Panoramic Camera Market Share 2026: Competitive Landscape and Growth Outlook

Other |

2026-02-24 09:15:24

As senior industry analyst at PW Consulting, I present a focused orientation to our latest Quick Service Restaurant (QSR) IT Market study — a strategic briefing intended to clarify the choices that will determine winners and laggards in 2026. The market has moved from recovery into structural expansion; our modelling shows the QSR IT opportunity accelerating through the rest of the decade on a sustained double-digit-value curve (9.0% CAGR across the forecast horizon). From a practical perspective, the study is designed to translate growth trajectories into investment theses, partnership priorities, and operational playbooks that enterprise leaders can execute against this year.

Quick Service Restaurant (QSR) IT Market

2025 was a pivotal base year: the market has grown materially since 2020 and is now positioned for a step-change as automation, cloud-native operations, and new ordering modalities (drive-thru, kiosks, voice, mobile) converge. For executives deciding how to allocate scarce capital in 2026 — whether to re-platform legacy POS instances, pilot edge AI for drive-thru throughput, or pursue tuck-in M&A to secure last-mile logistics integrations — the right dataset shortens cycles and reduces execution risk.

Quick Service Restaurant (QSR) IT Market

Between 2020 and our 2025 base year, the QSR IT market expanded significantly, reflecting both demand-side digitalization and supply-side innovation. That momentum is not a simple rebound; rather, it signals structural adoption across hardware, software, and managed services. Projected forward, our forecast shows the market continuing to expand to nearly double the 2025 level over the forecast window under a central 9.0% CAGR — a pace that requires commensurate attention to scalability, interoperability, and cost discipline.

Quick Service Restaurant (QSR) IT Market

What does this growth imply for 2026 decisions? First, vendor lock-in risk rises as platforms aggregate more customer data and operational control; companies should favor modular integrations and clear data ownership clauses. Second, the financial math for technology-enabled labor substitution becomes compelling for high-volume locations — but only when paired with measurement frameworks that account for change management costs and guest experience impacts. Finally, capital planning must factor in an environment of higher hardware refresh cadence as restaurants adopt digital menus, kiosks, and IoT-enabled kitchen devices.

To preserve competitive value for our clients, the report includes detailed segmentation, region-by-region rollout economics, and proprietary unit-level modelling available only within the full report. This briefing intentionally highlights strategic takeaways while directing readers to the full release for granular allocations and channel breakdowns.

The vendor ecosystem in QSR IT is heterogeneous: cloud-native POS platforms, hardware specialists, enterprise hospitality suites, and unified-commerce players all coexist and pursue different go-to-market plays. Our research profiles the leading names and interprets their strategic directions.

Across suppliers, the market balance favors specialization paired with strategic partnerships: vendors that combine platform capabilities with third-party ecosystems (payments, loyalty, third-party delivery APIs, and AI services) are creating defensible commercial propositions without requiring tight single-vendor lock-in.

Two external forces are particularly important for 2026 planning:

These dynamics favor solutions that are modular, instrumented, and finance-friendly. Capital-light subscription models and vendor-financed hardware refreshes will remain attractive as franchisors look to reduce upfront burdens on franchisees.

Beyond headline projections, our full study contains proprietary unit economics models cross-walked to real-world operator archetypes, M&A screens calibrated to strategic fit, and executable transition plans for converting pilots into system-wide rollouts. We also include buyer negotiation playbooks and sample legal clauses aimed at preserving franchisee interests while enabling enterprise-level standardization.

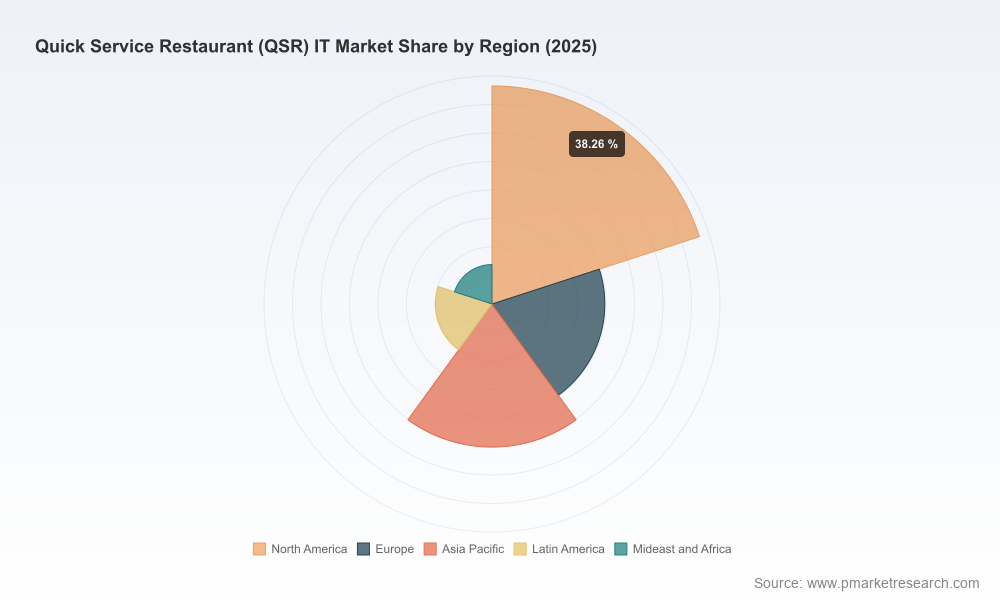

This briefing intentionally omits the detailed segment and regional splits — those granular allocations, vendor share matrices, and unit-level ROI tables are part of the full report and client dashboards. If your 2026 plan depends on precise channel-by-channel sizing, competitive share by sub-region, or detailed supplier scorecards, the full PW Consulting deliverable provides the depth required to operationalize those decisions.

For executive teams and investment committees: use our top-line scenarios to set guardrails for 2026 technology spend and to define the go/no-go criteria for strategic pilots. For vendor and channel leaders: align product roadmaps to enterprise demand drivers identified in the report — particularly around drive-thru throughput, AI-enabled ordering, and payments integration. If you’d like an executive briefing or a tailored workshop to convert these insights into an action plan for 2026, PW Consulting can provide a condensed implementation roadmap and modeling session.

Our market intelligence is built to be immediately actionable while preserving the confidentiality and commercial nuance that senior leaders require. The full report contains the segmentation and tactical guidance necessary to make binding decisions; consider this briefing the strategic trailer — watch it, then access the full release to execute.

For detailed analysis of this topic, please visit the official page:Quick Service Restaurant (QSR) IT Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com