Lamination Adhesives for Flexible Packaging: Strategic Imperatives for 2026

As companies plan capital allocation, product development and go-to-market strategies for 2026, the lamination adhesives segment for flexible packaging is emerging as a focal point where sustainability regulation, raw material volatility and product differentiation intersect. PW Consulting’s new market study—anchored on a 2025 base year and projecting through 2032—combines quantitative forecasting with actionable strategy playbooks to help executives and investors convert structural trends into defensible competitive advantage.

Lamination Adhesives for Flexible Packaging Market

Why this study matters for 2026 decisions

- Macro trajectory you can act on: The global market for lamination adhesives for flexible packaging expanded from roughly USD 163.15 million in 2020 to USD 212.6 million in 2025, and our base-case forecast (2026–2032) assumes a compound annual growth rate (CAGR) of 5.9%. By 2032 the market is expected to approach USD 312.6 million under the baseline scenario. These aggregate dynamics create a compelling backdrop for investment in new formulations, production capacity and commercial partnerships.

- Timing matters: 2026 sits at the inflection point where regulatory enforcement, Extended Producer Responsibility (EPR) adoption, and producer-level recyclability requirements will materially affect procurement specifications and customer willingness to pay. Companies that align R&D and supply strategies to these regulatory deadlines can convert compliance into revenue differentiation.

- Actionable economics: The study does more than project topline growth—it translates demand scenarios into unit economics, margin impacts and payback periods for capital investments. This enables CFOs and business unit leaders to prioritize initiatives with the highest ROI in the near term (12–18 months) and to stress-test strategic options over the full 2026–2032 horizon.

What the report contains (practical content)

- Demand & Forecast Engine: Granular scenario-based forecasting (base, upside, downside) from 2026–2032, integrating macro drivers such as packaging conversion rates, food & medical packaging trends, and adoption curves for recyclable and compostable laminates.

- Cost & Margin Modelling: A dynamic cost model that maps raw material inputs (resin, solvents, polyurethane precursors), PPI movements and pass-through mechanisms to gross margins at different pricing strategies.

- Regulatory Impact Matrix: Detailed assessment of how state-level EPR laws, recyclability mandates and international standards reshape formulation requirements and permissible adhesives profiles—aligned to procurement timelines used by major CPGs and co-packers.

- Supplier & Product Scorecards: Comparative assessments of adhesive technologies (solvent-based, solventless, water-based, hot/cold-seal and emerging bio-based solutions) using commercial KPIs—performance, cost-to-serve, recyclability, regulatory readiness and supply risk.

- M&A and Partnership Heatmaps: Identification of targets and capabilities that accelerate entry into high-growth subsegments, plus integration playbooks and valuation sensitivities keyed to integration synergies.

- Commercial Playbooks: Go-to-market strategies for niche specialization (e.g., compostable laminating adhesives for flexible food packaging), distributor partnerships, and channel economics for both developed and emerging markets.

- Operational Roadmaps: CapEx sizing and phasing, workforce skill requirements, and pilot-to-scale templates for bringing new solvent-free or compostable adhesive lines online with controlled quality and compliance checks.

Competitive landscape — who matters and why

The market is moderately fragmented: the three- and five-firm concentration ratios indicate meaningful room for differentiation and consolidation. Our study shows a CR3 of approximately 24.6% and a CR5 near 26.2%, signaling that while global leaders are influential, regional and specialist players retain substantial share and strategic flexibility.

Lamination Adhesives for Flexible Packaging Market

- H.B. Fuller Company (United States) — Notable for its Flextra® compostable lamination adhesives and solvent-free polyurethane offerings. Their positioning makes them a leading supplier to brands seeking compliance with recyclability and compostability criteria. Strategic implications: incumbent relationships with packaging converters and early investments in compostable chemistries give them defensive advantages in high-regulation markets.

- Henkel AG & Co. KGaA (Germany) — With the Loctite Liofol portfolio spanning solvent-based, water-based and solvent-free laminating adhesives, Henkel competes across performance and regulatory-focused segments. Strategic implications: breadth of portfolio supports flexible commercial approaches to both price-sensitive and sustainability-led customers.

- Arkema Group / Bostik (France) — Arkema’s 2024 acquisition of Dow's flexible packaging laminating adhesives business consolidated capabilities in solvent-based and solventless systems; Bostik’s packaging adhesives emphasize solvent-free and water-based solutions. Strategic implications: consolidation trends among chemical majors are driving scale and R&D capacity—watch for further bolt-ons that capture pockets of innovation.

- 3M Company (United States), DIC Corporation (Japan), COIM Group (Italy), Flint Group (Germany), Ashland Inc. (United States), Jowat (Germany), Brilliant Polymers (India) — These players collectively illustrate the market’s technological breadth, from high-performance specialty laminating adhesives to regionally optimized eco-conscious formulations. Notably, Brilliant Polymers’ visibility at Interpack 2026 signals that smaller, agile suppliers remain important sources of innovation.

Recent market moves and context

- Deal activity: Arkema’s acquisition (completed December 2024) of a major flexible packaging laminating adhesives business—publicly reported at a significant price point—illustrates strategic consolidation by firms seeking immediate scale in laminating technologies.

- Trade & innovation signals: Specialist firms such as Brilliant Polymers are leveraging trade shows (e.g., Interpack 2026) to showcase next-generation laminating formulations, indicating active product innovation at the edge of the market.

