Power Inductors Market: Strategic Preview for 2026 Decision‑Makers

Executive synopsis

As electrical systems push for higher efficiency, power density and robustness, the global power inductors market has returned to steady, investment‑grade growth. Our base‑year assessment puts the market at approximately USD 215.0 Million in 2025, following a multi‑year recovery from the 2020 trough. PW Consulting’s forecast through 2032 projects a compound annual growth rate (CAGR) of 5.0%, lifting the market toward a materially larger opportunity by the end of the decade. Market concentration remains meaningful — the top three and top five suppliers control a substantial share of revenues — a structure that shapes supplier bargaining power, innovation cadence and M&A dynamics.

Power Inductors Market

Why this research matters for 2026 decisions

- Boardroom planning: Equip strategic planning cycles with an independent, model‑driven view of where incremental revenue and margin opportunity will arise across the product lifecycle.

- Procurement and supply chain: Quantify exposure to raw‑material volatility and supplier concentration and prioritize mitigation actions that preserve time‑to‑market for new designs.

- Product and engineering: Translate market direction into component roadmaps — where to invest in low‑loss, high‑current, shielded and vehicle‑grade variants to win next‑generation designs.

- M&A and corporate development: Identify the types of targets (technology enablers, regional fill‑ins, niche manufacturers) that accelerate route‑to‑market while managing integration risk in a moderately concentrated sector.

What the report delivers (operational, transaction and go‑to‑market content)

- Top‑down market sizing and 2026–2032 forecast models—transparently modeled by demand drivers, pricing scenarios and sensitivity to raw material inputs.

- Demand driver and use‑case mapping aligned to automotive, consumer electronics, industrial and emerging power architectures, with an emphasis on product form‑factor and electrical tradeoffs.

- Supply‑side diagnostics: supplier cost curves, capacity maps, lead‑time analytics and material sourcing concentration risk assessments.

- Competitive landscaping and company scorecards for established incumbents and fast‑moving specialists, including product positioning, channel strategies and recent R&D/product launches.

- Commercial playbooks for procurement (dual‑sourcing templates, hedging options) and engineering (specification checklists to reduce BOM cost without performance regression).

- Scenario analysis toolkits — stress‑testing revenue and margin under commodity shocks, regulatory constraints and accelerated EV adoption — with recommended tactical countermeasures.

- Transaction support materials: valuation benchmarks, integration risk matrices and a shortlist of acquisition candidates matched to strategic objectives.

Market dynamics and the 2026 risk heat‑map

Three structural dynamics dominate near‑term market behavior and should be central to 2026 planning.

Power Inductors Market

- Raw‑material volatility: Input cost swings have concrete impact on product economics. In recent cycles, metals and specialty powders driving coil and core costs experienced pronounced price and availability shifts, requiring active sourcing and pass‑through pricing mechanisms to defend margins.

- Supply concentration and regulatory friction: Core material supply chains are geographically concentrated, and 2025 policy changes extended lead times for certain ferrite materials—effectively doubling supplier lead times in some cases. That raises the practical cost of single‑source strategies and increases the value of near‑site inventory and qualified alternate materials.

- Product innovation race: The field is bifurcating between ultra‑low loss, ultra‑low resistance components for high‑efficiency converters, and ruggedized, high‑current vehicle‑grade devices. Winning suppliers couple materials expertise with process control and system‑level validation support for OEMs.

Competitive landscape — who shapes the market (and how)

The market structure blends global incumbents with regional specialists. Below are the strategic profiles we analyze in depth in the full report; the preview summarizes their positioning and implications for partners and competitors.

Power Inductors Market

- Bourns Inc (Riverside, CA) — Known for product breadth and strong distribution relationships. Recent launches show a continued focus on shielded designs that combine high thermal and saturation performance with reduced emissions — a direct play into compact, high‑current converter applications.

- Coilcraft Inc (Middletown, IL) — Specialist reputation in low‑loss and precision inductors. The firm’s push into ultra‑low inductance, shielded power parts targets next‑generation DC‑DC converters where switching frequencies and EMI constraints tighten.

- TDK Corporation & Murata Manufacturing (Japan) — Large, diversified component houses that leverage scale and deep materials science for multilayer and thin‑film solutions; they compete on reliability, footprint and supply continuity for high‑volume OEMs.

- Vishay, Wurth Elektronik, Taiyo Yuden — Compete across performance and cost spectrums; recent product moves show emphasis on low RDC, extended temperature operation and manufacturability improvements.

- Eaton, Pulse Electronics, Sumida and specialized US magnetics players — Address industrial, automotive and custom power needs with emphasis on system‑level validation, custom winding and magnetics integration.

- Regional specialists (Codaca, Gowanda, API Delevan, etc.) — Offer vehicle‑grade and high‑current niche products and can be attractive targets for OEMs seeking lower cost or localized sourcing. Recent vehicle‑grade launches highlight the speed at which smaller players can iterate for automotive programs.

