Slope: The Ultimate Rolling Game That Will Test Your Reflexes

Games |

2026-05-15 07:56:37

As PW Consulting’s senior strategy advisor and chief industry analyst, I present a concise strategic preview that positions the full Spinal Fusion Market report as an operational playbook for 2026 decisions. This piece synthesizes the macro growth trajectory, the regulatory and reimbursement inflection points reshaping the business model, and the competitive dynamics that will determine winners and losers — while intentionally withholding detailed segment breakouts to incentivize access to the full study.

Spinal Fusion Market

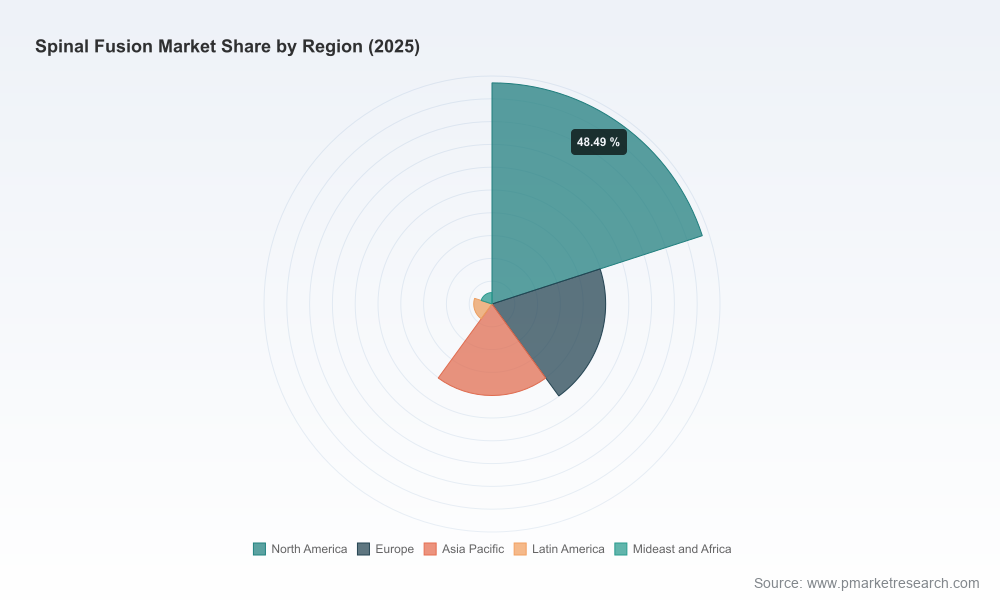

The spinal fusion market is on a sustained growth path: using 2025 as the base year, our market model shows a steady expansion at a compounded annual growth rate (CAGR) of 7.19% over the forecast window (2026–2032). That trajectory reflects structural demand for fusion procedures, continued device innovation, and important shifts in how payers and hospitals reimburse and deliver care. Our forecast maps a clear growth arc from the market’s 2025 baseline to its projected size in 2032, providing a reliable context for capital allocation, product prioritization, and geographic expansion decisions in 2026.

Spinal Fusion Market

Reimbursement reconfiguration: Medicare’s January 2026 revisions — notably the removal of a substantial set of spine and cranial procedures from the Inpatient Only list and the addition of numerous payment codes — materially expand outpatient reimbursement options for spinal fusion. Simultaneously, the 2026 CPT code set includes major updates to SI joint fusion coding. These changes shift economic incentives toward outpatient and ambulatory surgery center (ASC) pathways and demand new coding and evidence-generation strategies from manufacturers.

Spinal Fusion Market

Cost pressure on providers: Hospital costs for inpatient lumbar fusion have escalated dramatically (historical data show a near-tripling across the last two decades), and recent Diagnosis-Related Group (DRG) revisions separating single-level from multilevel fusions increase billing complexity. Health systems are actively seeking lower-cost, higher-throughput solutions, creating commercial openings for devices optimized for same-day or short-stay pathways.

Regulatory momentum and product churn: The past 18 months have seen multiple 510(k) clearances for interbody and stabilization devices and the initiation of pivotal regenerative trials. This wave of clearances and clinical advancement both accelerates product availability and raises the bar for clinical differentiation.

