Could Natural Wellness Trends Boost the Ayurvedic Personal Products Market?

Networking |

2026-07-03 07:04:45

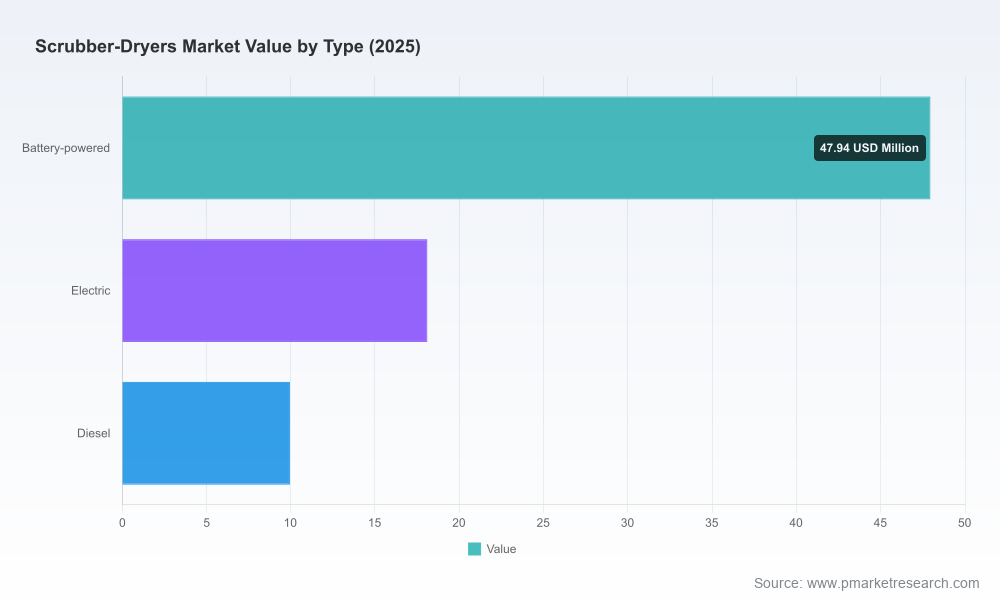

As facility managers, OEM executives, and private-equity sponsors set budgets and strategic priorities for 2026, the scrubber-dryers market presents a classic growth-with-disruption profile. Our PW Consulting Scrubber-Dryers Market study (base year 2025, forecast period 2026–2032) shows an industry re-accelerating from post-pandemic normalization into a phase of digitization, sustainability-driven product replacement, and service-led monetization. The market reached USD 76.0 Million in 2025 and is forecast to expand at a 4.8% CAGR across the 2026–2032 horizon, reaching roughly USD 97.0 Million by 2032. That trajectory underpins distinct strategic choices in product investment, channel strategy, and M&A through 2026 and beyond.

Scrubber-Dryers Market

Timing of investment: The market’s mid-single-digit CAGR signals steady demand—enough to justify selective capacity and R&D investments, but not a broad race for volume that compresses margins. 2026 is a window to prioritize high-return product upgrades (battery systems, autonomous capability, water/chemical efficiency) over low-margin expansion.

Scrubber-Dryers Market

Technology and cost trade-offs: Advances in battery tech, telematics, and AI-enabled routing are changing service economics. Buyers are trading higher capex for demonstrable OPEX reductions—an important consideration for financing and leasing structures in 2026 contracts.

Scrubber-Dryers Market

Regulatory and procurement filters: Sustainability metrics and environmental rules (e.g., EU Green Deal requirements and U.S. EPA/OSHA clean-floor expectations) are increasingly embedded in procurement RFPs. Products that document energy, water, and detergent savings have clearer paths to specification.

Service and aftermarket upside: With moderate market concentration and fragmented end-user procurement, aftermarket consumables, preventive service contracts, and telematics-enabled SLA offerings represent high-margin expansion routes.

Market sizing & forecast model (2020–2032): a transparent, auditable model calibrated to macro demand drivers and validated against vendor shipment signals.

Scenario-based demand simulations: baseline (policy-neutral), sustainability-accelerated, and automation-accelerated pathways—each with sensitivity to labor-cost curves and raw material price shocks.

Technology adoption curves: detailed adoption timelines for battery chemistries, autonomous navigation, telematics, and advanced dosing systems—mapped to TCO inflection points for typical facility types.

Product benchmarking & feature parity matrix: side-by-side analysis of fielded models (walk-behind, ride-on, compact micro-scrubbers) emphasizing energy, water, detergent, and maintenance metrics.

Go-to-market playbook: channel segmentation, financing constructs (leases, subscription, pay-per-clean), and procurement win strategies for 2026 RFP cycles.

Aftermarket and services model: revenue forecasts for spare parts, consumables, and remote monitoring services with margin profiles and cross-sell strategies.

Risk & compliance register: regulatory scenarios, warranty liabilities, and supply-chain vulnerability scores with mitigations and contingency plans.

Policy-driven product specification: Environmental standards in the EU and tighter procurement requirements in several jurisdictions are turning sustainability features from marketing differentiators into procurement prerequisites. Buyers increasingly require documented metrics on water consumption, detergent use, and recycled-content construction.

