Van Market Growth and Future Trends

Other |

2026-03-11 08:42:44

As global vehicle architectures accelerate toward electrification, mixed-material design, and smarter, more modular assemblies, adhesives have shifted from a supporting role to a core enabler of automotive value chains. PW Consulting’s latest Automotive Adhesives Market study — anchored on a 2025 base year and projecting through 2032 — delivers the actionable intelligence executives need to align product roadmaps, procurement decisions, and M&A strategies with a market that is both expanding and structurally evolving. The market expanded from roughly USD 4.97 billion in 2020 to USD 6.65 billion in 2025 and is forecast to reach about USD 10.01 billion by 2032, tracking a compounded annual growth rate of 6.01% over the 2026–2032 period. This trajectory underscores sustained demand across OEM and aftermarket channels, but the path to profitable growth is uneven and strategy-dependent.

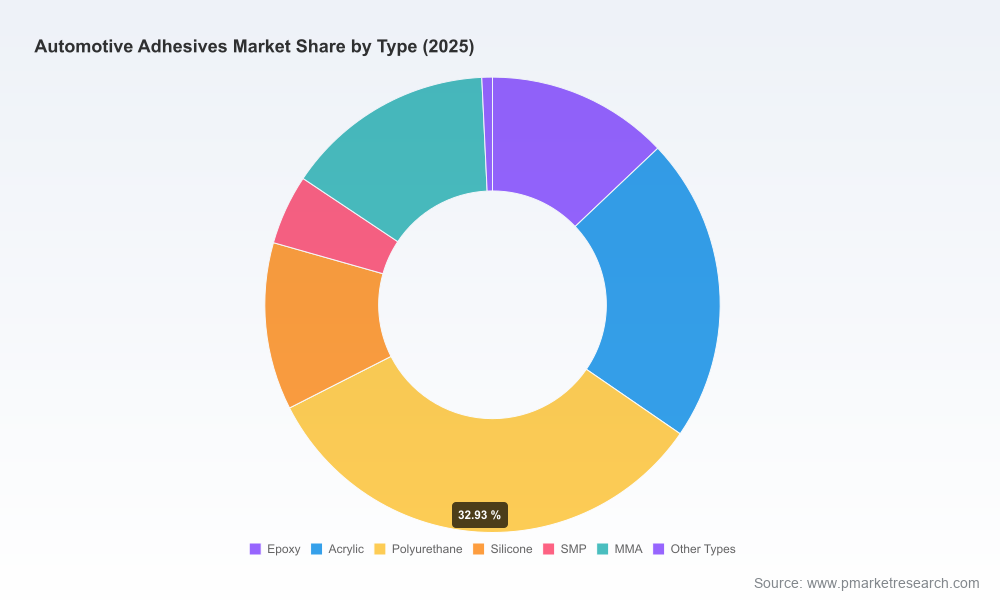

Automotive Adhesives Market

Clarifies where growth is structural versus cyclical. The study differentiates demand driven by vehicle production volumes from demand created by technology transitions — for example, increased use of structural adhesives in mixed-material body-in-white and specialized chemistries for EV battery assembly.

Automotive Adhesives Market

Translates regulatory inflection points into commercial levers. Compliance pressures — including mandatory quality certifications and tightening VOC/emissions rules — are reshaping supplier selection criteria and product roadmaps. Our report maps these regulatory vectors into procurement risk matrices and product development priorities.

Automotive Adhesives Market

Enables capital allocation with precision. With a granular view of market size, growth rates, and scenario-based upside, leadership teams can prioritize capacity investments, targeted geographic expansions, and bolt-on acquisitions that accelerate time-to-revenue.

Supports go-to-market redesigns for EV and ADAS supply chains. Adhesive applications in battery modules, sensors, and displays demand both material performance and functional safety adherence — our research lays out validated routes to qualification and commercialization in these high-barrier segments.

The automotive adhesives market is in structural expansion, driven by three converging trends. First, multi-material vehicle bodies and the pursuit of lightweighting are increasing the technical complexity and volume of structural bonding solutions. Second, electrification has created entirely new adhesive use-cases — from thermally conductive and electrically insulative formulations in battery modules to debonding-on-demand chemistries that enable end-of-life recycling. Third, tighter environmental and safety standards are raising the bar for supplier qualification and process controls.

These trends are interacting with operational realities: suppliers face margin pressure from raw-material volatility while being required to deliver higher quality and traceability. At the same time, OEMs are shortening validation cycles for component suppliers and demanding Just-in-Time (JIT) logistics close to production hubs — a dynamic that is shifting the economics of regional footprint strategies.

Functional safety for battery adhesives: Adhesives used in EV battery assembly increasingly must align with ISO 26262 expectations for functional safety. That shifts procurement evaluation from purely material performance to lifecycle validation and post-failure analysis capabilities.

Quality certification as a baseline: IATF 16949 has moved from “nice-to-have” to mandatory in many OEM supplier selection processes for adhesives. Recent supplier certifications confirm this trend; compliance now materially affects access to Tier 1 and OEM contracts.

