Cardiac AI Monitoring and Diagnostics Market Value, Growth Drivers, Challenges and Opportunities

Health |

2026-07-03 09:19:29

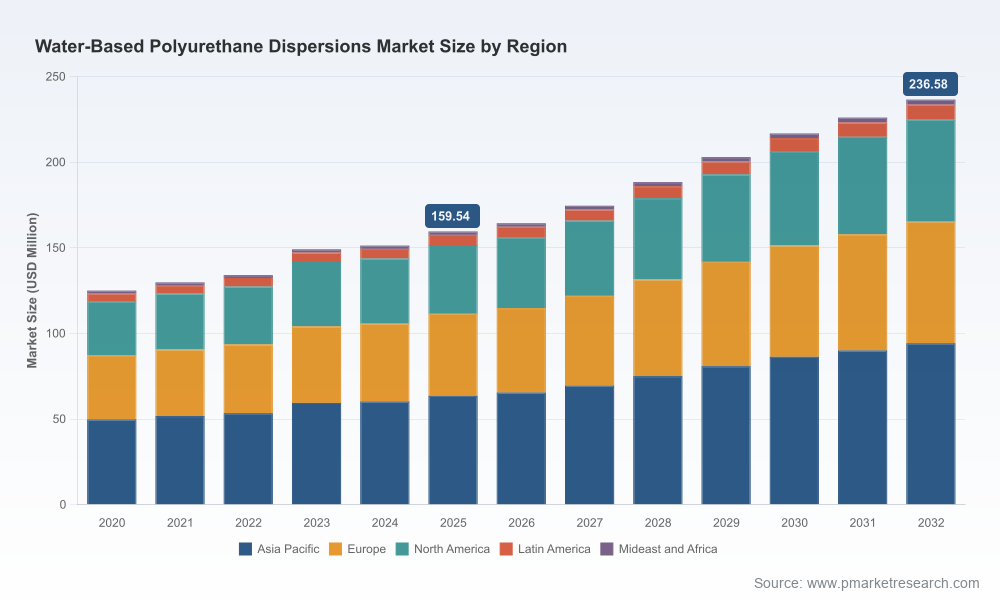

As companies prepare strategic plans for 2026, the water-based polyurethane dispersions (PUDs) market offers a compelling mix of steady growth, regulatory-driven demand shifts, and concentrated industry structure that invites targeted commercial and operational plays. Our analysis shows the global market expanding from an estimated USD 125.0 Million in 2020 to USD 159.54 Million in 2025, with a baseline compounded annual growth rate (CAGR) of approximately 5.9% across the 2026–2032 forecast window. Under this trajectory, PW Consulting projects the market to rise to roughly USD 236.6 Million by 2032, reflecting resilient end‑market demand and ongoing product innovation.

Water-Based Polyurethane Dispersions Market

Budgeting and capital allocation: A mid‑single-digit CAGR in the medium term validates moderate capacity expansions and efficiency investments rather than speculative greenfield bets in most regions.

Water-Based Polyurethane Dispersions Market

Regulatory and product roadmaps: Accelerating low‑VOC requirements and sustainability targets make low‑emission and bio‑based PUD variants not just a compliance choice but a route to price premia and preferred supplier status.

Water-Based Polyurethane Dispersions Market

M&A and partnership strategy: Market concentration metrics (CR3 ≈ 65%, CR5 ≈ 80%) indicate a market where scale and integration matter — attractive for bolt‑on acquisitions, co‑development, and feedstock-secured joint ventures.

The headline growth path masks several practical nuances that should shape 2026 decisions. Volumes are being driven by gradual penetration into flexible coatings, adhesives, and specialty industrial applications where waterborne formulations replace solventborne incumbents. Parallel to volume growth, value migration is occurring as formulators add low‑VOC, mass‑balance, and bio‑based attributes — pulling average selling prices and gross margins upward in targeted segments.

However, the pace of premiumization varies by end use and region. Cost inflation in core feedstocks and evolving regulatory frameworks will create uneven returns across product variants and geographies. Firms that rely on commodity positioning without feedstock integration or clear sustainability differentiation will face margin pressure as input costs and compliance requirements tighten.

Regulatory momentum: Stricter VOC limits in jurisdictions across the US and Europe have accelerated conversion towards low‑VOC waterborne PUDs. This provides both a compliance push and a commercial pull for differentiated formulations that deliver parity in performance.

Feedstock volatility: Recent industry data indicates polyol and isocyanate feedstock price upticks (in the low single‑digit percent range), squeezing margins for non‑integrated producers. This amplifies the advantage for players with upstream positions or long‑dated supply arrangements.

Sustainability premium: Bio‑based polyols and renewable feedstocks are migrating from niche to mainstream for select applications. Buyers in building products, automotive interiors, and premium packaging increasingly demand lifecycle improvements — requiring suppliers to present verified carbon and renewables credentials.

Regional capacity realignment: Geopolitical and trade pressures have catalyzed capacity investments in Asia‑Pacific and other strategic hubs to reduce supply chain exposure. This is reshaping lead times, logistics costs, and competitive dynamics.

The PUD space is dominated by a handful of integrated and specialty players. Scale, application know‑how, and feedstock exposure define competitive advantage. Below are practical implications derived from the profiles and recent moves of core companies active in the market.

