Bipolar Forceps Market — Strategic Outlook and 2026 Playbook for Executive Decision‑Makers

As hospitals, device manufacturers and private equity sponsors calibrate strategy for 2026, the bipolar forceps market presents a classic “steady-growth, high-stakes” opportunity: resilient baseline expansion driven by procedure volumes and device innovation, but front-loaded with tactical trade-offs (reusable vs single‑use, thermal control vs cost, product breadth vs SKU rationalization). This preview highlights the strategic value of PW Consulting’s full Bipolar Forceps Market study for 2026 decision-making — offering the context, competitive signals and action frameworks you need today, while intentionally withholding the granular segment and regional tables reserved for the full report.

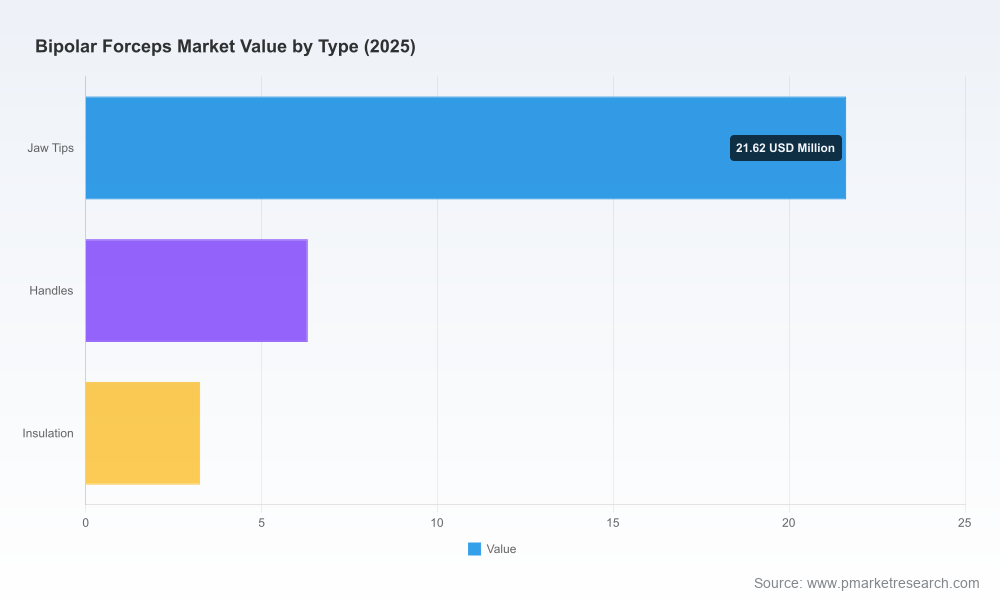

Bipolar Forceps Market

Executive snapshot — what the market looks like at a glance

Using 2025 as the base year, our analysis traces a clear, steady uptrend from the 2020 baseline through the 2025 checkpoint and projects continued expansion across the 2026–2032 forecast window. The market has shown a resilient multi-year recovery and is projected to grow at a mid-single-digit compound annual growth rate (CAGR) over the forecast period. In absolute terms, the market scale moves from the mid‑tens of millions (USD, Million unit of account) in 2020 to a mid‑40s million projection by 2032, reflecting predictable demand uplift from procedure growth, broader adoption of minimally invasive approaches and iterative product innovation.

Bipolar Forceps Market

Two structural implications are visible from this macro shape: (1) product innovation and differentiation — especially around non‑stick finishes, irrigation capability, and sensor-enabled precision — is the fastest route to expand product margins; (2) total cost of ownership (TCO) considerations in hospitals — sterilization, inventory management and OR throughput — will increasingly determine buyer preference between reusable and disposable options.

Bipolar Forceps Market

Why this study matters for 2026 strategic choices

- Prioritizing R&D investment: Which incremental features (irrigation rates, non-stick coatings, insulated tip geometry, sensor integration) materially drive purchasing decisions and justify premium pricing? Our study maps feature‑level value capture against buyer willingness to pay.

- Go‑to‑market sequencing: Where should firms deploy limited commercial resources (key opinion leader programs, OR trials, distributor partnerships) to maximize early adoption in the clinic and accelerate hospital contracts?

- M&A and partnership screening: Which midsize suppliers represent accretive SKU breadth or geographic access for rapid scale, and how to price acquisitions using conservative synergies?

- Procurement and pricing optimization: How to structure bundled offers (devices + reprocessing services) and assess TCO vs list price to win health system formularies.

- Manufacturing and supply resilience: Where to localize production to mitigate shipping disruptions and cost inflation while protecting product quality and regulatory compliance.

Key market drivers and headwinds

- Clinical demand drivers: Ongoing expansion of elective and minimally invasive procedures and the move toward energy‑based hemostasis sustain baseline device demand.

- Feature competition: Irrigating and non‑stick forceps, as well as sensor‑enabled precision instruments, are focal points for differentiation — evidenced by recent product introductions from established players.

- Cost pressure from sterilization and labor: Reusable instruments require repeated sterilization cycles and maintenance. We model sterilization costs of multiple cycles per instrument and incorporate external findings that a single sterilization cycle can add up to several dollars in direct cost, cumulatively representing material pressure on hospital operating budgets (sector analysis, March 2026).

- Regulatory and procurement cycles: Device approvals and hospital procurement timelines create multi‑quarter adoption lags; successful market entrants must plan for elongated sales cycles and early clinical evidence generation.

