Managed File Transfer Software Market: Strategic Preview for 2026 Decisions

As enterprises confront accelerated digital collaboration, stricter cross‑border data rules, and a rising threat landscape, Managed File Transfer (MFT) is no longer a back‑office commodity — it is a strategic control point. This preview, produced by PW Consulting’s industry practice, synthesizes the headline market trajectory, competitive tensions, regulatory inflection points, and the practical decision framework procurement and architecture teams must use in 2026. It is designed to demonstrate the analytic depth of our full study while reserving detailed segment-level tables and vendor scorecards for report subscribers.

Managed File Transfer Software Market

Market trajectory at a glance (macro only)

The global MFT market has moved from a niche infrastructure category toward an essential enterprise integration and compliance layer. Our consolidated market model shows steady expansion across the historical window (2020–2025), and a continuation of that trend through the forecast horizon (2026–2032). Key macro indicators to anchor decision-making in 2026:

Managed File Transfer Software Market

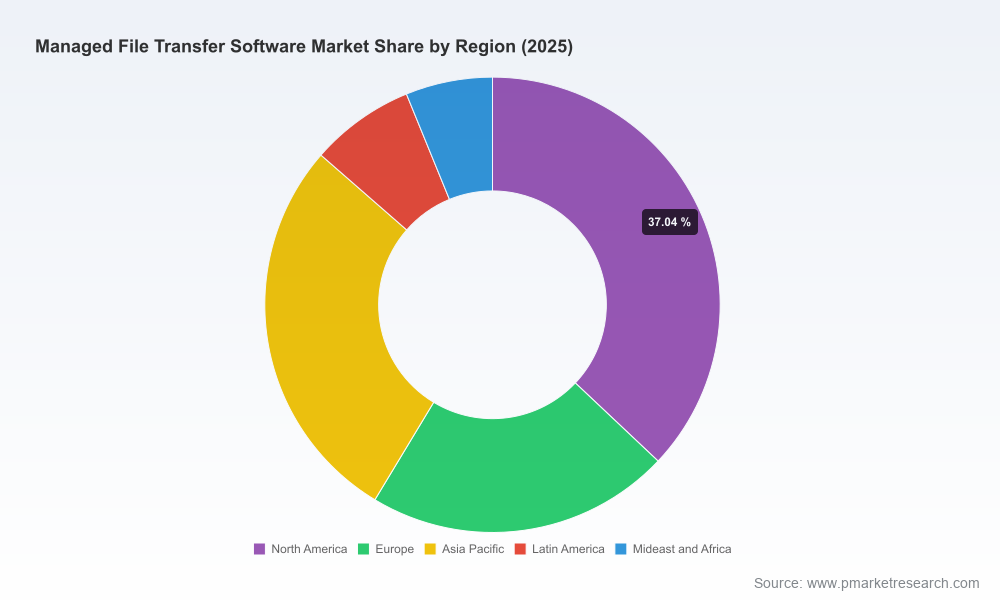

- Base year (2025) market size: USD 1.62 Billion.

- Near‑term projection (2026): USD 1.81 Billion.

- Forecast outlook to 2032: USD 3.21 Billion.

- Compound annual growth rate (CAGR) across the forecast period: 10.4%.

These aggregate numbers reflect accelerating adoption of cloud‑delivered MFT, expanded use across regulated verticals, and rising demand for automation and demonstrable compliance. Use them as a planning baseline: 2026 procurement roadmaps should assume materially higher transaction volumes and stricter audit requirements than those contemplated three years prior.

Managed File Transfer Software Market

Why this matters for 2026 enterprise decisions

- Regulatory urgency has changed procurement priorities. High‑profile enforcement actions and national privacy laws are increasing the cost of non‑compliance and pushing enterprises toward platforms that embed compliance templates, automated logging, and real‑time incident response.

- Cloud acceleration is shifting TCO calculus. Organizations evaluating MFT must weigh reduced CAPEX and operational overhead from SaaS models against data‑sovereignty, latency, and integration constraints that still favor on‑premise or hybrid approaches for mission‑critical flows.

- Operational resilience and automation are now table stakes. Buyers expect workflow orchestration, end‑to‑end visibility, and automated remediation — elements that materially reduce manual effort and incident exposure.

- Security is a procurement differentiator. Platform features such as anti‑malware scanning, FIPS‑validated crypto, AS4 support, and fine‑grained key management are business requirements in regulated industries.

What the full PW Consulting report contains (practical, operational outputs)

The full study is structured as an operator’s playbook for CIOs, security leaders, procurement teams, and partners. Highlights include:

- Executive market synthesis and scenario modelling (base, conservative, upside) that link adoption curves to operational metrics and expected transaction growth.

- Vendor evaluation framework and scorecards that rate providers across security, automation, cloud maturity, integration APIs, managed services, and vertical specialization.

- Deployment decision tools: on‑premise vs. cloud vs. hybrid decision matrix, migration playbooks, cutover risk assessments, and sample runbooks for common enterprise transitions.

- Commercial models and TCO templates (editable spreadsheets) that quantify capex/opex tradeoffs, migration costs, and expected ROI based on consumption and SLA tiers.

- Compliance and audit toolkit: pre‑built templates for GDPR, HIPAA, SOC 2, ISO 27001, and local data‑sovereignty clauses; sample RFP language and contractual protections.

- Use‑case mapping and buyer personas: transaction profiles for regulated finance, healthcare, media, manufacturing, and high‑volume B2B exchange scenarios — plus recommended architecture patterns for each.

- Risk register and mitigation playbook covering supply‑chain risks, third‑party vendor controls, and incident response integration with SIEM/SOAR platforms.

