New Projects in Shamshabad – Brochure, Pros & Cons, PriceSheet with Detailed Floor Plans | Housiey

Home |

2026-06-23 10:06:19

As PW Consulting’s Senior Strategy Advisor and Head of Industry Analysis, I present a concise, decision-focused preview of our full Triazine Market study (base year 2025; forecast period 2026–2032). This article translates the report’s core strategic implications into pragmatic actions for executives planning their 2026 agendas. We surface the high‑level, data-driven trends that will shape commercial, technical, and M&A choices — while intentionally reserving the granular regional, application and price-by-tier tables for the full report to protect competitive advantage and encourage direct access to our analytical tools.

Triazine Market

Market growth profile: The global triazine market displays steady, mid-single-digit expansion. From a 2020–2025 historical ramp, PwC-calibrated estimates show acceleration into the forecast window with a compound annual growth rate (CAGR) of 6.46% across 2026–2032.

Triazine Market

Scale and momentum: Using 2025 as the analytical base year, the market has moved from a well‑defined five‑hundred‑million dollar scale in 2020 towards clear sub‑billion dollar territory by the end of the forecast horizon. This is a market large enough to justify dedicated product lines and targeted investments, yet not so concentrated as to preclude nimble new entrants with specialized value propositions.

Triazine Market

Concentration snapshot: Market concentration measures indicate a mid‑to‑high oligopolistic structure — a three‑player concentration metric under 50% and a five‑player concentration comfortably above the mid‑50s percent. In practice, this translates into meaningful incumbent influence on pricing and distribution, coupled with space for regional champions and disruptive specialists.

Portfolio prioritization: The triazine family continues to bridge agricultural herbicides and industrial chemistries (notably H2S scavenging and water treatment). In 2026, firms should re-evaluate product portfolios with a two-track mindset — defend legacy ag revenue where regulatory durability exists, while allocating R&D and commercialization resources to higher‑margin industrial and specialty chemistries.

Supply‑chain resilience and feedstock strategy: Volatility in feedstocks (melamine, cyanuric acid, urea feedstocks, chlorine inputs) and regional cost swings require active hedging, supplier diversification, and scenario‑based contract design. Practical moves include multi‑tier sourcing agreements, regional buffer inventories, and joint‑development arrangements with upstream chemical producers.

Regulatory intelligence as a competitive moat: Ongoing regulatory programs (for example, continued EPA monitoring under legacy atrazine frameworks) mean that compliance timelines and residue management are table stakes. Companies that operationalize regulatory foresight — i.e., embed monitoring triggers into portfolio gating criteria — will avoid disruptive delisting or reformatting events.

Commercial go‑to‑market refinement: Precision agriculture and tailored local formulations (e.g., regional crop varietal adaptations) are driving differentiated demand. Sales organizations should segment distributors and OEM partners by solution complexity and invest in digital agronomy tools that demonstrate yield lift and input efficiency to overcome pricing pressure.

M&A and capability plays: Given the market’s moderate concentration, selective bolt‑on acquisitions (regional formulators, specialty H2S scavenger producers, or digital advisory platforms) can rapidly extend capability without the integration risk of mega‑deals. Conversely, strategic divestitures can fund focused investments in high‑growth chemistries.

Transparent methodology: Reproducible market sizing with base year 2025 calibration, historical series (2020–2025), and scenario‑based forecasts through 2032. We describe our demand drivers, elasticity assumptions, and cost pass‑through mechanics in full so clients can test alternate scenarios.

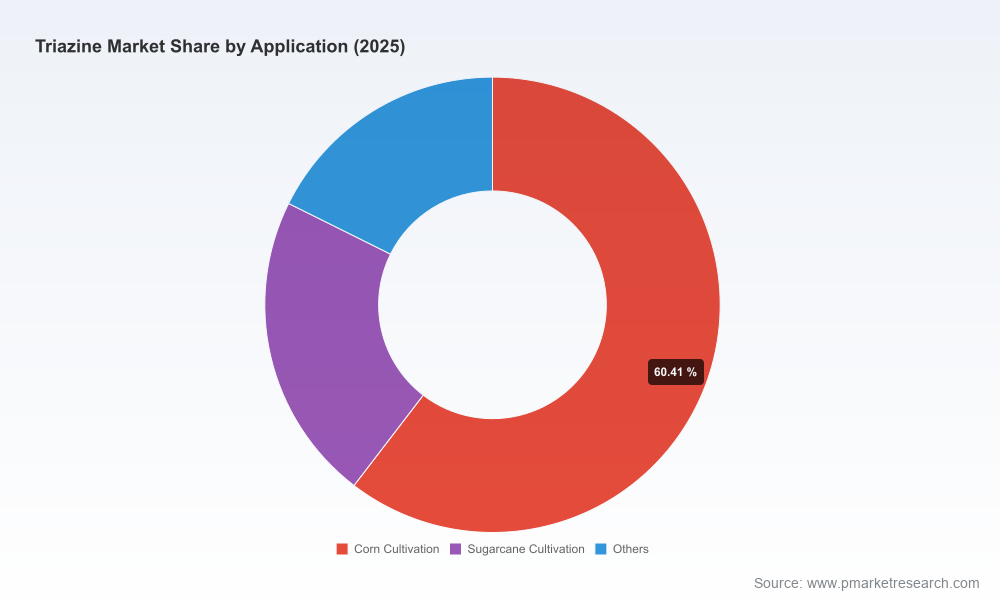

Applied segmentation and playbooks: Actionable segmentation (by product chemistry, applications, and region) linked to go‑to‑market playbooks — including distributor economics, margin waterfall models, and tiered pricing templates. (Note: detailed tables for regional/application splits and price tiers are available in the full deliverable.)

