda

The full PW Consulting ERP report is built to shorten decision cycles and de‑risk implementation. It pairs a rigorous macro forecast (anchored to the 2025 base year and projecting forward with a 9.5% CAGR) with deal‑ready artifacts: thermal risk maps, vendor negotiation playbooks, TCO sensitivities, and implementation accelerators. If your team is preparing RFPs, defining a migration roadmap, evaluating M&A targets, or negotiating a multi‑year enterprise agreement in 2026, our report supplies both the evidence base and the operating templates to act fast and with conviction.

For the full dataset, segmented forecasts, downloadable models, and vendor‑level analysis that underpin the above insights, please access the complete PW Consulting ERP Software Market study. The detailed segmentation and proprietary scorecards are intentionally available only in the full release to ensure you have the defensible intelligence required for board‑level decisions and supplier negotiations.

Contact PW Consulting to request the full report, bespoke briefings, or direct advisory support tailored to your industry and transformation timeline.

For detailed analysis of this topic, please visit the official page:Enterprise Resource Planning (ERP) Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com