Vegetables and Fruits Market in Middle East and Africa Is Growing Around Food Security Goals

Networking |

2026-05-26 11:28:01

As PW Consulting’s lead industry analyst, I present a focused strategic preview of our full Titanium Dioxide (TiO2) Market study (base year 2025). This brief synthesizes the macro trajectory, structural dynamics, competitive posture, and the practical decisions that should guide corporate boards, investors, and operating units through 2026. The aim is to demonstrate the analytical depth of the full report while preserving the proprietary segmentation and granular forecasts that drive transaction- and operations-level decisions.

Titanium Dioxide (TiO2) Market

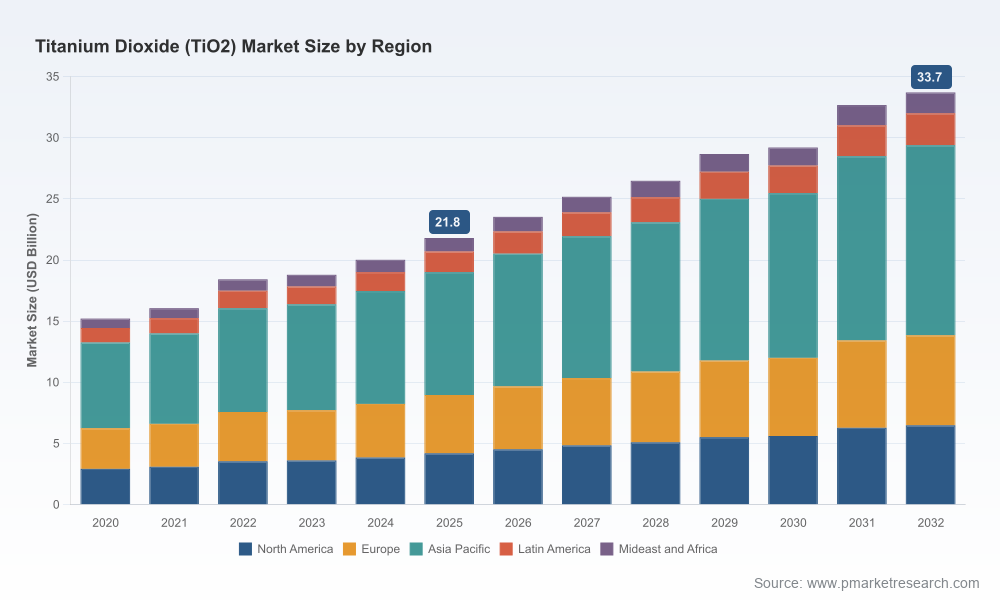

TiO2 has returned to a clear growth path following a cyclical period of demand normalization. Our market-sizing exercise — built on vintage 2020–2025 history and forward-looking modeling — pegs the global TiO2 market at roughly USD 21.8 Billion in 2025. At an expected compounded annual growth rate (CAGR) of approximately 6.5% over our forecast window (2026–2032), the market is projected to approach the low-to-mid thirties (USD 33.7 Billion by 2032). This trajectory is driven by steady end-market recovery in industrial coatings and plastics, alongside structural shifts in feedstock access and sustainability-driven product initiatives.

Titanium Dioxide (TiO2) Market

Macro-to-meso alignment: 2026 will be the first year where post-pandemic demand patterns, elevated regulatory costs, and supply-side restructuring converge. Companies that align commercial strategy (pricing, contract terms) with revised cost curves and sourcing realities will preserve margin and market share.

Titanium Dioxide (TiO2) Market

Regulatory inflection points: Tariff regimes and anti-dumping measures have materially altered cross-border flows. In particular, additional US duties on certain titanium ores and a broader set of duties and anti-dumping measures affecting Chinese-origin material are compressing arbitrage opportunities and increasing landed cost volatility.

Raw material exposure: The upstream market — from ilmenite and rutile mining to synthetic concentrates — is showing signs of stress as environmental constraints and capital discipline reduce the elasticity of supply. For example, US import values for titanium mineral and synthetic concentrates reached a notable level in 2025, underscoring tighter market tightness and increasing strategic importance of feedstock control.

Process bifurcation: Chloride- and sulfate-route production remain the two dominant process archetypes, each with different capex footprints, environmental profiles, and suitability for premium pigment grades. Strategic investments and divestments by leading manufacturers are increasingly process-driven.

Concentration and bargaining power: Market concentration is meaningful but not monopolistic — a mid-range share resides with the largest industrial players. This structure leaves room for both global scale players and regional specialists to exert pricing discipline or pursue niche premium strategies.

Environmental and compliance costs: Tightening environmental regulations on mining, waste disposal, and emissions have increased operating costs for ilmenite producers and pigment manufacturers. These regulatory costs are structural and will continue to influence plant investment, regional competitiveness, and sourcing strategies.

Trade policy as a strategic variable: Tariffs and anti-dumping duties (in the US and EU) are shifting sourcing strategies, prompting near-shoring, supplier diversification, and greater emphasis on secure long-term contracts with reliable upstream partners.

Coatings remain the demand engine, driven by architectural renovation cycles, industrial coatings in infrastructure, and growing performance coatings for automotive and specialty applications.