We map product announcements, manufacturing footprints and channel strategies into a competitor matrix that highlights where capability gaps and acquisition opportunities exist. The market’s measured concentration (top‑three and top‑five shares) reinforces that partnerships and selective acquisitions are logical levers for firms aiming to scale quickly without compromising margins.

Recent product and supply developments with strategic implications

- Several suppliers announced new shielded, low‑resistance or high‑current families in 2025–2026 — directly addressing the twin market pulls for higher efficiency and higher current handling. Expect OEM design cycles to accelerate around these technologies in 2026.

- Policy‑driven lead‑time expansion for certain ferrite materials has real consequences: qualify alternate core materials early, and build multi‑tier supplier relationships to avoid program slips.

- Metal price volatility (notably in conductor and powder feedstocks) has become a recurring P&L stress; firms that can instrument raw‑material pass‑through clauses or hedge economically will preserve competitive margins.

Actionable recommendations for 2026

- Procurement: Implement a two‑track sourcing strategy — secure critical long‑lead materials under firm contracts while expanding qualified second sources for core powders and wound components.

- Engineering & product: Prioritize modules that reduce BOM sensitivity to scarce materials and that allow platform reuse across automotive and industrial product families. Invest in validation for low‑loss, flat‑wire and shielded designs because these are clear OEM preference vectors.

- Manufacturing footprint: Evaluate partial nearshoring for mission‑critical production to mitigate cross‑border regulatory and logistics risk; where onshore costs are prohibitive, secure capacity via long‑term agreements with high‑quality regional partners.

- M&A & partnerships: Target small, high‑margin specialists that bring material know‑how or vehicle‑grade credentials rather than broad scale bolt‑ons. Consider minority strategic investments to secure preferential supply terms.

- Commercial: Revisit pricing frameworks to include commodity escalation clauses; deploy inventory and lead‑time analytics to optimize safety stock without capital lockup.

How to use the full report

The PW Consulting Power Inductors Market report provides the data, models and strategic templates necessary to turn the insights above into executable plans. The full package includes downloadable spreadsheets with our scenario engine, supplier scorecards, a detailed competitor matrix and an M&A shortlist calibrated to different strategic objectives (scale, capability, regional access).

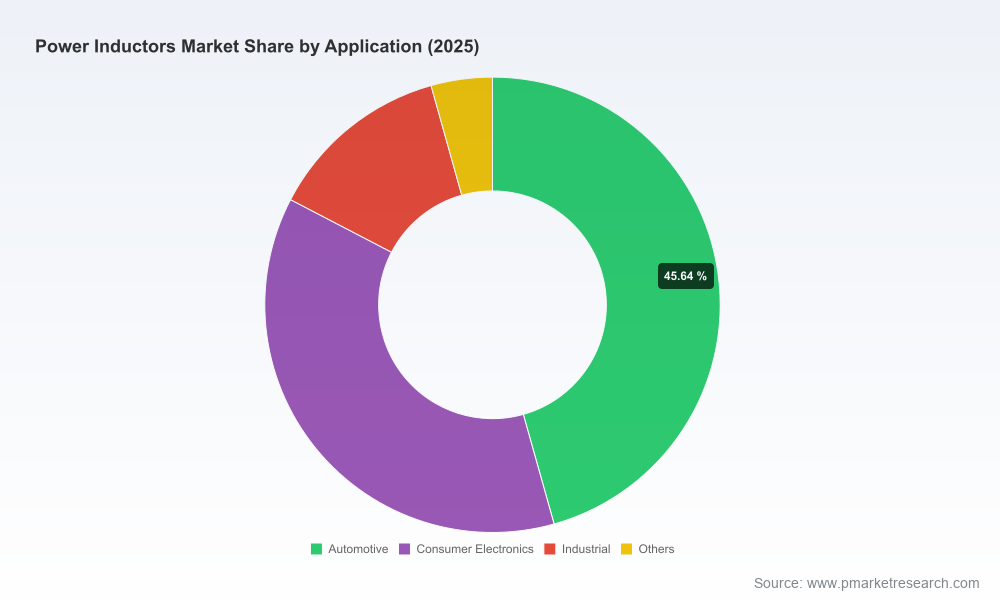

Note: this preview intentionally omits granular regional, type and application breakdowns — those core segmentation tables, SKU‑level maps and regional demand curves are available only in the full report to preserve competitive integrity and to enable our clients to make differentiated decisions.

Next steps

For leadership teams evaluating product roadmaps, procurement portfolios, or transaction strategies in 2026, the full report will supply the actionable intelligence and modeling required to lock in advantage. Contact PW Consulting to request the comprehensive dataset, the scenario toolkit or a bespoke briefing tailored to your strategic questions.

For detailed analysis of this topic, please visit the official page:Power Inductors Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com