Flat Glass Market Insights into Production Technologies and Supply Dynamics

Other |

2026-06-02 08:05:10

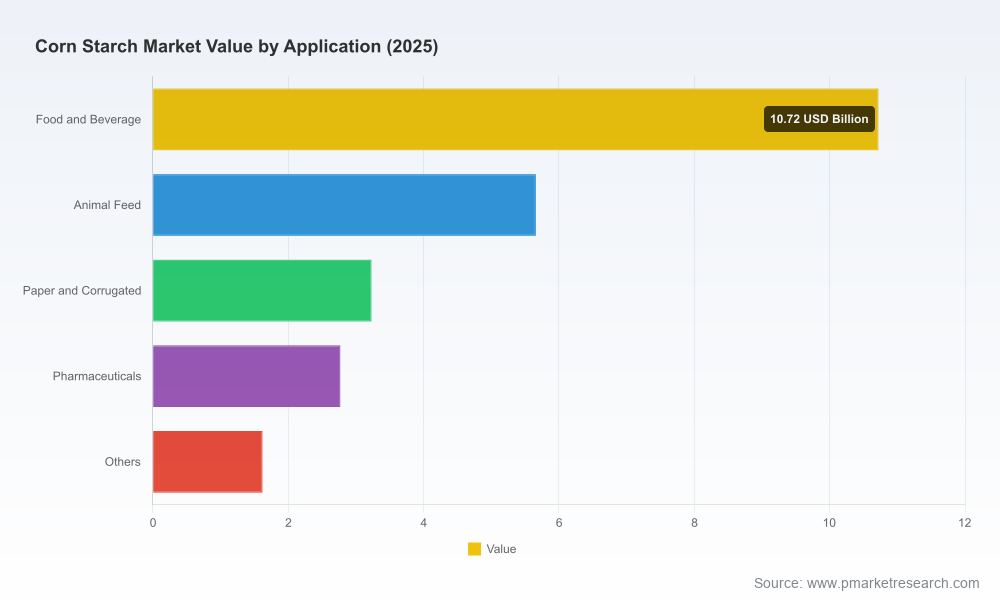

Between 2020 and 2025 the global corn starch market roughly doubled in reported value, accelerating into a structural growth phase. Our base-year analysis (2025) puts global market value at approximately USD 24.0 Billion, and our forecast models project sustained expansion at a compound annual growth rate (CAGR) of 8.1% through 2032, lifting the market to roughly USD 41.4 Billion by the end of the forecast horizon. For 2026 specifically, the study positions the market at the outset of an opportunity window where commodity, regulatory and end-market dynamics converge — producing differentiated opportunities for scale players, specialty manufacturers, downstream formulators and capital allocators.

Corn Starch Market

Portfolio & capital allocation: With an 8.1% CAGR baked into mid-term base cases, every incremental percentage point of share gain translates into material revenue upside. Boards and C-suite teams deciding 2026 capex, M&A and R&D allocations must reconcile near-term commodity tailwinds with durable demand shifts toward specialty and pharma-grade starches.

Corn Starch Market

Procurement & margin management: Volatility in feedstock and freight remains a primary earnings lever. The near-term price environment provides breathing room for margin restoration, but structural hedging and supplier diversification strategies instituted in 2026 will determine who locks in competitive cost curves into the 2027–2030 period.

Corn Starch Market

Regulatory & go-to-market timing: Several regulatory developments — from public procurement bio-preference to pharma excipient guidance — create a narrow window in 2026 to secure certification and partnership advantages that will compound commercial returns through 2028–2030.

Our historic series shows rapid growth from the 2020 base, with value climbing to USD 24.0 Billion in 2025 and following a trajectory that reaches the low‑forty billions by 2032 under our central scenario. That pace implies both continued expansion of traditional end markets (food, feed, paper) and faster adoption in higher-margin segments (specialty food ingredients, pharmaceutical excipients, engineered bio-based products). For executives, the implication is clear: a single, undifferentiated commodity play will underperform. The highest return profiles sit at the intersection of scale, product differentiation and regulatory-compliant manufacturing.

Global integrators (e.g., major agricultural processors): These firms leverage integrated sourcing, broad product portfolios and scale in primary starch production. Their primary advantage is cost leadership and global offtake channels; their strategic playbook for 2026 will be capacity optimization, selective specialty investments and industrial partnerships in fast-growing regions.

Specialty formulators and regional champions: Companies focused on pharma-grade, organic, or functional-modified starches compete on technical expertise, certification and customer intimacy. Expect these players to pursue targeted capacity upgrades and co-development agreements with downstream pharmaceutical and food manufacturers.

