Electric Enclosure Market — Strategic Outlook for 2026 (PW Consulting)

Executive snapshot

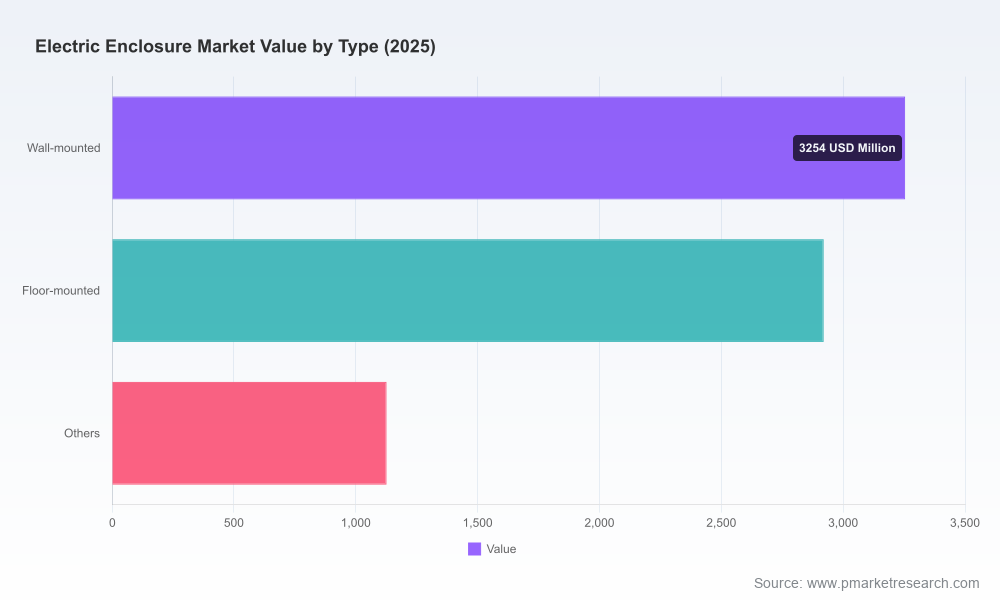

Our Electric Enclosure Market study (base year 2025, historical 2020–2025, forecast 2026–2032) provides a practice-oriented, board-ready assessment of where value will be created and captured through the next planning cycle. The market has grown from approximately USD 5,500 Million in 2020 to USD 7,300 Million in 2025, and is projected to continue expanding at an approximate CAGR of 7.5% through 2032, reaching roughly USD 12,200 Million by the end of the forecast horizon. Figures are expressed in USD, revenue unit = Million.

Electric Enclosure Market

For executives preparing 2026 budgets, capex plans, M&A roadmaps, and technology investments, this research translates macro momentum into specific strategic imperatives — without revealing the granular segmentation that subscribers will find in the full report.

Electric Enclosure Market

Why this study matters for 2026 decision-making

- Translate growth into choices: The market’s sustained mid-single-digit to high-single-digit growth creates bandwidth for incumbents to expand and for new entrants to niche — but every dollar of investment must be positioned against clear demand elasticities and regulatory constraints.

- Prioritize product bets: Rising thermal densities, EV charging roll-outs, and data center expansion force enclosure design tradeoffs (protection, cooling, modularity) that determine product roadmaps and margins.

- De-risk supply chains and materials: Steel, die-cast alloys, FRP and polymer supply volatility makes sourcing strategy a first-order question for 2026 continuity planning.

- Align compliance with go-to-market: Certification timelines for NEMA, UL and other standards can be multi-quarter impediments to revenue recognition; planning needs to be integrated with engineering roadmaps.

Market dynamics and structural drivers

The enclosure market sits at the intersection of infrastructure modernization and broad-based electrification. Key demand drivers we track in the report include industrial automation retrofit cycles, distributed energy resources and inverter roll-outs, rapid expansion of EV charging networks, and capacity growth in hyperscale data centers. Each of these drivers imposes different product and service requirements: ingress and environmental protection (NEMA/IP ratings), thermal management (active and passive cooling), mechanical robustness, and maintainability for field service.

Electric Enclosure Market

Regulatory and standards frameworks are central to commercial viability. The report synthesizes the operational impact of NEMA 250 Type ratings and NEC Article 314 installation marking on design and installation timelines, details how UL 50/50E shape enclosure specification for up to medium-voltage applications, and explains how IP/NEMA compliance is becoming non-negotiable for data center and EV infrastructure projects. For underground electrical infrastructure, ANSI/SCTE 77 requirements add another layer of product and testing complexity. We map the certification ladders and lead times that materially affect product-to-market timing.

Competitive landscape — what we observed

The market structure combines pockets of specialization with broad-system providers. Market concentration is moderate: the combined share of the largest three players is material but not dominant (CR3 ≈ 35%), and the top five increase that footprint further (CR5 ≈ 45%). This profile produces local oligopolies in certain subsegments while leaving room for innovative niche players and regional champions.

- Hammond Manufacturing (Guelph, Ontario, Canada — https://www.hammfg.com/): A specialist in industrial and electronic enclosures, Hammond’s strength is rugged die-cast series and customizable NEMA-rated options. Recent product enhancements (e.g., IP68 flanged additions to rugged lines) demonstrate a play to win in harsh-environment and outdoor surface-mount applications.