- Input cost volatility: Raw material price swings—notably oil-linked feedstocks—remain the principal near-term earnings risk. The Producer Price Index for Adhesive Manufacturing (Synthetic Resin and Rubber Adhesives) stood at 393.025 in April 2026, reflecting elevated input-cost pressure that will influence pricing strategies and margin management.

- Regulatory tailwinds: Adhesives are increasingly recognized as enablers of recyclability. Compliance with new EPR frameworks is now part of procurement specifications in several U.S. states (California, Oregon, Colorado, Maine, Minnesota, Maryland and Washington), accelerating demand for adhesives that facilitate single-stream recycling and easier delamination where required.

- Industry forums: The World Adhesive & Sealant Conference 2026 and FEICA sessions are focal points for regulatory dialogue and standards-setting, and should be monitored for early indicators of future testing or certification requirements.

Strategic playbook for 2026 — five priorities

- 1. Prioritize regulatory-ready R&D: Accelerate development of solvent-free and compostable formulations that meet both performance and recyclability criteria. Build testing corridors with major converters and CPGs to shorten validation cycles.

- 2. Hedge and localize feedstock exposure: Implement a dual-track procurement strategy—long-term contracts for critical monomers and an agile spot-purchase capability for near-term cost optimization. Evaluate onshore vs. offshore production economics to reduce freight and lead-time risk.

- 3. Targeted M&A and partnerships: Use bolt-on acquisitions or joint ventures to acquire niche chemistries or customer relationships rather than broad generalist acquisitions. Focus on capabilities that close time-to-market gaps (e.g., pilot lines, certification labs).

- 4. Commercial segmentation and value selling: Move from product-only selling to solution-selling—packaging system assurances, recyclability certifications and total cost of ownership (TCO) analyses that justify premium pricing for regulatory-ready adhesives.

- 5. Operational readiness for scale: Invest in modular production assets and quality systems that allow rapid scale-up of validated formulations. Create a regulatory compliance dashboard to ensure alignment across R&D, production and sales functions.

How to use the full PW Consulting study

Executives should treat this study as a decision-support asset: use the cost models to test M&A scenarios, the supplier scorecards to re-run vendor selections under EPR-constrained requirements, and the market forecasts to size investment envelopes for pilot lines and commercial trials. The report includes downloadable templates—capex calculators, RFP language for sustainability specs, and an M&A integration checklist—that translate insight into executable workplans.

Lamination Adhesives for Flexible Packaging Market

Transparency note — what we intentionally withhold here

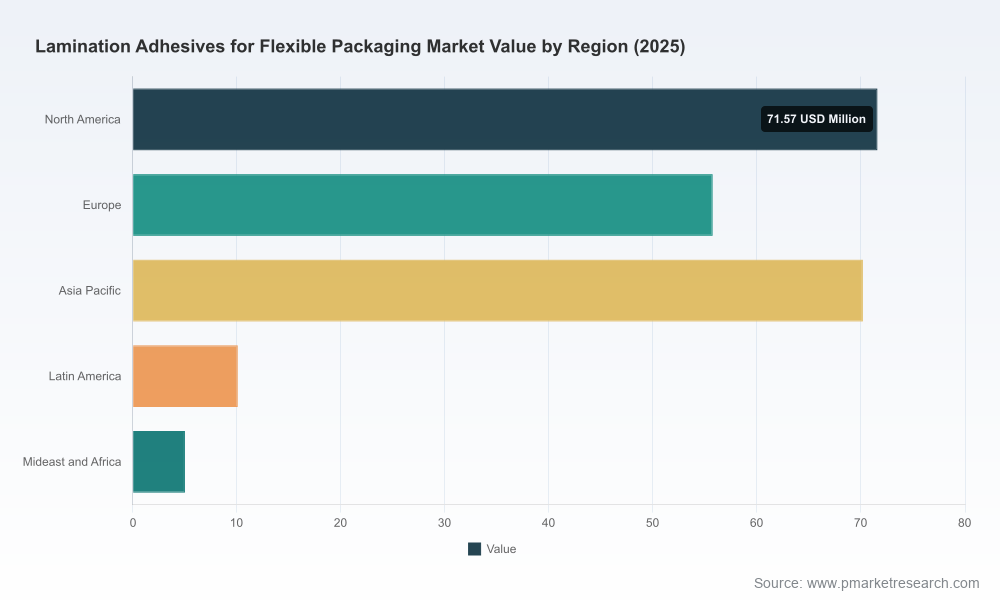

To preserve strategic value for decision-makers and to maintain the “trailer” function of this introduction, we have deliberately not published the detailed regional, type- and application-level revenue splits in this brief. The full dataset—covering granular regional dynamics, product-type shares, and application-level adoption curves—is available in the complete PW Consulting report and includes primary-sourced supplier contracts, converter interviews and proprietary demand elasticities that underpin the forecast scenarios.

Next steps

- For commercial leaders: request the report’s supplier scorecards and the commercial playbook to accelerate customer trials.

- For R&D and product teams: obtain the regulatory impact matrix and test-plan templates to shorten validation cycles with major converters.

- For corporate development: review the M&A heatmap and valuation sensitivities before initiating outreach or competitive bids.

PW Consulting’s full Lamination Adhesives for Flexible Packaging Market study provides the proprietary datasets, scenario models and operational templates that leaders need to make high-confidence decisions for 2026 and beyond. Contact our commercial team to access the complete report and raw data packages that will enable transaction-grade diligence and executable go-to-market blueprints.

For detailed analysis of this topic, please visit the official page:Lamination Adhesives for Flexible Packaging Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com