Amniocentesis Needle Market Growth Driven by Advancements in Prenatal Diagnostics

Other |

2026-06-17 05:17:00

This briefing distills the strategic implications of PW Consulting’s full Image Editing Software Market study for executives and boards preparing major decisions in 2026. It highlights the macro trajectory, competitive fault-lines, and the practical levers business leaders must consider—while intentionally withholding the granular regional and application splits that are available in the full report. Use this as a high-fidelity orientation to decide whether you need the complete dataset and playbooks to execute faster and with lower risk.

Image Editing Software Market

Timing: With 2025 as the base year and the forecast horizon running through 2032, the study translates recent structural change (AI, cloud, mobile adoption, and new business models) into forward-looking choices aligned to the next major investment cycle.

Image Editing Software Market

Signal-to-noise: The market’s multi-year direction is now clearer—our model shows a robust expansion from the mid-2020s into the early 2030s supported by a compounded annual growth rate (CAGR) of 6.98% across the forecast window. That growth converts into materially larger addressable opportunities for incumbents and challengers alike.

Image Editing Software Market

Decision topology: The report maps decisions across product roadmaps, pricing & packaging, GTM partnerships, M&A prioritization, channel economics, and enterprise procurement—areas where timing and sequencing materially affect value capture.

PW Consulting’s top-line sizing anchors strategy conversations. The base-year snapshot (2025) establishes the market scale and we trace a continuous expansion from the 2020 baseline through the 2025 anchor and into the 2026–2032 forecast horizon. The model demonstrates consistent annual growth since 2020 and projects continued acceleration into the early 2030s, reaching materially higher aggregate revenues by 2032 under a central-case CAGR of 6.98% (USD, revenue unit = Million). This trajectory validates continued investment in core editing capabilities, adjacent services, and AI-enabled feature sets while also exposing where competitive pressure will concentrate.

Comprehensive market sizing and a granular forecasting model (downloadable Excel) with base-year calibration, confidence intervals, and scenario toggles (high/low technology adoption, subscription vs. perpetual licensing mix, and regional demand shifts).

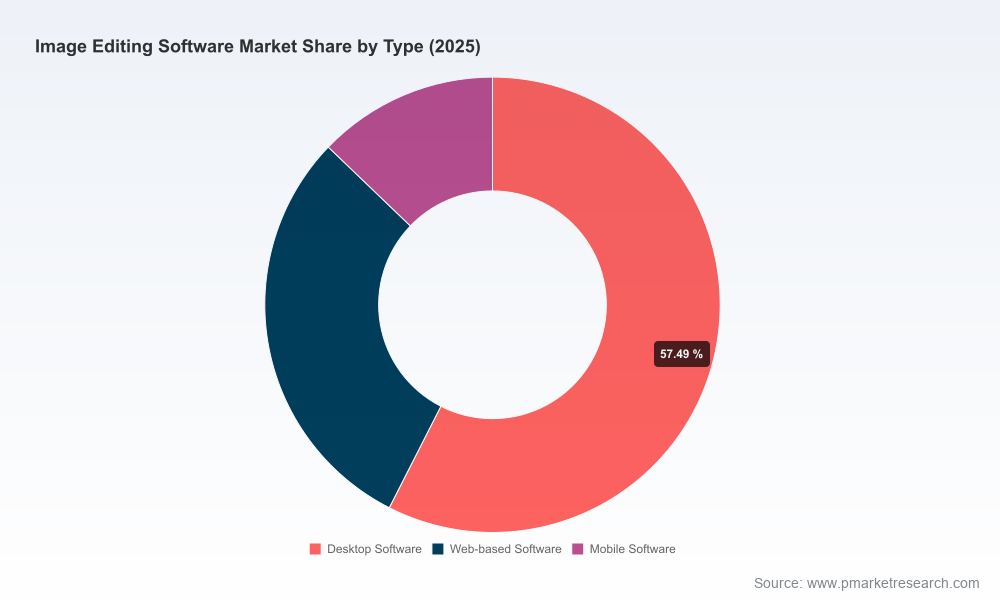

Segment-level demand drivers and adoption curves across usage types, deployment models, and customer archetypes (note: the public brief intentionally omits detailed segment splits—these are included in the full deliverable).

Vendor landscape: capability matrices, financial proxies, technology roadmaps, and product overlap heatmaps that support competitive response planning or M&A diligence.

Commercial playbooks: recommended pricing architectures, go-to-market bundles, channel incentive structures, and enterprise procurement negotiation levers.

Scenario and sensitivity analyses: impact on revenue, margin, and customer lifetime value under alternative assumptions for AI adoption, open‑source pressure, and subscription churn.

Primary research appendices: selected interview excerpts, structured survey results, and benchmarking templates for vendor and asset-level evaluation.

