Adult Hearing Aids Market: Future Growth Engines, Investment Trends, and Strategic Outlook 2026-2034

Other |

2026-06-01 20:48:09

As OEMs accelerate model refreshes for cross‑overs, SUVs and EV lineups, the power liftgate has shifted from a convenience accessory to a material contributor to vehicle safety, energy budget and perceived vehicle quality. PW Consulting’s latest Automotive Power Liftgate Market study (base year 2025) synthesizes market dynamics, supplier strategies and technology trajectories that will determine winners and losers over the 2026–2032 planning horizon. The global market—having expanded from the mid‑hundreds of millions USD in 2020 to approximately USD 215 million in 2025—is forecast to grow at a 7.6% CAGR, reaching roughly USD 345 million by 2032. For executives making product, sourcing and M&A decisions in 2026, the implications are immediate: hardware choices, materials decisions and software integration strategies will materially affect unit economics, time‑to‑market and residual value.

Automotive Power Liftgate Market

Product roadmaps now need to balance three vectors simultaneously: mass reduction for EV range, safety and regulatory compliance, and differentiated UX (hands‑free/gesture recognition). Our study translates market trajectories into concrete KPIs for each vector so engineering and commercial teams can align.

Automotive Power Liftgate Market

Sourcing strategies are under stress from raw‑material concentration and price volatility. The report highlights where supply risk is concentrated (magnets, copper) and presents mitigation levers—technical and commercial—that procurement teams can implement in 2026.

Automotive Power Liftgate Market

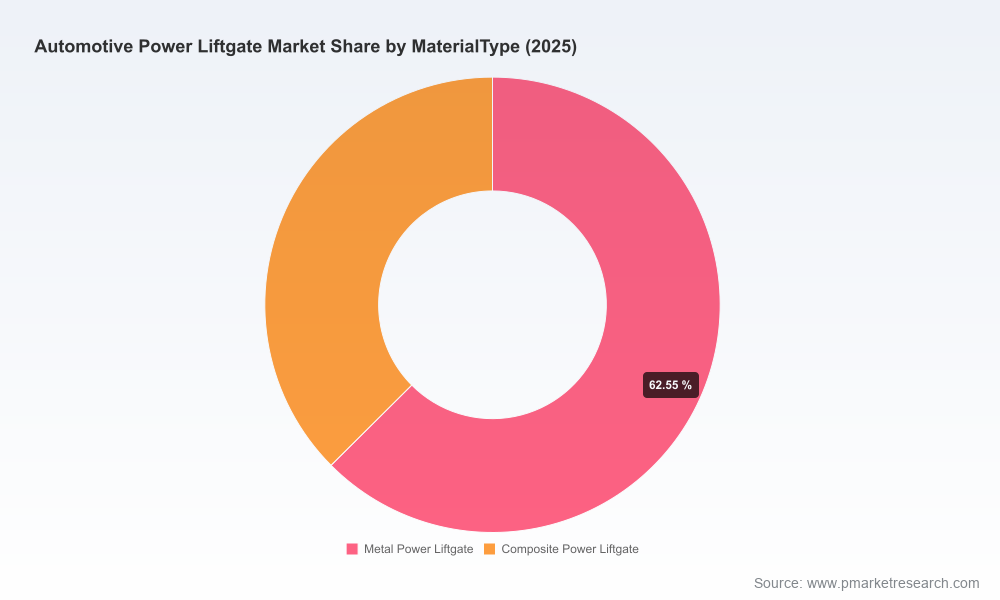

Supplier selection and pricing: the market exhibits modest concentration (CR3 ≈ 24.6%, CR5 ≈ 26.2%), meaning scale leaders exist but a broad field of specialized suppliers remains. We map how these competitors compete—by full‑system modules, lightweight materials, actuation technologies or sensor integration—guiding tier selection and negotiation posture.

Regulatory readiness: pending and evolving safety standards are raising the bar for anti‑pinch performance, environmental robustness and electrical compatibility (12V/48V). Decisions made in 2026 about architecture and validation scope will lock in compliance costs and time to homologation.

Time‑series market sizing (2020–2032) and growth scenarios tied to vehicle production outlooks and EV penetration rates, enabling finance teams to stress‑test investment cases against demand scenarios.

Technology roadmaps articulating the tradeoffs across actuator types (spindle, push‑rod, electromechanical with/without gas‑spring assist), motor topologies and sensor suites. For each approach we quantify expected impacts on mass, energy draw and bill‑of‑materials complexity.

Supplier profiles and capability matrices that highlight who delivers full system modules, who specializes on high‑torque motors, and who offers lightweight thermoplastic structures versus traditional metal designs.

Procurement playbooks and TCO models—covering material cost drivers, anticipated warranty exposure and service economics—that procurement and product managers can use during RFPs and contract renegotiations.

Risk matrices and scenario planning tools, which bundle raw‑material shocks, regulatory tightening and competitive technology shifts into actionable contingency plans for program managers.