Supply‑demand modelling and sensitivity analysis: SKU‑level production capacity, utilization curves, and short‑term re‑routing maps for feedstock shocks. We include stress tests for sudden export controls, energy shocks, and feedstock outages.

Regulatory & environmental risk matrix: Comprehensive monitoring of active regulatory programs (e.g., ongoing US EPA atrazine oversight), expected review cycles, and a compliance playbook that maps mitigation investments to business outcomes.

Competitive and M&A intelligence pack: Verified profiles for global incumbents, private and listed specialty players, recent transactions and capacity moves, plus a curated list of accretive targets aligned with buyer profiles.

Commercial and R&D roadmaps: Technology adoption timelines (precision ag integrations, formulation advances), recommended R&D experimentation portfolios, and commercialization templates tailored to regional distribution systems.

Interactive tools: Scenario builder, portfolio optimizer, and a short‑listing engine for M&A and partnership targets — all configurable to client risk tolerances and balance sheet constraints.

Our competitive review focuses on the mix of global agrichemical conglomerates, specialty chemicals producers, and oil & gas chemicals suppliers. Key players include legacy agrichemical leaders and diversified chemical companies with complementary industrial applications:

BASF SE (Ludwigshafen, Germany — https://www.basf.com): A long‑standing producer with a global distribution footprint and a recent push toward precision agriculture‑oriented triazine lines. Expect continued investment in formulation and digital advisory bundles to protect ag channels.

Syngenta AG (Basel, Switzerland — https://www.syngenta.com): Strong in crop‑centric solutions, with deep product registration portfolios in key row‑crop markets. Their R&D and field‑trialing focus remain centered on corn and sorghum weed control.

Bayer AG (Leverkusen, Germany — https://www.bayer.com): Leveraging broad crop protection capabilities to combine triazine chemistries with resistance management packages. Expect integrated solutions aimed at preserving long‑term agronomic efficacy.

Dow Chemical Company (Midland, Michigan, USA — https://www.dow.com): Emphasizing local adaptation: expanded R&D and production capabilities in regions such as Brazil to tailor triazine variants to local crop and regulatory needs.

FMC Corporation, Corteva Agriscience, Nufarm, UPL, Adama: These players compete on formulation agility, regional channel strength, and price/performance balance. Their strategies vary from deepening distributor partnerships to co‑development with local seed and service providers.

Hexion Inc., Stepan Company, SLB (Schlumberger Limited), Ecolab: Represent the industrial and oilfield footprint of triazine chemistries — primarily H2S scavengers, desulfurization feedstocks, and water treatment applications. Recent capacity expansions and M&A in production chemicals indicate stronger cross‑industry demand.

Recent industry moves underscore these dynamics: late‑2025 product launches aimed at precision agriculture, capacity and facility expansions in Latin America for localized development, strategic acquisitions to broaden production chemicals capabilities, and capacity increases for H2S scavenger lines. Collectively, these actions point to a bifurcated market — agricultural volumes continue to underpin scale economics, while industrial specialty chemistries present higher margin growth pockets.

Feedstock fluctuations: The 2025 market saw regionally divergent behavior — melamine pricing pressure in Asia and USD‑area price points that require adaptive procurement strategies; cyanuric acid experienced upward pressure tied to urea and energy inputs; cyanuric chloride remained relatively stable against a backdrop of balanced chlorine costs. Each feedstock dynamic has direct margin and availability implications for triazine producers.

Regulatory environment: Ongoing monitoring programs (for example, legacy atrazine regulatory frameworks in the US) and export controls (e.g., selective controls on medium and heavy rare earths enacted by some jurisdictions) raise the importance of proactive regulatory tracking in scenario planning and in supplier selection.

Operational risk: Energy price volatility and regional manufacturing reliability remain the most probable near‑term shocks. Companies with flexible multi‑region production footprints and contractual hedges will outperform peers during episodic stress.

Board-level: Use the market trajectory and concentration indicators to validate mid‑term capital allocation — prioritize bolt‑on acquisitions and capacity shifts that deliver differentiated yields and expedite access to specialty industrial applications.

Commercial teams: Rebuild pricing playbooks that incorporate feedstock pass‑through triggers, channel economics for precision ag platform bundling, and differentiated service tiers for industrial clients (H2S scavenging, water treatment).

R&D and regulatory: Institute cross‑functional review cadences that translate anticipated regulatory milestones into experiment gating and label submission priorities — reducing the likelihood of sudden withdrawal or expensive relabeling.

Supply chain: Shift from tactical sourcing to strategic partnerships with key feedstock suppliers; create capacity rights and flexible take‑or‑pay constructs to smooth raw material swings.

M&A teams: Shortlist acquisition targets using our scorecard for capability gaps (regional reach, specialty chemistries, digital agricultural assets) and run quick synergy models tied to realistic integration timelines.

Triazines present a nuanced opportunity set in 2026: a reliably growing market (6.46% CAGR over the forecast window), substantial incumbent influence, and differentiated pockets of industrial profitability. The right strategic response balances defensive measures in legacy agricultural channels with offensive moves into specialty industrial applications and digital‑enabled commercial models. Our full PW Consulting Triazine Market report contains the granular segmentation tables, price tier sheets, regional share maps, and interactive tools required to translate these high‑level prescriptions into executable 90‑ to 180‑day plans.

For senior leaders preparing budgets and initiatives for 2026, consider this preview your strategic checklist. The complete dataset, scenario models, and executable playbooks are available through the full report — where we keep detailed subsegment disclosure gated to protect client advantage. Contact PW Consulting or visit our report page to access the complete intelligence package and configure a workshop tailored to your company’s risk appetite and growth ambitions.

For detailed analysis of this topic, please visit the official page:Triazine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com