The market sits between established platform incumbents, specialized professional tools, and lively open-source and challenger ecosystems. Market concentration is non-trivial—our concentration metrics indicate that the top-three players control a significant portion of market value and the top-five amplify that share considerably—creating a dual dynamic where strategic scale and niche differentiation both matter.

Adobe Systems Inc. (San Jose, California) – The clear reference player. Adobe’s portfolio remains the benchmark for professional capability, and its subscription-based Creative Cloud continues to shape customer expectations for continuous updates and integrated workflows. Adobe’s recent product cadence—most notably updates that integrate generative AI into consumer and professional offering lines—forces peer vendors to match functionality or find defensible niche value.

Corel Corporation (Ottawa, Canada) – A mature vector and image toolset provider that competes on workflow ergonomics and legacy customer relationships. Corel’s strategic options include deeper vertical specialization and tighter OEM/channel partnerships.

Serif (Nottingham, UK) – A disruptive product strategy that pursued consolidation of photo, vector and layout editing into a single, highly capable application and took an aggressive pricing/availability stance in late 2025. This move shifts the competitive set by lowering switching friction for price-sensitive pros and SMBs.

ACD Systems, CyberLink, ON1, Skylum, Zoner, Capture One – These vendors represent the middle and professional tiers. Their strategic choices (AI differentiation, batch-processing capabilities, RAW processing excellence, or video-photo crossovers) will define whether they consolidate niche segments or become acquisition targets for scale players.

GIMP (global open-source community) – The continued investment in the open-source alternative, including multiple releases across 2025–2026 that improved stability and usability, increases baseline competitive pressure and influences enterprise procurement debates about TCO and lock-in.

Product cadence matters: notable product releases and updates across 2025–2026 (both from commercial vendors and open-source projects) demonstrate an arms race in usability and AI-assisted features. Expect frequent, incremental innovations rather than sporadic large-bang releases.

Open-source velocity: multiple major updates to the leading open-source editor over 2025–2026 improved stability and UX. For product and procurement teams, that changes the baseline expectations for interoperability and cost evaluation.

Pricing and distribution disruption: one vendor’s decision to make a professional-grade, all-in-one app widely available at no cost in late 2025 is the kind of tactical move that forces incumbents to reassess segmentation and bundling strategies—especially for SMBs and freelancers.

Product & R&D: Prioritize pragmatic AI integration (assistants, templating, automated workflows) that reduces user time-to-outcome more than flashy one-off features. Differentiate by workflow integration (camera-to-cloud, plugin ecosystems) rather than feature parity alone.

Monetization: Reassess subscription tiers and entry points. Adobe’s subscription-first model continues to influence buyer expectations; companies without recurring revenue should model subscription migration impacts on CAC payback and churn. Use our scenario model to stress-test cash flow across licensing transitions.

Go‑to‑market: Invest in verticalized partnerships (photography studios, marketing agencies, device OEMs) and developer ecosystems to lock in workflows. Channel economics and partner enablement often yield better margin defense than pure price competition.

M&A & corporate development: Seek targets that either close capability gaps (RAW engines, AI components, cloud infrastructure) or provide defensible niches (high-value vertical workflows). Our report ranks targets by strategic fit, integration complexity, and expected revenue uplift.

Cost & talent: The broader design and editing software industry has experienced material labor- and service-cost pressure; firms must optimize hybrid delivery models and invest in productivity tooling to protect margins as they scale.

Risk management: Prepare for regulatory and IP scrutiny around generative content and derivative works. Additionally, model downside scenarios tied to rapid open-source feature adoption and to faster-than-expected commoditization of certain editing capabilities.

Use this briefing to orient strategic debates and to prioritize internal analyses during 2026 planning cycles. If your decisions include any of the following, request the full report and model:

You are evaluating a pricing transition from perpetual licenses to subscription or hybrid models and need cash-flow impact modeling.

Your M&A screening requires ranked targets with pro forma revenue projections and integration risk assessments.

You need regional and application-level demand curves, channel margin waterfall models, or granular vendor market shares to support negotiations or investor diligence.

Your product roadmap must be validated against feature-level adoption elasticities and competitor release timelines.

The Image Editing Software market is entering a consequential phase: steady market growth underpinned by technology-led productivity gains, juxtaposed with intensifying competition from both commercial and open-source players. The 2025 baseline and the 2026–2032 forecast horizon paint a picture of expanding aggregate opportunity—but capturing disproportionate share will require clear choices about product scope, monetization model, channels, and inorganic growth. PW Consulting’s complete study provides the granular splits, scenario models, and vendor scorecards necessary to make those choices defensible. For executives who must convert strategic intent into executable programs in 2026, the full dataset and playbooks materially shorten execution risk and accelerate value capture.

For detailed analysis of this topic, please visit the official page:Image Editing Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com