Why Professional Resume Formatting Matters for Job Success

Other |

2026-05-30 06:22:47

As PW Consulting’s lead industry analyst, I present a focused intelligence brief designed to translate our Urea Formaldehyde (UF) Resin Market study into operational decisions for 2026. This introduction highlights the research’s strategic value and actionable directions without reproducing the granular segmented tables found in the full report. Consider it a high-fidelity trailer: enough depth to inform near-term strategy, and a clear signal of where executive teams must direct attention to capture opportunity and mitigate risk.

Urea Formaldehyde Resin Market

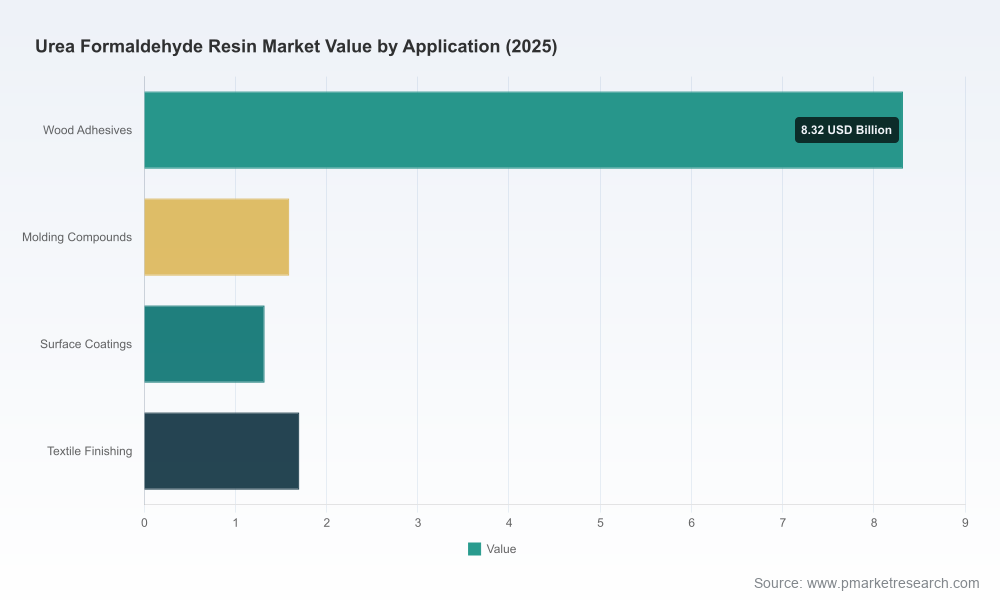

The UF resin market showed steady recovery and modest expansion through the early 2020s, arriving at an estimated market size of approximately USD 12.9 billion in the base year (2025). Our forward view assumes a conservative compound annual growth rate (CAGR) of about 2.0% across the 2026–2032 forecast window, with the market gradually expanding toward the mid-decade and beyond. This growth path reflects a mature industrial chemical market subject to regulatory tightening, feedstock volatility, and incremental product innovation rather than explosive end-market demand.

Urea Formaldehyde Resin Market

Market structure is moderately consolidated: the top three players represent a meaningful share of supply, while the top five increase that share noticeably. For decision-makers, this concentration profile implies that competitive moves from the leading producers materially influence pricing, standards adoption, and innovation diffusion across the value chain.

Urea Formaldehyde Resin Market

Regulatory alignment is no longer optional. Emerging and tightening standards—in particular CARB Phase‑III and US federal composite wood regulations under TSCA Title VI—are enforcing substantial reductions in volatile emissions and formaldehyde limits. Compliance timelines compress product development cycles and force prioritization of low-emission grades and certification-readiness in manufacturing lines.

Input-cost volatility drives margin pressure and strategic hedging needs. Feedstock dynamics remain a dominant variable. Recent snapshots show notable spikes in formaldehyde and resin prices in 2024–2025, underscoring the need for disciplined procurement, indexed contracts, and scenario modeling to preserve margins under stress.

Product premiumization and green differentiation create defensive and offensive playbooks. Customers in wood panels, furniture, and specialty moulding are increasingly substituting toward low-emission or certified grades. Producers that can cost-effectively deliver compliant UF resins—while demonstrating credible sustainability credentials—capture value through price premiums or retained volume under stricter procurement specifications.

Operational and commercial responses must be integrated. Reformulating resins for lower emissions affects raw material mix, process conditions, yield, and waste streams. Procurement, R&D, plant operations and commercial teams must coordinate to avoid cost escalation and downtimes while meeting customer timelines.

The competitive set remains a mix of global chemical majors, specialty resin houses, and integrated panel producers. Several strategic themes emerge from leading players’ positioning.

Ercros — notable for its ErcrosGreen+ UF range that targets ultra‑low formaldehyde emission performance. Positioning emphasizes regulatory compliance (LEF/ULEF/CARB/E0 tiers), which makes Ercros an attractive partner for panel producers transitioning to certified low‑emission portfolios.