Report contents — practical, transaction‑ready deliverables

The full PW Consulting report converts market intelligence into tools that enable immediate action. Highlights include:

- Market sizing and trend models (historical 2020–2025 and forecast 2026–2032) with downloadable Excel models that allow scenario toggling on pricing, adoption rates and unit shipment assumptions.

- Feature‑level demand drivers and a product‑feature matrix that links clinical priorities to price elasticity and margin impact.

- Commercial playbooks for manufacturers and distributors: surgeon engagement, OR trial design, tender response templates and distributor scorecards.

- Supply‑chain and manufacturing assessment, including cost build‑ups and options for contract manufacturing vs in‑house production.

- Regulatory and reimbursement intelligence: country‑level timelines, submission requirements, and payer positioning that affect adoption speed.

- Competitive benchmarking with SKU‑level profiling, go‑to‑market motions, and capability heatmaps for product, manufacturing and service layers.

- Decision support tools for private equity: diligence checklists, synergy assessment templates and exit scenario modeling.

Note: this preview intentionally omits the full segmentation tables and country‑level detail — those are included in the subscription package and bespoke engagements.

Competitive landscape — who’s shaping the market

The market is moderately concentrated: the top three global players capture a meaningful share of revenue, while the top five consolidate a larger portion of volume and influence. This concentration profile produces both advantages and strategic challenges: dominant players set clinical expectations and technical baselines, while mid‑tier and regional suppliers can win on cost, niche features or service models.

- Aesculap (Center Valley, PA) — extensive portfolio across reusable and disposable forceps with recent product developments emphasizing irrigating, non‑stick disposable offerings. Their October 2025 launch of an irrigating specialty non‑stick disposable forceps underscores competition centered on irrigation throughput and single‑use convenience.

- Medtronic (Minneapolis, MN) — emphasis on precision control and sensor integration for electrosurgery; positions strongly where system‑level integration and data feedback matter.

- B. Braun (Melsungen, Germany) — focus on ergonomics and insulation to minimize lateral thermal spread, appealing to surgical groups prioritizing tissue preservation.

- CONMED (Largo, FL) and Stryker (Kalamazoo, MI) — strong in laparoscopic and neurosurgical niches respectively, with offerings spanning reusable and single‑use options.

- KLS Martin, Kirwan Surgical, Stingray and Integra LifeSciences — specialist vendors with strengths in microsurgery, mixed‑matrix materials and ergonomic designs that win in high‑precision cases.

- Asia‑based suppliers (including manufacturers from China and India) — increasingly relevant for cost‑competitive disposable lines and for regional supply expansion.

Strategically, the competitive dynamic is bifurcating: platform players leverage breadth and system integration, while nimble specialists compete on advanced surface treatments, irrigation performance or price advantage for single‑use disposables.

Strategic implications and recommended 2026 actions

- Adopt a TCO‑first commercial argument: For manufacturers targeting hospital formularies, present comparative analyses that fold sterilization cycle costs, instrument downtime and OR throughput into the pricing pitch.

- Invest selectively in high‑value features: Prioritize R&D for non‑stick chemistries, higher irrigation outputs and sensor feedback that demonstrably reduce procedure time or complication rates; these features convert into premium positioning in tender evaluations.

- Pilot bundled service offerings: Test device plus reprocessing service bundles in a controlled set of health systems to evaluate margin uplift and lock‑in effects without broad capex exposure.

- Rationalize SKUs and pricing: Trim low‑velocity SKUs to reduce manufacturing complexity and inventory cost; reallocate commercial spend to high‑margin lines and surgeon training programs.

- Expand regional manufacturing selectively: For firms with global ambitions, locate production to balance cost advantages with regulatory pathway speed and customer proximity.

- Pursue targeted M&A: Acquire niche technology providers that complement surgical portfolios (e.g., irrigation modules, non‑stick surface treatments) rather than duplicative breadth acquisitions.

- Prepare for procurement shifts: Equip sales teams with hospital‑specific TCO calculators and OR productivity case studies to navigate tightening budgets in 2026.

What this preview withholds — and why

Following the “trailer” principle, this article demonstrates PW Consulting’s analytical depth while withholding the core granular tables that often determine commercial actions: we do not publish the detailed regional and end‑use percentage splits, SKU‑level price curves, country‑by‑country forecasts, or the confidential supplier contract benchmarks in this preview. The full report contains those tables, the downloadable financial model, SKU benchmarking sheets, and customer survey data that underlie our recommendations.

How PW Consulting accelerates implementation

- Executive briefings tailored to C‑suite and board needs (90‑minute deep dives with Q&A).

- Custom Excel models with scenario toggles for pricing, adoption curves and M&A valuation inputs.

- Vendor shortlists and RFP support for procurement teams, including templated contract language for bundled offerings.

- Due diligence support for investors: technical diligence, regulatory risk assessment and synergy quantification.

For teams making strategic commitments in 2026 — whether launching new bipolar forceps SKUs, negotiating hospital formularies, or evaluating acquisition targets — the right combination of market sizing, competitive intelligence, and execution playbooks is essential. PW Consulting’s full Bipolar Forceps Market study packages that combination into actionable intelligence and transaction‑grade tools.

To access the complete dataset, SKU benchmarks, and downloadable models that power the above insights, please visit our report page or contact our industry team for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Bipolar Forceps Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com