Central Venous Catheters Market — 2026 Strategic Briefing for Executives

As healthcare systems recalibrate capital allocation and clinical pathways in 2026, central venous catheters (CVCs) have re-emerged as a focal point for clinical efficiency, infection‑prevention investment, and device innovation. This industry briefing — derived from PW Consulting’s full Central Venous Catheters Market study (base year 2025) — frames the market trajectory, competitive dynamics, regulatory inflection points and the practical, near-term choices executives must make to preserve share and capture value. Consider this a professional “trailer”: it demonstrates the analytical depth that underpins our conclusions, while reserving the granular segmentation tables and scenario models for the full report.

Central Venous Catheters Market

Market snapshot (concise, data-driven)

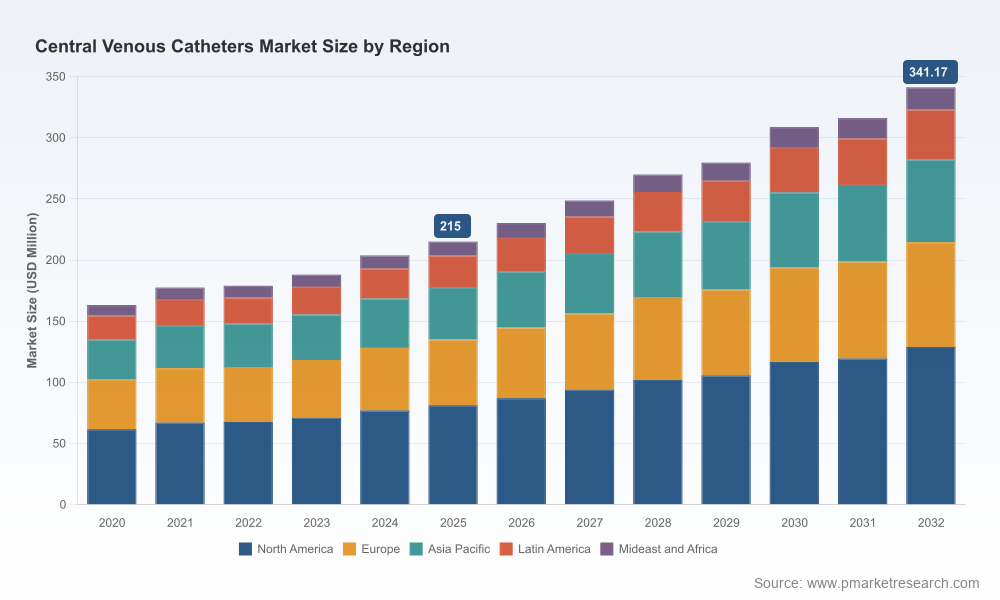

Our base-year analysis finds the global CVC market at approximately USD 215.0 Million in 2025 after steady growth through the 2020–2025 historical window. Under our central forecast the market expands at a compound annual growth rate (CAGR) of 6.8% over 2026–2032, reaching roughly USD 341.17 Million by 2032. The near-term step-up between 2025 and 2026 is notable, reflecting renewed capital spending in acute-care vascular access and accelerating adoption of enhanced-insertion systems and infection-mitigation technologies.

Central Venous Catheters Market

These topline dynamics are driven by three intersecting forces: (1) persistent clinical demand for reliable central venous access across critical care, oncology and interventional radiology; (2) supplier-led product innovation — from integrated insertion systems to antimicrobial coatings and pressure‑injectable CVCs — that change purchasing criteria; and (3) regulatory and standards updates that raise validation and testing expectations for single‑use catheter products.

Central Venous Catheters Market

Why this analysis matters for 2026 corporate decisions

- Resource allocation: The market’s mid-single-digit CAGR creates a finite runway for R&D and commercialization spending. Leaders must prioritize offers that materially affect clinical outcomes or provider workflow to justify investment.

- Portfolio rationalization: With product development cycles and regulatory lead times compressing, deciding which CVC variants to scale, shelve or partner on is a make-or-break decision for 2026 P&Ls.

- Regulatory preparedness: New test standards and recall activity have sharpened buyers’ procurement filters. Companies must accelerate conformity testing and supplier controls to avoid market disruptions.

- M&A and partnership timing: Moderate market concentration combined with ongoing technology differentiation creates tactical windows for bolt-on transactions or co-development agreements ahead of projected volume increases.

- Go-to-market and clinical evidence: Adoption now hinges on demonstrable reductions in time-to-use, infection rates, or insertion complications — not just product specs. Clinical, real-world evidence will be a primary purchasing lever.

What the PW Consulting report delivers (practical, operational content)

- Topline market model (2020–2032) with downloadable scenarios: baseline, conservative and aggressive uptake curves calibrated to procedure volumes and adoption rates.

- Demand-driving use cases and procurement pathways: clinician decision trees, hospital buyer personas, and purchasing-cycle timelines (capital vs. consumables procurement).