Electrification and energy budgets: As OEMs squeeze every kWh to extend EV range, liftgate mass and actuation energy consumption are scrutinized. Lightweight structures and more efficient actuation are becoming baseline requirements on many EV programs.

Material and component supply chains: Permanent‑magnet motor production is visibly impacted by rare‑earth supply concentration, and copper price volatility continues to affect motor winding costs. These inputs create asymmetric risk across actuator technologies and geographies.

Sensor fusion and UX: Hands‑free activation, ultra‑wideband (UWB) positioning and radar‑based occupant detection are migrating from concept demos to production intent. These capabilities confer differentiation but also require deeper software, validation and cybersecurity investments.

Regulation and safety: Global safety standards emphasize anti‑pinch protection and performance across temperature ranges, while electrification trends push compatibility with both 12V and 48V domains. Early design alignment with these constraints reduces costly rework during homologation.

The field combines global tier‑ones that offer complete modules with specialized vendors that own critical subsystems. The CR3 and CR5 metrics reflect a market with recognizable scale players but meaningful room for niche leaders and technology specialists. Highlights from the competitive analysis:

Brose focuses on modular drive concepts (spindle and push‑rod variants), integrating sensors and power‑cinching units. Their recent demonstration of ultra‑wideband and radar activation in a concept vehicle underscores a strategy that pairs electromechanics with advanced sensing to capture OEM system‑integration programs.

Aisin continues to anchor programs in Asia with integrated actuator and control solutions tuned for local OEM architectures—making them a preferred partner where platform commonality and supplier co‑development are priorities.

Magna plays the full‑system angle: electric actuators, hands‑free detection, integrated ECUs and a clear push into thermoplastic lightweighting. Their thermoplastic liftgate announcement demonstrates a tactical response to EV efficiency requirements and shows where modular suppliers can win by co‑optimizing structure and actuation.

Continental is deploying strengths in body electronics and motor control, providing anti‑pinch motor control and integration with vehicle networks that reduce OEM integration effort.

Specialists—Huf, Stabilus, Hi‑Lex, Strattec and Johnson Electric—are carving durable niches: latches and striker systems, hybrid gas‑spring + electromechanical drives, actuator assemblies for specific platform form factors, integrated security modules and high‑torque, high‑density motor solutions respectively. Their value lies in depth of component IP and program‑level reliability.

Prioritize architectures that decouple mass and actuation energy: favor modular systems where liftgate skins and actuators can be independently optimized. This accelerates supplier competition and allows OEMs to tune solutions per platform (ICE vs EV).

Hedge magnet and copper exposure: engineer dual‑compatible motor topologies and establish multi‑sourcing for magnet components. Negotiate supplier contracts that include indexation clauses or price‑sharing mechanisms to limit near‑term margin shock.

Invest in sensor fusion and over‑the‑air update capabilities: secure UX differentiation while minimizing field recall risk. A software‑first validation plan reduces system integration timelines and creates ongoing revenue streams (feature unlocks, subscription services).

Pursue selective partnerships and bolt‑on acquisitions: the market size and moderate concentration favor targeted M&A to acquire specific IP (lightweight skins, BLDC motor specialists, sensor algorithms) rather than large scale buyouts.

Embed regulatory readiness in the program gating process: treat anti‑pinch and temperature‑range validation as a design driver, not a downstream test. Early compliance alignment cuts certification cycles and warranty exposure.

Design for service and retrofitability: as consumers seek enhanced convenience post‑purchase, offering upgradeable sensor modules or retrofit actuators creates aftermarket revenue opportunities and strengthens dealer ecosystems.

Raw‑material shocks (rare earths, copper) can rapidly alter BOM parity between actuator types; scenario models in the report quantify break‑even points for primary actuator choices.

Regulatory tightening on safety features could raise validation and certification costs; the report provides threshold scenarios and mitigation timelines for common regulatory regimes.

Technological disruption—e.g., a low‑cost, high‑efficiency actuation topology or a commoditized sensor suite—could compress margins for incumbent suppliers. We outline defensive IP and pricing responses tailored to supplier archetypes.

Conclusion: The power liftgate market in 2026 is not a niche convenience item—it is a cross‑functional lever that affects vehicle mass, system energy, perceived quality and software monetization. PW Consulting’s study translates market momentum (7.6% CAGR) and observed supplier moves into practicable strategies for product, procurement and corporate development teams. This briefing intentionally highlights themes and strategic implications while omitting detailed segment tables and regional splits to preserve the actionable insights that live in our full model.

For the complete segmentation, supplier scorecards, interactive TCO calculators and program‑level scenario outputs that will underpin 2026 decision cycles, access the full Automotive Power Liftgate Market report on our website or contact your PW Consulting engagement lead.

For detailed analysis of this topic, please visit the official page:Automotive Power Liftgate Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com