Contact Lenses Market: Insights, Key Players, and Growth Analysis

Other |

2026-04-22 06:12:37

The trailer axle market is entering 2026 from a position of steady expansion and structural change. Our base-year analysis (2025) puts the global market firmly in the mid‑hundreds (USD Million), and our forecast to 2032 reflects a compound annual growth rate (CAGR) of approximately 5.1% over the 2026–2032 period. That trajectory indicates a market that is large enough to support differentiated players and nimble newcomers, yet still sufficiently fragmented to reward executional advantages in manufacturing, procurement and product innovation.

Trailer Axle Market

At PW Consulting we publish this preview to crystallize why the next 12–18 months are decisive for manufacturers, OEM customers, suppliers and investors: supply‑chain resilience, regulatory alignment and product differentiation via lightweighting and telematics will separate winners from laggards. This piece highlights strategic implications and actionable pathways while intentionally reserving the granular segment and regional breakdowns for subscribers of the full report.

Trailer Axle Market

Growth profile: A mid‑single digit CAGR through 2032 signals predictable demand expansion that supports multi‑year capacity and technology investments without requiring speculative, high‑risk bets.

Trailer Axle Market

Scale and runway: After steady recovery through the early 2020s, the market in the report’s base year (2025) provides a strong platform for reinvestment and consolidation plays, with a clear path to higher nominal revenue by 2032.

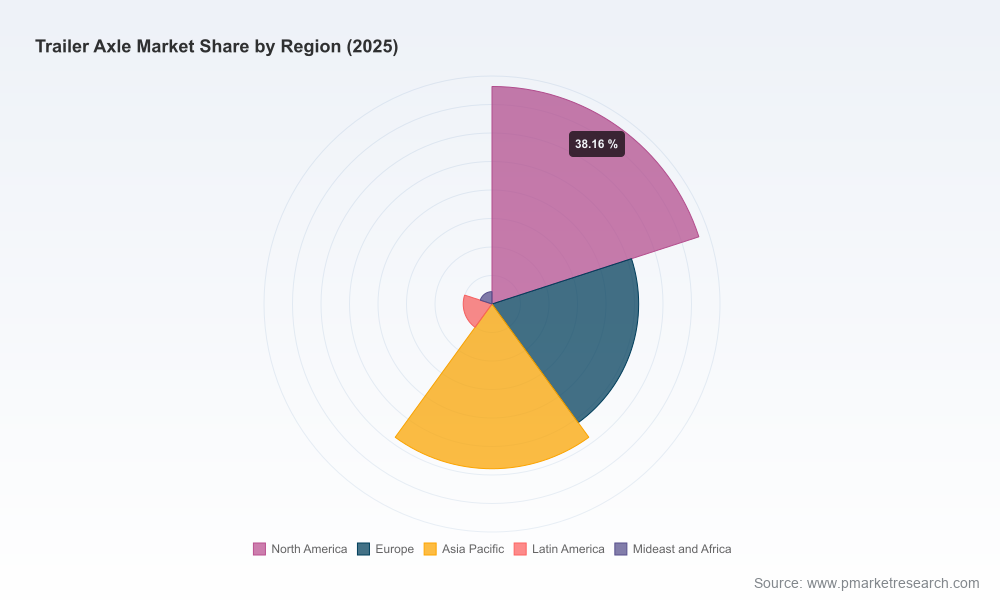

Concentration: The market remains moderately concentrated at the top; the largest three firms account for roughly two out of every five dollars of industry revenue, and the top five approach half of the market. That structure favors scale players but leaves opportunity windows for focused specialists and aftermarket operators.

Executives facing 2026 planning cycles must translate the market’s steady growth into concrete capital, product and commercial choices. Key strategic imperatives include:

Supply‑chain hedging and procurement sophistication. Volatility in steel and alloy pricing, and occasional raw material shortages, directly compress margins. Firms should prioritize multi‑tier sourcing, strategic long‑term contracts with indexation clauses, and dynamic inventory buffers calibrated to scenario stress tests.

Lightweighting for regulatory and operational advantage. Tighter emissions standards and weight regulations push manufacturers toward lighter, high‑strength alloys and modular designs. Early adoption reduces OEM retrofit costs and creates premium product lanes.

Electrification and telematics readiness. While trailer axles are mechanically mature, integration of sensors, telematics and diagnostics is accelerating. Manufacturers that offer “smart axle” options can access higher aftermarket margins and recurring revenue models.

Aftermarket and service ecosystems. With the market’s moderate concentration, aftermarket service networks and parts availability are decisive differentiators. A service‑first strategy protects lifetime value and smooths cyclicality.

M&A and partnership discipline. Strategic acquisitions should be judged by access to IP (lightweight metallurgy, sensor integration), channel expansion, or contract manufacturing capabilities rather than headline revenue multiples alone.

Our scenario framework identifies three dynamics that should be stress‑tested in every 2026 planning conversation:

Raw material price swings. Steel and specialty alloy input cost movements materially affect gross margins. Procurement policies must be linked to product pricing elasticity models to avoid margin erosion in adverse scenarios.