Labor-cost push to automation: Rising facility labor costs are accelerating adoption of ride-on machines and purpose-built autonomous scrubbers. Automated routing and uptime guarantees now factor directly into procurement ROI calculations.

Material circularity and production energy: OEMs are moving toward post-industrial recycled plastics (polypropylene, polyethylene, PET) to reduce embodied energy. Independent studies indicate this can significantly lower production energy footprints—an advantage for sustainability claims and life-cycle assessments.

Product innovation is measurable: Recent product introductions demonstrate meaningful operational improvements. For example, new walk-behind models now advertise step-changes in energy efficiency, water reduction, and detergent use, while compact micro-scrubbers are displacing labor-intensive manual mopping in high-turnover venues.

Regulatory tailwinds for electrification: Safety and environmental guidelines that favor zero-emission, low-noise equipment support battery-powered units in regulated indoor settings, widening institutional procurement opportunities.

The market exhibits moderate concentration, with the top three and top five players capturing a meaningful but not dominant share—creating room for both incumbents and fast-follow innovators. Below is a strategic snapshot of core players featured in our analysis.

Nilfisk Group (Denmark): Strong in both walk-behind and ride-on categories, Nilfisk is emphasizing resource optimization and user-centric digital features. Recent launches showcase significant improvements in energy efficiency and resource consumption, positioning Nilfisk well in sustainability-led procurement.

Alfred Kärcher (Germany): Kärcher combines product breadth with sustainability engineering—recycled plastics in construction and efficient dosing systems—making it a preferred supplier where green procurement is prioritized.

Tennant Company (United States): Tennant’s push into autonomous and IoT-enabled machines is a differentiator for large facilities seeking route optimization and preventative maintenance. Its approach highlights the attached-value opportunity in software and services.

Hako GmbH (Germany): Hako retains strength in professional ride-on and walk-behind equipment with a focus on industrial customers and service reliability.

Taski / Diversey (United States): Integration of cleaning chemicals and equipment gives Taski unique leverage in sectors requiring certified disinfection and compliant cleaning protocols, such as healthcare and hospitality.

Numatic, RPS, Polivac, Eureka, Comac: These players cover compact, small-to-medium, and heavy-duty industrial niches. Their market strategies emphasize simplicity, durability, and productivity—key attributes for contract cleaning businesses and large industrial estates.

OEMs: Prioritize modular architectures that enable incremental upgrades—battery packs, autonomy modules, telematics subscriptions. This reduces development cycle risk and creates recurring revenue pathways.

Distributors & service networks: Invest in remote diagnostics, technician upskilling, and bundled service contracts. Service differentiation will be a primary retention engine as fleet ownership shifts to uptime-and-outcomes procurement models.

Facility operators: Re-evaluate procurement on total cost of ownership and outcome guarantees (cleaning time, wet-floor risk reduction, sustainability metrics) rather than unit price. Run pilot programs in 2026 focusing on autonomy and telematics to quantify labor savings.

Private equity & M&A: Target bolt-on acquisitions in telematics/software, local service networks, or niche industrial scrubber specialists to capture aftermarket margins and consolidate regional service footprints.

Supply chain managers: Secure sources of recycled plastics and diversify battery suppliers to mitigate raw-material and component concentration risks. Consider forward contracts or strategic partnerships with recyclers.

Baseline: The market follows the projected 4.8% CAGR, with steady upgrades and replacement cycles driving measured growth.

Upside: Rapid adoption of autonomy and financing-as-a-service accelerates fleet refresh rates and drives above-baseline growth—favouring vendors with telematics platforms and financing capabilities.

Downside: Raw-material price spikes or delayed regulatory alignment suppress capital procurement and extend equipment lifecycles—shifting focus to aftermarket service revenue to preserve margins.

Use the report’s TCO models to validate capex vs. opex trade-offs before committing to large-scale fleet upgrades in 2026.

Adopt the procurement playbook to reconfigure RFPs around outputs (cleaning outcomes, safety metrics, sustainability KPIs) rather than inputs (machine model specs alone).

Apply the scenario toolkit to stress-test M&A targets and to size the serviceable aftermarket under alternative adoption pathways.

This preview intentionally frames strategic choices and market contours while withholding granular regional and application splits that drive tactical execution. The full PW Consulting Scrubber-Dryers Market report contains the precise segmentation, regional breakdowns, vendor share tables, and downloadable financial models you will need to build investment cases and procurement templates for 2026. Accessing the complete dataset and appendices will allow you to:

Run tailored TCO scenarios with your own wage and energy inputs;

Benchmark specific competitor models and feature-level performance;

Extract region- and application-specific demand forecasts for localized go-to-market plans.

Contact PW Consulting to obtain the full report and the editable forecast model. Our team can also deliver a 90-minute workshop to translate the report’s findings into a prioritized 18-month action plan for equipment OEMs, distributors, or facility management organizations.

PW Consulting advises industrial-technology clients on market strategy, commercial due diligence, and growth transformation. Our scrubber-dryers practice combines product-level engineering analysis, procurement economics, and service-business modelling to help clients convert market trends into captured value. For decision-makers planning 2026 investments, our study provides the framework and the executable modules to move from insight to action.

For detailed analysis of this topic, please visit the official page:Scrubber-Dryers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com