Each deliverable is oriented toward executable decisions: what to pilot, how to de‑risk go‑live, and which commercial levers to negotiate in 2026 contracts.

Competitive landscape — current structure and what to watch

The MFT market exhibits moderate concentration: a small group of global incumbents competes alongside a diverse set of regional specialists and vertical‑focused SaaS providers. Top vendors account for a substantial portion of enterprise deployments, but market share is diffuse enough that differentiation — not scale alone — wins deals. The competitive dynamic in 2025–2026 is defined by three parallel plays:

- Large platform vendors pushing integrated B2B/Integration suites and cloud storage integration as part of broader enterprise portfolios.

- SaaS‑native players and media/creative specialists offering high‑performance, automated transfers tailored to large files and complex workflows.

- System integrators and managed services providers packaging MFT as a service (MFTaaS), combining deployment, management, and compliance guarantees for regulated buyers.

Recent vendor moves underscore how competitive advantage is increasingly defined by automation, compliance templates, and cloud delivery economics.

Vendor snapshots — positioning and implications

- Axway (Paris): Offers enterprise MFT platforms with advanced automation and centralized operations tooling; recent launches enhance operational visibility for SecureTransport and Transfer CFT — appealing to large enterprises that need centralized control across hybrid estates.

- Progress Software (Burlington, MA): Delivers MOVEit and the newer Automate MFT SaaS offerings; strong emphasis on usability, compliance, and AI‑assisted workflows — targeting organizations seeking rapid SaaS migrations with lower manual overhead.

- OpenText (Waterloo): Positions MFT within a broad Business Network/Information Exchange stack; favors buyers prioritizing large B2B partner ecosystems and integrated document flows.

- Software AG (Darmstadt): Integrates MFT into the webMethods integration platform, useful for buyers looking to consolidate integration and transfer capabilities under a single middleware.

- Oracle (Austin): Leverages cloud storage and OCI capabilities to offer managed transfer services for cloud‑native adopters focused on large scale and global reach.

- IBM (Armonk): Offers Sterling File Gateway with strengths in enterprise integration and deep compatibility with legacy ecosystems.

- Signiant (New York): Differentiates through high‑speed, SaaS‑based transfers for media and entertainment use cases where throughput and automation are prioritized.

- Wipro (Bengaluru): Competes with MFTaaS offerings, coupling managed services with cloud delivery to appeal to buyers aiming to shift operational burden off‑premise.

- JSCAPE (Dublin), Fortra (Minneapolis), Coviant, Kiteworks, GlobalSCAPE, Boomi, MetaDefender (OPSWAT): These vendors represent a mix of focused MFT servers, compliance‑centric platforms, iPaaS‑integrated solutions, and security‑first transfers — each attractive to specific verticals or workflow requirements.

For buyers, the implication is clear: evaluate vendors not only on functionality but on the ecosystem fit (integration, SI/partner network), delivery model (managed vs. self‑hosted), and the provider’s roadmap on automation and compliance accelerators.

Recent product and market developments to factor into 2026 plans

- Progress’s 2025 launches upgraded MOVEit and introduced Automate MFT as a next‑gen SaaS platform — signaling stronger cloud push and workflow automation capabilities among market leaders.

- Axway’s early‑2025 Workbench release enhances operational visibility and centralized automation control for enterprise MFT portfolios.

- Wipro’s cloud MFTaaS entry explicitly targets enterprises shifting to managed models to reduce CAPEX and simplify audits.

- OPSWAT’s MetaDefender releases underscore the increasing expectation that MFT platforms incorporate malware scanning and advanced content inspection as default controls.

Strategic decision framework for 2026 (what procurement and architecture teams should do now)

- Start with a compliance‑first requirements capture: map data flows to applicable laws (GDPR, HIPAA, LGPD, new national laws) and define controls required for automation and evidence collection.

- Run a hybrid pilot: validate both SaaS and on‑prem connectors in a production‑like pilot that measures latency, throughput, and audit/report fidelity under expected load.

- Demand operational SLAs and observability: prioritize platforms with built‑in logs, SIEM integration, and automated incident response to cut breach notification costs and protect brand equity.

- Negotiate commercial levers tied to performance and compliance — not just uptime. Include audit rights, data‑residency commitments, and rollback pathways in contracts.

- Plan migration in phases: shore up critical regulated flows first, then migrate bulk B2B exchanges. Use gateway patterns to minimize partner disruption.

- Assess vendor ecosystem and services: picks that look attractive on feature lists may lack partner ecosystems necessary for global rollouts; check regional support and certified integrators.

Risks and tailwinds

- Regulatory enforcement and fines are an accelerating risk — recent high‑visibility enforcement actions have raised boardroom attention to transfer controls.

- Cloud adoption and SaaS economics are a tailwind for faster deployments, but data sovereignty laws and latency requirements preserve demand for hybrid architectures.

- Automation and AI‑assisted orchestration are reducing manual operational costs, creating displacement pressure among legacy operators and opening opportunities for new entrants.

- Market consolidation could compress choice for buyers, increasing the importance of contractual protections and exit planning.

Next steps and how PW Consulting helps

This preview highlights the strategic considerations C‑suite and procurement teams must internalize in 2026. PW Consulting’s full Managed File Transfer Software Market report expands each theme into actionable modules: granular regional and vertical segmentation, vendor scorecards, downloadable TCO models, RFP templates, migration runbooks, and an interactive scenario tool that quantifies the impact of regulatory and architecture choices on cost and risk.

To access the detailed segment tables, vendor rankings, and executable templates referenced here, consult the full report and accompanying toolset available through our research portal.

For detailed analysis of this topic, please visit the official page:Managed File Transfer Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com