From a strategic planning perspective, the market’s projected growth (CAGR of 7.19% for 2026–2032) provides a predictable backdrop for investment decisions. The expansion is large enough to justify incremental R&D spending and selective M&A, but not so explosive that undifferentiated entrants will thrive without defensible clinical or commercial advantages. In short: scale matters, clinical evidence is currency, and go‑to‑market speed is the differentiator.

The spinal fusion competitive map is concentrated and characterized by a mix of global platform players, specialist innovators, and emerging biologics companies. Market concentration metrics indicate material dominance among the top-tier vendors, a structural reality that shapes price dynamics, distribution access, and consolidation risk.

Medtronic — A platform leader combining a broad fusion portfolio with AI-enabled navigation and bone grafting technologies. Strategic advantage: integrated systems that align with hospital capital investments and digital OR strategies.

Globus Medical — Focused on minimally invasive fusion systems and lateral/ TLIF interbody technologies. Strategic advantage: procedural-enabling implants for ASC and MIS adoption.

Orthofix — Strength in biologics and adjunctive bone growth stimulators, positioning it at the intersection of devices and biologic-mediated outcome improvement.

SI‑BONE — Niche specialist in sacroiliac joint stabilization with an established commercial model for a high-margin, focused therapy.

Small-to-mid innovators (Spine Innovation, Spinal Elements, ChoiceSpine, Highridge Medical, etc.) — These firms are pushing material product innovation (expandable titanium implants, 3D-printed interbody systems, porous cages) and gaining regulatory traction. Recent 2026 clearances and product launches demonstrate accelerating commercialization potential for differentiated implants.

Biologics and regenerative contenders (Theradaptive, Inc.) — With pivotal trial progress for protein‑based fusion enhancers, these companies are potential disruptors if clinical endpoints translate into superior fusion rates and payer-accepted value propositions.

FDA clearances in early 2026 for novel expandable and ALIF systems signal an uptick in device refresh cycles — incumbents will need faster iteration and more compelling clinical data to defend share.

Pivotal trial advancement for a regenerative spinal therapy highlights the growing role of biologics as both product extensions for device companies and acquisition targets for strategic buyers focused on long-term outcomes.

Divestitures and business transactions among major players are changing distribution footprints and creating whitespace for partnership-driven market entry strategies.

Our comprehensive study is designed for commercial and corporate strategy teams who must act in 2026. It contains:

To convert market growth into profitable share gains, firms should execute a focused, sequenced set of initiatives over the next 12–36 months:

Near term (0–12 months): Rebaseline product value propositions for outpatient use; submit updated coding support packages; accelerate limited-market launches to generate real-world evidence; and lock in pricing pilots with high-volume ASCs.

Mid term (12–24 months): Invest in evidence-generation (registries, payer outcomes studies), pursue tuck-in acquisitions that fill capability gaps (navigation, biologics, or MIS-specific implants), and adapt sales compensation to channel shifts.

Longer term (24–60 months): Build integrated offerings combining implants, biologics, navigation, and service models (implant-as-a-service, outcomes warranties) to protect margin against price compression and to leverage the concentrated nature of the market.

This preview outlines the levers at play but intentionally omits the granular segmentation tables and geo‑application breakouts that underpin commercial targeting and M&A valuation. The full PW Consulting Spinal Fusion Market report contains those breakouts, provider-level utilization trends, pricing curves, and a downloadable dataset that supports custom scenario modeling for your business plans.

Market growth provides runway, but 2026’s real opportunity lies in execution: converting reimbursement change into commercial advantage, translating regulatory clearances into differentiated product portfolios, and pairing clinical evidence with novel commercial constructs designed for outpatient care. Companies that align R&D, evidence generation, and channel strategy now will compound presence over the forecast window. For teams responsible for 2026 P&L and three‑year strategic plans, the full PW Consulting report is the operational guidebook that turns market forecasts and regulatory insights into executable, measurable actions.

To access the complete segmentation, provider-level analyses, and the actionable playbooks referenced here, consult the full PW Consulting Spinal Fusion Market report.

For detailed analysis of this topic, please visit the official page:Spinal Fusion Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com