Plastics demand is benefiting from packaging innovation and higher-performance engineering resins, but remains sensitive to resin prices and substitution dynamics.

Specialty niches — such as high-performance inks, paper, and select cosmetics applications — offer margin pools for innovation (e.g., surface-treated grades, low-impurity pigments, and specialty dispersions).

Sustainability and additives: Market adoption of low-toxicity, low-resin migration, and energy-efficient pigment grades is accelerating product development cycles and opening premium price opportunities for compliant producers.

The industry is anchored by several global and regional leaders with differentiated strategies that span vertical integration, process specialization, and portfolio rationalization. Our full report profiles each major player; below are the strategic takeaways for 2026 planning:

The Chemours Company — A scale leader in chloride-route TiO2 production, focused on premium Ti-Pure™ grades for coatings and plastics. Recent actions include the divestment of a former manufacturing site in Taiwan (announced January 2026), which signals ongoing portfolio optimization and site rationalization to match demand footprints with cost-efficient capacity.

Tronox Holdings plc — A vertically integrated participant with upstream mineral mining and multiple pigment plants. Its control of feedstock supply provides resilience against raw-material shocks, though it faces the same regional regulatory and logistics challenges as peers.

Venator Materials plc — Positioned as a pigment and additives specialist, Venator continues to refine its asset base and product portfolio. Recent activity includes a site sale in the UK (October 2025) and a product launch (May 2025) for a TMP- and TME-free pigment grade, underscoring a strategic push toward regulatory-compliant, differentiated products.

KRONOS Worldwide — A legacy player focused on high-performance grades, where deep formulation expertise and customer relationships protect higher-margin niches.

LB Group (Lomon Billions) and Ishihara Sangyo (ISK) — Regional champions with global ambitions. Their mix of chloride and sulfate capability and proximity to certain end markets give them tactical advantages in specific geographies.

Cristal Global — A large-scale producer with global footprint; its scale and multi-site capability are strategic assets as supply chains tighten.

Asset rationalization: Multiple strategic site sales and closures announced across 2025–2026 reflect a broader trend of footprint optimization and response to local regulatory cost pressures.

Product differentiation: New product introductions that address regulatory and formulation trends (e.g., TMP-/TME-free pigments) indicate R&D-led pathways to defend margins and meet customer sustainability mandates.

Upstream focus: With trade barriers and higher compliance costs, securing feedstock — whether through vertical integration, long-term contracts, or regional partnerships — is a dominant theme for risk-averse players.

Executives should treat 2026 as a year for active portfolio and supply-chain decisions rather than passive monitoring. The following actions are prioritized based on our scenario analysis:

Supply-risk mapping and secured sourcing: Build a 24–36 month supply-risk dashboard that includes feedstock origin, tariff exposure, and regulatory risk. Where possible, convert spot exposure to indexed contracts or strategic offtakes.

Cost-to-serve reengineering: Reassess plant footprints against end-market demand and total landed cost (including tariffs and environmental compliance). Selective site consolidation or greenfield near-shoring may be justified under several scenarios.

Product and formulation roadmap: Prioritize launch of regulatory-compliant pigment grades and high-value treated products. Customers are willing to pay for low-impurity, low-risk inputs that reduce downstream reformulation costs and compliance headaches.

M&A and partnership playbooks: Explore bolt-on acquisitions to secure feedstock or expand treatment capabilities; consider JV structures in regions where trade barriers elevate local production premiums.

Scenario-based commercial strategies: Develop pricing and contract templates for three scenarios — benign demand recovery, constrained supply with upward cost pressure, and disruptive tariff escalation — to expedite commercial responses.

The complete study is designed as an operationally actionable roadmap for 2026. Key deliverables include:

Granular, audited market sizing (historic 2020–2025 and detailed forecasts through 2032) with scenario sensitivity and unit economics.

End-market demand models (coatings, plastics, paper/inks, cosmetics/others) with adoption curves, elasticity analysis, and substitution risk matrices.

Supply-side analysis by process (chloride vs. sulfate), plant-level cost stacks, and feedstock-flow maps reflecting tariff impacts and recent trade measures.

Competitive benchmarking and strategic profiles for the leading producers, including recent corporate actions, capacity movements, and capability heatmaps.

Regulatory and environmental impact assessment, including an actionable compliance cost tracker and investment implications for mining and pigment operations.

Playbooks for procurement, pricing, M&A, and capex prioritization — including modelled ROI cases and break-even thresholds under alternate tariff and feedstock scenarios.

TiO2 in 2026 is not a simple volume game. It is a multi-dimensional contest in which feedstock security, regulatory foresight, product differentiation, and tactical commercial execution determine returns. Companies that treat the next 12–24 months as a window for deliberate repositioning — not mere cost-cutting — will create durable advantage. Our full report provides the data-driven granularity, playbooks, and executable scenarios to make those decisions with confidence.

To access the complete analysis, detailed segment forecasts, plant-level economics, and the full set of strategic templates referenced above, please visit the PW Consulting report page. The full study contains the segment-level numbers and country/plant breakdowns that are intentionally summarized here to preserve proprietary analytical value.

For detailed analysis of this topic, please visit the official page:Titanium Dioxide (TiO2) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com