- Product-technology deep dives: insertion systems, pressure‑injectable lines, antimicrobial coatings, multi‑lumen trade-offs, securement and disinfection integrations — with technology readiness assessments and adoption friction scoring.

- Competitive playbooks and capability matrices: public/private company profiles, go-to-market vectors, and a qualitative strength/opportunity map for each major vendor.

- Regulatory and quality roadmap: implications of recent standards, recommended validation strategies, and a recall‑risk mitigation checklist for supplier and contract-manufacturing oversight.

- M&A and ROI scenarios: target screening criteria, valuation sensitivities and post‑close integration checklists tailored to the CVC subdomain.

- Commercial tactics and pricing models: value-based contracting templates and hospital-level ROI calculators to support field teams.

Each module in the report is organized for immediate operational use — slide decks for executive briefings, Excel models for commercial planning, and an implementation playbook for product and regulatory teams.

Competitive landscape — practical implications for strategy

The CVC vendor field combines large legacy device manufacturers and specialized vascular-access suppliers. Market concentration measurements indicate a moderate level of aggregation: the three largest suppliers collectively hold roughly 35% of reported market revenue, while the top five approach just over half the market. That positioning produces both competitive stability and clear pockets of opportunity for differentiated entrants.

- Becton Dickinson and Company (BD): BD’s strengthened presence in acute and short‑term CVCs — exemplified by the commercial introduction of the CentroVena One Insertion System (FDA 510(k) clearance in April 2025, commercial launch April 2026) — signals a strategic push into integrated insertion workflows. Expect BD to lean on system-level adoption (device + insertion platform + training) to expand wallet share within high-volume acute channels.

- Teleflex (Arrow brand): Teleflex’s Arrow line remains a fixture in critical care, particularly where pressure‑injectable and antimicrobial-coated options are required. Their focus on kit-based convenience and infection mitigation targets procurement teams that value bundled solutions.

- B. Braun, Cook Medical, Merit, Terumo, Nipro, Vygon and others: These regional and global suppliers sustain demand across hospital networks and specialty centers. Their portfolios emphasize product breadth, manufacturing scale and clinician relationships — attributes that preserve share but also invite focused competition where innovation accelerates.

- ICU Medical and Access Vascular: Expect differentiated moves around securement, integrated disinfection and advanced insertion technologies. These are the firms most likely to convert clinician workflow improvements into share gains.

- AngioDynamics: With an oncology and interventional orientation, AngioDynamics is positioned to capture procedure‑specific demand, particularly where multi‑lumens and durable vascular access are required.

Recent industry events underscore the importance of both quality governance and regulatory strategy: a Class II recall affecting a multi‑lumen CVC kit was initiated in early 2026 due to supplier-related issues, and European standards (prEN ISO 10555-3, 2026) now specify testing requirements for single‑use sterile CVCs, including tensile force criteria. These developments increase the commercial premium for suppliers with robust supplier auditing, rapid corrective-action protocols and broad conformity testing documented in sales packages.

2026 strategic playbook — prioritized, actionable moves

- Immediate (0–6 months)

- Audit suppliers and contract manufacturers against the new prEN ISO test expectations and create a prioritized remediation tracker for nonconformances.

- Fast‑track a small set of pragmatic clinical studies that target measurable outcomes (reduction in CLABSI, insertion time, line occlusion rates) to support tender responses.

- Run scenario stress tests on supply continuity for key components; qualify secondary sources for critical inputs.

- Near term (6–18 months)

- Refine product portfolio: double down on insertion-system combos and value-added consumables that shorten procedures and reduce downstream costs.

- Explore bolt-on acquisitions or licensing deals to acquire antimicrobial coatings, securement or insertion-system IP rather than building from scratch.

- Deploy field economics tools (hospital ROI calculators) to standardize value communication and accelerate procurement decisions.

- Medium term (18–36 months)

- Shape category standards by participating in consensus bodies and publishing real-world evidence that supports your differentiated claims.

- Implement value-based contracting pilots with high-volume hospital systems where pricing offsets are tied to infection-rate reductions and device utilization metrics.

How to use the full PW Consulting report for 2026 planning

Our complete study includes the detailed segmentation matrices, regional and product-split models, company scorecards and an interactive Excel model that exports scenario outputs for board-level planning. If you are making decisions about R&D prioritization, commercial investments, M&A targeting, or regulatory compliance for 2026 budgets, the full dataset and playbooks will convert strategic intent into executable programs.

Contact PW Consulting to obtain the full report and the accompanying toolkit: scenario workbooks, product adoption roadmaps, procurement playbooks and competitor benchmarking. The market is growing, standards are tightening, and first-mover advantage will accrue to organizations that can operationalize evidence, quality and supply resilience at scale.

For detailed analysis of this topic, please visit the official page:Central Venous Catheters Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com