Prefere Resins — doubling down on “green chemistry” narratives and CO2 neutrality ambitions, with recent organizational moves to substantiate ESG claims (notably an EcoVadis Gold rating and a group sustainability report). Their emphasis on bio‑based and CO2‑neutral options signals longer‑term product roadmaps oriented toward customers with strict sustainability mandates.

Hexion Inc. — maintains a broad commercial offering with methylated UF grades used in core panel and particleboard applications. Their scale and established customer relationships create inertia that makes them a default supplier for many industrial buyers.

BASF — leverages extensive downstream relationships and branding to promote Urecoll® grades for wood bonding. As a diversified chemical player, BASF can cross‑leverage capabilities in additives, application know‑how, and regulatory advocacy.

Dynea, Advachem, Metadynea — specialty producers focusing on technology and tailored resin recipes for panel adhesives and niche moulding compound needs. Their agility supports faster reformulation cycles and customer trials.

Kronospan — as a major panel manufacturer with in‑house UF resin production, Kronospan exemplifies vertical integration as a strategic hedge against raw material volatility and supply constraints.

Recent corporate developments—especially around sustainability reporting and certification—are not cosmetic. They reshape procurement dynamics: large customers increasingly require third‑party verification, and those suppliers already certified gain competitive access to regulated markets faster.

Compliance cost normalization. Regulatory compliance—across CARB, TSCA, and EU low‑emission frameworks—adds explicit production cost differentials for conventional versus low‑emission UF variants. Our modelling indicates this can increase production costs materially and therefore should be embedded into product costing, pricing, and capex decisions.

Input-price shocks require hedging and redesign. Recent market datapoints documented material price highs for formaldehyde and spot movements for UF resins. Procurement teams should adopt multi‑tiered sourcing, increase use of forward contracts, and evaluate backward integration opportunities where capex and scale rationales exist.

Standards-driven product segmentation. Even in a mature market, product segmentation is now increasingly driven by emissions performance and ESG credentials rather than purely by functional chemistry. This shifts R&D priorities toward low‑emission formulations, alternative crosslinkers and additives, and validated life‑cycle claims.

Prioritize a two‑track product roadmap. Maintain a cost‑competitive conventional line while accelerating development and certification of low‑emission grades. Treat regulatory‑ready SKUs as strategic products with dedicated launch calendars tied to customer conversion targets.

Lock in raw‑material risk management. Move from spot exposure to a mix of index‑linked contracts, strategic inventory cushions, and selective forward purchases. Evaluate partnerships or minority investments with specialty feedstock suppliers to secure preferential allocation in stress scenarios.

Invest selectively in retrofit and capacity rationalization. Converting or retrofitting existing reactors to produce low‑emission grades may be more cost‑effective than greenfield projects. Create a prioritized retrofit roadmap based on plant location, proximity to key customers, and regulatory patchwork risk.

Leverage certification as a commercial asset. Achieve third‑party ESG and emission certifications early where customers demand them; use certification to defend pricing and to pursue new accounts in regulated jurisdictions.

Pursue targeted M&A or JVs. Given moderate market concentration, acquisitive moves can accelerate technology access and geographic reach. Consider bolt‑on acquisitions that add low‑emission formulations, downstream application expertise, or regional fill‑capacity.

Define measurable KPIs for 2026. Track: share of revenue from certified low‑emission products; procurement hedge ratio; product reformulation pipeline milestones; compliance‑ready capacity (tons per month); and customer conversion rate for transition projects.

The complete study provides the granular intelligence required to execute the playbook above. Highlights include:

Full segmentation by region, product type, and application with historical series and forward projections (data tables and interactive charts).

Price and cost modelling for key raw materials, including scenario stress tests and break‑even analyses for low‑emission production routes.

Regulatory impact matrices and a compliance timeline mapped to product and plant implications for all major jurisdictions.

Comparative technology assessments, process‑change cost estimates, and time‑to‑market analyses for reformulation options.

Deep competitive profiles and a transaction pipeline overview, including capability matrices for leading suppliers and integrated panel producers.

Operational playbooks, procurement clause templates, and KPI dashboards that executives can drop into 2026 planning cycles.

For suppliers, customers and investors active in or adjacent to the UF resin ecosystem, 2026 will be a year when regulatory cadence, input‑cost regimes, and sustainability narratives converge to re‑order value capture. The market is not vanishing; it is evolving. Success will accrue to organizations that integrate regulatory readiness, disciplined procurement, and targeted product innovation into a single, measurable strategy.

PW Consulting’s full report contains the dataset, modelling tools, and execution templates needed to move from insight to action. Use this briefing to orient your 2026 playbook — then consult the full study for the granular, transaction‑ready intelligence that converts strategy into measurable outcomes.

For detailed analysis of this topic, please visit the official page:Urea Formaldehyde Resin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com