BASF SE (Ludwigshafen, Germany): A technology leader with strong architecture in low‑VOC and mass‑balance enabled dispersions. BASF’s orientation towards product platforms and global footprint means competitors should expect sustained investment in premium grades and localized production for market responsiveness.

Covestro AG (Leverkusen, Germany): Known for cohesive product families across coatings and industrial adhesives. Covestro’s emphasis on low‑emission formulations suggests partnerships with downstream formulators and co‑development projects will continue to be an effective route for market penetration.

Dow Inc. (Midland, USA): Integration across polyol and isocyanate chains gives Dow flexibility on pricing and margin management. For mid‑sized players, this argues for long‑term supply agreements, hedging frameworks, or strategic alliances to stabilize feedstock costs.

Lubrizol Corporation (Wickliffe, USA): Focused on high‑value niches such as wood coatings and chemical resistance. Specialist product launches show route‑to‑market via technical differentiation can preserve margin in otherwise competitive categories.

Wanhua Chemical Group (Yantai, China): Recent capacity additions underscore a cost‑competitive, volume‑driven approach. Their upstream MDI integration creates structural advantages on feedstock arbitrage — a salient factor for buyers seeking competitive pricing in volume applications.

Alberdingk Boley GmbH (Krefeld, Germany): A specialist in bio‑based dispersions; well positioned to capitalize on sustainability mandates. Their strategy highlights the premium for renewables‑qualified chemistries and the importance of validated claims.

Hauthaway Corporation, Chase Corporation, UBE Corporation, SIWO US Inc.: These specialty players demonstrate the viability of a focused, application‑led model — delivering tailored PUD solutions for leather, graphic arts, and industrial finishes where customer stickiness is high.

Capacity plays: Wanhua’s large resin complex (completed 2025) and new facilities by major players in Asia and Türkiye indicate an anticipation of sustained demand and a desire to control regional supply chains.

New product introductions: Lubrizol’s recent wood‑protection PUD illustrates tight coupling between formulation innovation and end‑use performance, enabling new value pools in maintenance and premium residential markets.

Facility expansions: Start‑ups of low‑CO2, low‑VOC production lines reflect a broader industrial repositioning to meet regulatory and customer expectations for lower carbon footprints.

Based on quantitative projections and qualitative market intelligence, we recommend the following priority actions for companies making 2026 decisions:

Refine portfolio segmentation: Separate commodity, performance‑differentiated, and sustainability‑branded PUDs in P&L analyses. Allocate R&D and commercial resources disproportionately to margin‑accretive niches that benefit from regulatory tailwinds.

Secure feedstock resilience: Negotiate multi‑year supply contracts, explore upstream integration, and implement dynamic pricing clauses to mitigate short‑term cost volatility.

Invest selectively in regional capacity: Prioritize brownfield expansions near key demand clusters and logistic hubs to shorten lead times and reduce tariff exposure, rather than broad new‑builds unless justified by long‑term offtake.

Accelerate sustainability verification: Move beyond marketing claims — invest in lifecycle analyses, mass‑balance accounting, and third‑party certifications that buyers increasingly require.

Explore M&A and partnerships: Use M&A to acquire application expertise, regional footprint, or feedstock security. Consider JV models with downstream formulators to lock in demand for premium grades.

Operationalize price realization: Implement value‑based pricing frameworks tied to performance and sustainability outcomes, especially for bespoke and premium PUDs.

Our comprehensive market study provides decision‑grade intelligence structured for executives and functional leads. Highlights include:

Granular historical and forecast market sizing (base year 2025; historical 2020–2025; forecast 2026–2032) with scenario modelling across demand, price, and raw‑material pathways.

Detailed segmentation by region, formulation type, and application — delivered with node‑level demand estimates, growth drivers, and margin benchmarks (note: granular node data is available via the full report).

Competitive benchmarking of manufacturers across technology, cost position, and strategic intent — including capability matrices for the major players profiled above.

Supply‑chain risk maps quantifying exposure to feedstock shocks, logistics disruptions, and regulatory changes.

Practical playbooks for growth, margin protection, and sustainability transition — with investment sizing, payback estimates, and prioritized action lists tailored to corporate profiles.

Dealflow and partnership intelligence: curated targets and partnership archetypes for rapid execution of M&A or JV strategies.

Executives should treat our findings as input to three immediate workstreams for 2026: (1) a 24‑month tactical plan that reallocates commercial resources to premium and regulated segments; (2) a 3‑5 year capital allocation plan that sequences expansions and integration; and (3) a sustainability roadmap that converts product claims into verifiable advantages that buyers will reward.

We intentionally present a high‑resolution strategic overlay here while reserving node‑level segmentation tables, price curves, and company‑specific financial impacts for the full report. This preserves the competitive value of the granular insight and ensures direct access to the data that underpins our recommendations.

For teams crafting 2026 strategies, PW Consulting can provide a tailored briefing that maps the report’s findings onto your product portfolio, cost base, and the regulatory footprint of your key markets. Request the full dataset and scenario workbook to convert market insight into executable business plans.

For detailed analysis of this topic, please visit the official page:Water-Based Polyurethane Dispersions Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com