- nVent (HOFFMAN) (London, UK — https://www.nvent.com/en-us/): Known for heavy-duty solutions and climate-controlled enclosures, nVent’s HOFFMAN brand has been positioning for inverter and EV charging deployments. Public Q1 2026 results and raised guidance underline continued demand resiliency across its enclosure businesses.

- Hubbell (Shelton, Connecticut, USA — https://www.hubbell.com/): Strong in utility and underground enclosures, Hubbell’s FRP and below-ground offerings make it a preferred partner for power distribution and infrastructure projects where ANSI/SCTE 77 compliance and lifecycle robustness matter.

- Eaton (Dublin, Ireland — https://www.eaton.com/): Offers broad B-Line and non-metallic platforms; Eaton’s distribution network and cross-sell into electrical components position it as a systems provider for commercial and industrial customers seeking integrated solutions.

- Rittal (Herborn, Germany — https://www.rittal.com/us-en_US/): A leading modular and freestanding systems supplier with strong hygienic and stainless-steel design capabilities — attractive in food, pharma and other regulated industrial verticals.

- Schneider Electric (Rueil-Malmaison / France — https://www.se.com/): Delivers broad PanelSeT enclosures and integrated distribution platforms; Schneider’s software-and-hardware angle helps customers bundling power management and enclosure solutions.

Beyond these incumbents, the competitive field includes agile non-metallic specialists and contract manufacturers introducing design-for-manufacturability and rapid-prototype capabilities. Recent launches across the market (including non-metallic conduit expansions and IP68-focused product variants) highlight a shift toward niche differentiation and environmental hardening.

What the report delivers — practical, operational outputs

This is not a passive market narrative. The full report contains the tools a leadership team needs to convert insight into action:

- Executive dashboards and scenario models (base case and alternative demand curves tied to a 7.5% CAGR central estimate) for use in planning and board presentations;

- Product roadmaps mapped to customer needs (thermal, ingress, modularity) and the certification timelines required to commercialize each variant;

- Detailed go-to-market playbooks by channel (OEM, distributor, EPC contractor) with suggested contract structures and margin benchmarks;

- Competitive scoring matrices and supplier heatmaps to prioritize strategic partnerships and acquisition targets without disclosing proprietary customer lists;

- Regulatory compliance checklist templates (NEMA, UL, NEC, ANSI/SCTE) paired with estimated validation lead-times and cost impacts;

- Supply-chain risk assessment and mitigation playbook focused on raw material sourcing, secondary suppliers, and nearshoring options;

- Case studies demonstrating successful migrations from bespoke builds to modular platforms and the operational KPIs that improved as a result.

Strategic recommendations for 2026

Our priority recommendations are organized by urgency and impact horizon so leaders can translate the market trajectory into quarterly and annual plans.

- Immediate (next 6–12 months): Accelerate product launches that address high-growth verticals (EV charging, data centers, renewables) with pre-certified IP/NEMA packages. Lock multi-year supply agreements for critical alloys and polymers to hedge against price and lead-time volatility. Use the report’s scenario dashboards to stress-test 2026 budgets against slower and faster adoption pathways.

- Near term (12–36 months): Invest in modular platform architectures that reduce SKUs and accelerate customization. Build field-service and aftermarket capabilities — remote monitoring (sensorized enclosures) and predictive maintenance services can convert hardware revenue into recurring income streams. Explore selective local manufacturing or third-party partnerships in target markets to shorten delivery cycles.

- Medium to long term (3–7 years): Position for materials and sustainability-driven differentiation — circular design, recyclable polymers, and serviceable mechanical components will become procurement priorities for large buyers. Consider bolt-on M&A to acquire niche IP (thermal management, ingress sealing) or to gain underground/encrypted-environment capabilities aligned with ANSI/SCTE 77 requirements.

How to use this research in your 2026 planning cycle

Leaders can operationalize the study in three ways:

- Board-level scenario planning: use the report’s financial templates to model top-line and margin outcomes under different CAGR paths and product mix substitutions;

- Product and engineering alignment: leverage the certification and design checklists to integrate compliance milestones into stage-gate processes and avoid time-to-market slippage;

- Commercial execution: adopt the report’s channel and pricing playbooks to inform distributor incentives, OEM partnerships, and value-based pricing strategies for differentiated enclosures.

Closing — what you’ll find in the full report

This briefing is designed as a strategic “trailer”: it demonstrates PW Consulting’s analytical depth and the practical orientation of our Electric Enclosure Market research while preserving the granular segmentation, competitive benchmarking, and downloadable financial models for report subscribers. The full study includes detailed segment and regional breakdowns, per-segment TAMs, pricing benchmarks, and granular competitor profiles that are essential for transactional diligence and product roadmaps.

For teams setting 2026 priorities — whether you lead product development, supply chain, M&A, or commercial operations — the research provides the scenario templates, regulatory playbooks, and go-to-market blueprints needed to convert market growth into durable competitive advantage.

For detailed analysis of this topic, please visit the official page:Electric Enclosure Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com