Sustainability and emissions compliance: Low-VOC and water-based formulations are not just marketing claims — they are compliance requirements in key markets (EU/US), influencing product portfolios and R&D roadmaps.

Thermal and environmental resilience: Under-hood and powertrain applications continue to favor hot-melt and reactive chemistries that sustain performance at elevated temperatures (up to 250°C), constraining material substitution in these zones.

We designed this study as a practitioner’s toolkit for 2026 planning cycles. Beyond market sizing and trend narratives, the research contains:

Proprietary supply-chain maps and lead-time models that quantify qualification timelines and logistics risk for regional expansions.

Supplier scorecards and capability matrices that rank vendors across technology, quality certification, scale, and aftermarket service — useful for sourcing and strategic partnerships.

Scenario-based demand models (base, acceleration, stress) that translate OEM electrification roadmaps and regional production shifts into adhesive volume and value projections.

Go-to-market playbooks for adhesives suppliers targeting EV battery and ADAS markets, including validated KPIs for qualification and cost-to-serve benchmarks.

M&A and partnership screening tools: a shortlist of value-creation levers and integration risks for bolt-on acquisitions to accelerate access to specialty chemistries or regional capacity.

Regulatory impact assessments and reformulation roadmaps for low-VOC, water-based, and debond-on-demand technologies.

Commercial templates — contract language, warranty frameworks, and service-level agreements — aligned to adhesive-specific failure modes and functional safety obligations.

The market shows a moderate concentration of capability among established chemical and adhesive specialists. Leading firms bring complementary strengths: global manufacturing scale, OEM relationships, and specialized chemistries for battery and mixed-material bonding. Our report profiles each major player and evaluates strategic position across three vectors: product-tech leadership, manufacturing and supply-chain footprint, and commercial muscle with OEMs and Tier suppliers.

Henkel: A strong position in structural adhesives and lightweight joint solutions with recent launches focused on durability and vibration damping. Strategic investments in regional logistics and warehouse capacity are enabling JIT fulfillment in high-growth manufacturing hubs.

3M: Depth in high-strength structural and repair adhesives, with established OEM-facing channels for assembly and collision repair markets. Their brand and global service footprint remain differentiators.

Sika: Known for crash-durable and multi-material bonding solutions in body shop and exterior applications, offering integrated systems for mixed-material vehicles.

H.B. Fuller: Differentiates with low-emission, water-based, and hot-melt technologies aimed at interior and lightweight structures and aftermarket repair segments.

Dow: Focused on silicone-based sealants for under-hood electronics and mobility systems, critical for electric and thermal management applications.

Arkema, BASF, Permabond, DELO, Jowat, ITW, Lord: Each brings focused capabilities — from battery module adhesives and specialty polymers to UV/2K solutions for electronics and vibration-damping chemistries — creating a competitive matrix where partnerships and niche leadership matter as much as scale.

Recent market moves underscore strategic priorities: product launches targeting vibration-damping and next-gen silane-modified polymers, supplier facility expansion to support JIT in major manufacturing geographies, certification wins that materially expand qualifying credentials, and targeted acquisitions to round out portfolios. These activities are both responses to and drivers of the market’s trajectory.

For adhesive manufacturers: prioritize qualification programs for EV battery and ADAS modules; invest selectively in low-VOC reformulations and certifications that OEMs now mandate. Evaluate regional micro-fulfillment centers to meet JIT expectations and shorten lead times.

For OEMs and Tier suppliers: embed adhesive performance early in design-for-manufacturability processes. Reassess supplier scorecards to weight certification and lifecycle traceability more heavily than unit price alone.

For investors and M&A teams: use the report’s screening tools to identify acquisitions that provide proprietary chemistries (e.g., debond-on-demand, thermally conductive adhesives) or regional footprint advantages in electrification hubs.

For procurement leaders: renegotiate contracts to include functional safety obligations, shared validation costs, and inventory-sharing arrangements that reduce cost-to-serve while ensuring supply continuity.

This article intentionally presents the strategic signal; the full PW Consulting report provides the supporting analytical noise — methodology, scenario assumptions, supplier-level scorecards, and detailed qualification roadmaps — that your team will need to operationalize strategy in 2026. If you are sizing capacity, evaluating an R&D pivot to debonding technologies, preparing for supplier rationalization, or building an inorganic growth thesis, the report is structured to shorten decision cycles and reduce execution risk.

To preserve the integrity of competitive insights for clients who require granular market segmentation and supplier-level economics, we have reserved detailed breakdowns and downloadable workbooks for the full report. Contact PW Consulting to request the dataset and a tailored briefing that aligns the findings with your portfolio and timeline.

The adhesive market’s steady expansion — from the mid-single-digit billions in 2020 to an expected roughly USD 10 billion by 2032 — signals both opportunity and complexity. Winners in 2026 will be those that treat adhesives not as commodities but as engineering systems that intersect materials science, process engineering, regulatory compliance, and supply-chain architecture. PW Consulting’s Automotive Adhesives Market study equips decision-makers with the strategic frameworks and operational tools to capture this value as vehicle platforms and supply chains continue their rapid transformation.

For detailed analysis of this topic, please visit the official page:Automotive Adhesives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com