Emerging regional players: New capacity announcements and greenfield projects are shifting regional balances. Executives should treat emerging facilities not just as new supply but as strategic assets or competitive threats depending on market access and quality certifications.

Across the competitive set, differentiation increasingly clusters around: (1) certified GMP/ISO facilities for pharma; (2) specialty product portfolios (resistant starches, enzymatically modified waxy variants); and (3) logistics and sustainability credentials that meet public procurement preferences.

Notable capacity additions in 2025–2026 signal targeted expansion into high-value end-markets: announced greenfield capacity in the Gulf region and incremental expansions in North America and Canada are intended to serve pharma, confectionery and specialty tablet markets. These projects are important because they alter regional delivery economics and create faster access to regulated customers.

Investments in North America and South Asia emphasize feedstock integration and downstream partnerships — a defensive response to rising specialty demand and regulatory shifts.

For 2026 planning, companies that move early to secure offtake or co-invest in specialist capacity will gain a first-mover advantage in several regulated end-markets where qualification cycles can take 12–24 months.

Commodity inputs: Corn futures in early 2026 stabilized at levels below the 2022 peaks, providing interim cost relief for processors. This creates a tactical window in which margin recovery or reinvestment into specialty lines is feasible — but management teams should treat the reduction as temporary unless sustained by structural supply changes.

Pharma & excipient rules: Draft and final guidance from key regulatory authorities is tipping procurement toward plant-based, certified excipients. Requirements that incentivize sourcing from certified plant/mineral origins accelerate demand for GMP- and pharma-grade corn starch variants.

Bio-preference and sustainability procurement: Expansions in public bio-preference programs effectively create a price-insensitive volume pool for qualifying suppliers — an underappreciated revenue corridor for compliant producers.

Nutrition policy impacts: Nutritional strategies in major markets are encouraging reformulation away from traditional fats toward carbohydrate-based replacers in some applications. Enzymatically modified and waxy starches are positioned to capture share in reformulation-driven demand.

The PW Consulting study is designed as an operational playbook for 2026 decision-makers. Key deliverables include:

Market structure and valuation model (2020–2032) with scenario-driven downside and upside cases.

Demand-by-end-market modelling and sensitivity analyses (price, feedstock, regulatory adoption rates) — presented as interactive decision matrices that let executives stress-test alternative strategies.

Supplier and asset scorecards: auditing framework for plant certifications, product capabilities and time-to-qualify for regulated customers.

Regulatory risk and opportunities map by jurisdiction, including timelines to compliance and implementation pathways for pharma and public-procurement programs.

Commercial playbooks: go-to-market approaches for specialty starches, recommended channel strategies, sample commercial KPIs and contracting templates.

M&A and partnership screening tool: a prioritized list of asset archetypes and financial thresholds that fit conservative and aggressive inorganic strategies.

Procurement and hedging templates, and a practical 18-month supplier-contingency plan focused on freight, feedstock and energy shocks.

Invest in certification and qualification pipelines now: Securing ISO/GMP and pharma qualification is a multi-quarter process. Companies looking to win in regulated segments should start certification and customer qualification processes in 2026 to capitalize on 2027–2028 demand.

Prioritize specialty R&D and co-development: Allocate a portion of innovation budgets to enzymatic and resistant starch platforms that map directly to reformulation and health positioning in food and pharma applications.

Hedge feedstock with layered strategies: Combine market hedges with physical sourcing contracts and optionality in logistics to lock favorable landed costs without forfeiting upside if corn prices fall further.

Selective capacity plays: Favor bolt-on expansion of specialty capacity over broad-based commodity growth unless supported by long-term offtake commitments.

M&A discipline: Use our screening criteria to identify targets that accelerate entry into regulated markets or provide technological differentiation rather than purely increasing throughput.

The corn starch sector in 2026 is not simply growing — it is fragmenting into clearly differentiated value pools. The economics of generic commodity starch production remain important, but the real upside lies in certified, value-added applications and in capturing institutional bio-preference demand. For executive teams, the difference between a commoditized strategy and a specialty-focused strategy will show up in margin profiles, customer stickiness and resilience to feedstock volatility across the next planning cycle.

PW Consulting’s full Corn Starch Market report contains the granular segmentation, proprietary datasets and executable templates that underpin the insights summarized above. For teams shaping budgets, capex approvals or M&A assessments in 2026, the detailed modelling and supplier-level analysis in the full report are the practical next step to convert the market’s structural tailwinds into defensible shareholder value. Visit our report page for the complete datasets, segmentation tables and bespoke advisory options.

For detailed analysis of this topic, please visit the official page:Corn Starch Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com