Regulatory tightening. New rules mandating weight or emissions‑related performance metrics will accelerate demand for lightweight and electronically compatible axles. Non‑compliant product lines will face rapid obsolescence risk.

Supply disruption. Unpredictability of raw material availability and concentrated component suppliers can produce production delays and cost overruns. Robust supplier mapping and dual‑sourcing strategies mitigate these operational exposures.

Understanding competitor positioning is central to any strategic play. Below we summarize the high‑level competitive logic implied by the market’s leading firms (contact links and company profiles are in the full report):

Dexter Axle Company — A US‑centric manufacturer with strength in torsion and spring systems across utility, recreation and specialty trailers. Their advantage lies in breadth of SKU coverage and integrated component offerings. Strategic takeaway: incumbency in light and specialty trailers translates into strong OEM relationships, but maintaining margin requires ongoing investment in manufacturing automation and aftermarket digital services.

Lippert Components — Positioned as a high‑volume US manufacturer leveraging automation to serve RV, marine and utility segments. Their recent strategic supply agreement (May 2026) to support a major trailer OEM underscores a trend toward near‑sourcing and co‑development. Strategic takeaway: partnerships that secure production cadence and localized manufacturing can be a decisive moat for domestic OEMs.

BPW Group — A Europe‑based systems integrator emphasizing disc brakes and telematics‑ready axles for commercial fleets. Their strength is systems thinking—integrated running gear coupled with electronics. Strategic takeaway: moving up the value chain into integrated systems and telematics creates higher attachment rates and recurring revenues.

Hendrickson International — Known for heavy‑duty axles and suspension systems, Hendrickson’s portfolio targets flatbed, dump and specialty trailers. Strategic takeaway: specialization in heavy applications offers defensive margins but requires continued engineering investment to meet evolving regulatory load‑management standards.

Meritor (Dana Incorporated) — A global supplier of spindles, assemblies and aftermarket parts with extensive production and service networks. Strategic takeaway: scale in aftermarket distribution and logistics supports a resilient revenue base; smaller firms should consider distribution partnerships to capture share.

Lippert’s May 2026 supply agreement exemplifies an acceleration of OEM‑level strategic sourcing. Expect more long‑term manufacturing contracts and co‑development deals as OEMs seek predictable production and compliance support.

Disc brakes and telematics integration are moving from premium to mainstream in commercial applications. Track product roadmaps that combine mechanical upgrades with electronic diagnostics.

Raw material and regulatory noise continues to shape short‑term procurement windows; companies that couple hedging strategies with agile production will gain a pricing advantage into 2027.

Translate market context into prioritized actions for the 2026 planning cycle. The following checklist is directly executable and aligned to the market dynamics above:

Implement scenario planning with the market’s base growth assumptions (use the report’s forecast as your base case). Run stress tests for ± commodity price shocks and 12–18 month supply interruptions.

Revisit product roadmaps to accelerate lightweighting and telematics compatibility. Prioritize modular designs that allow retrofit paths for OEMs and end users.

Negotiate multi‑year supply agreements with primary raw material suppliers that include clear indexation and volume flex provisions.

Expand aftermarket capabilities: localized inventory hubs, predictive maintenance analytics, and extended warranty offers to capture higher lifetime value.

Assess M&A targets for capability rather than scale: metals expertise, sensor integration IP, or secure OEM contracts offer higher strategic upside.

Invest in manufacturing automation selectively—focus where SKU rationalization and throughput improvement produce the fastest margin uplift.

Our full market study is designed to be immediately operational for strategy teams, commercial leaders and M&A desks. Highlights include:

Annualized market sizing and demand modelling from 2020 through 2032 with scenario variants for commodity and regulatory shocks.

Segmentation by type, application and region with indexed growth drivers and elasticity estimates (note: granular segment tables are intentionally gated to the full report to preserve the concise overview in this preview).

Competitor benchmarking with capability heatmaps, margin profiles and go‑to‑market strategies for the leading suppliers.

Supply‑chain diagnostics, supplier‑risk scoring, and a procurement playbook including contract templates and hedging guidance.

Commercial playbooks for OEM engagement, aftermarket expansion, and price realization models with editable Excel tools.

M&A screening funnel and valuation framework tailored to the trailer axle value chain, plus three case studies illustrating successful integration approaches.

With a reliable mid‑single digit growth trajectory and moderate market concentration, the trailer axle market in 2026 rewards disciplined, capability‑driven strategies. Focus capital on technological upgrades (lightweight materials, sensors), secure supply chains through contractual and sourcing resilience, and build aftermarket ecosystems that turn one‑time sales into recurring revenue. For companies considering inorganic moves, prioritize capability gaps that accelerate time‑to‑market for compliant, differentiated products.

This preview is intentionally selective. For the full data tables, regional and application splits, company profiles and the actionable Excel models referenced above, please consult the complete PW Consulting Trailer Axle Market report and data package.

For detailed analysis of this topic, please visit the official page:Trailer Axle Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com