Elastomeric Foam Market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-06-10 10:14:06

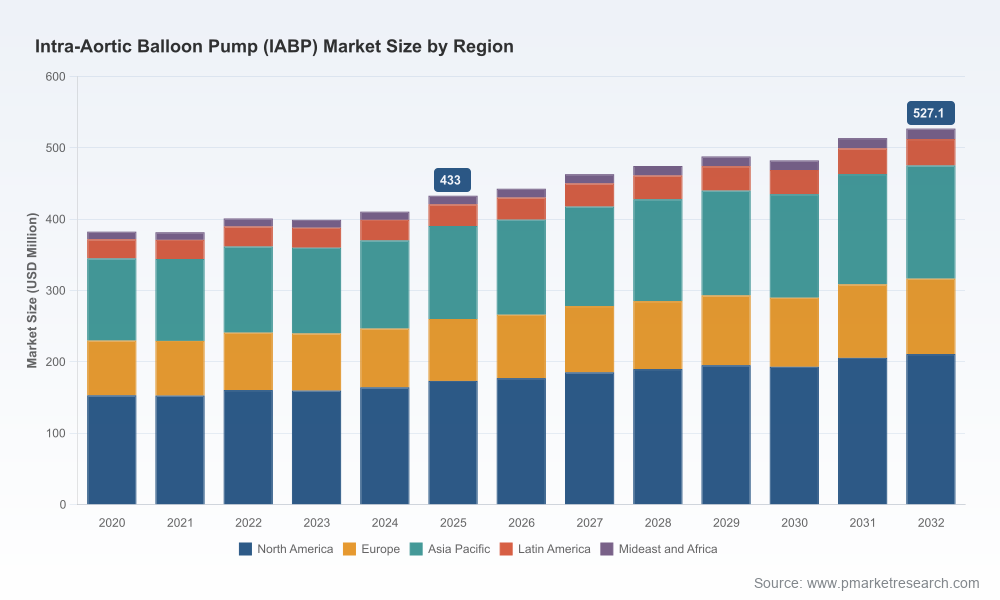

As healthcare systems recalibrate post-pandemic and procedural economics shift under new reimbursement regimes, the Intra-Aortic Balloon Pump (IABP) market occupies a distinct strategic niche for medtech executives, hospital procurement teams, and private-equity sponsors. PW Consulting’s latest market study (base year 2025) synthesizes longitudinal market behavior (2020–2025) and forward-looking scenarios (2026–2032) to equip decision-makers with the tactical intelligence they need for 2026. In brief: the global IABP market remains a modest, steadily growing market—projected to grow at a compound annual growth rate (CAGR) of roughly 2.8%—and to move from an estimated USD 433.0 Million in 2025 toward the mid-to-high hundreds by 2032. That macro stability masks pockets of regulatory, reimbursement and product-level volatility that will determine winners and losers over the next 12–36 months.

Intra-Aortic Balloon Pump (IABP) Market

Operational timing: 2026 is a pivotal year for procedure economics—new complex PCI CPT codes effective January 1, 2026 will alter hospital reimbursement for IABP-assisted interventions. Providers and suppliers must anticipate how reimbursement shifts will affect willingness-to-use and purchasing cadence.

Intra-Aortic Balloon Pump (IABP) Market

Regulatory sensitivity: recent regulatory events, including reinstated CE-mark pathways and multiple Class 2 recalls in 2025, have tightened buyer confidence and elevated compliance risk premiums. Companies with robust post-market surveillance and clear Instructions for Use will gain share; those that don’t will face restricted distribution.

Intra-Aortic Balloon Pump (IABP) Market

Consolidation dynamics: the market shows clear concentration among a small set of established players. This creates both partnership opportunities for mid-tier suppliers and procurement leverage for large hospital networks and group purchasing organizations (GPOs).

PW Consulting’s quantitative model integrates historical sales patterns (2020–2025) and supply-side disruptions to generate a conservative base-case envelope for 2026–2032. At a market size of approximately USD 433.0 Million in 2025, the market’s projected CAGR of around 2.8% yields a gradual expansion trajectory into the forecast window. That pace reflects a balance of headwinds (increased scrutiny after device recalls, reimbursement uncertainties) and tailwinds (incremental adoption in high-acuity centers, transport-ready device launches, and expanded use in perioperative and cardiogenic-shock pathways).

Importantly for strategy teams: the headline CAGR hides heterogeneity in channel growth, unit mix (console versus disposable-driven revenues), and application adoption. Our full report deconstructs these drivers and models multiple adoption scenarios—information that is intentionally withheld here to encourage direct engagement with the primary study.

Regulatory shocks and restorations: The re-certification or suspension of major products can abruptly alter regional availability. A recent reinstatement of CE-mark clearance for a leading counterpulsation system reopened European channels after a temporary suspension; conversely, multiple Class 2 recalls in 2025 impacted confidence and supply for several catheter kits and hybrid pumps. Buyers should build contingency sourcing plans and require robust traceability from suppliers.

Reimbursement reform: New CPT codes effective in 2026 change the procedural economics for complex percutaneous interventions. Strategic buyers and suppliers need to quantify the net reimbursement delta for IABP-assisted cases and incorporate that delta into pricing negotiations, bundle offers, and value-based purchasing pilots.

Channel reconfiguration: GPO activity and targeted contract awards for compatible catheter kits shifted procurement patterns in 2025. Where contract winners provided compatibility across multiple pump platforms, providers gained flexibility—heightening price competition and compressing margins for proprietary consumables.

Technology and clinical positioning: New product introductions—particularly transport-ready consoles and catheters optimized for emergency and cath-lab workflows—are reshaping purchase criteria. Clinicians increasingly value ease-of-use, portability, and single-operator set-up times as much as traditional hemodynamic performance metrics.

The market is anchored by a handful of accessible, well-funded manufacturers and several specialized suppliers that supply catheters and consumables. Market concentration metrics indicate a high degree of incumbency among top players, creating both defensive and offensive strategic postures.

Teleflex Incorporated — Teleflex has actively expanded its product stack with a transport-ready AC3 Range platform introduced in 2025. The company’s combination of system and catheter portfolio positions it well where ease-of-transport and interoperable consumables are decision drivers. For competitors and buyers, Teleflex’s launch demonstrates the commercial value of addressing emergent care settings (ambulance/air-transport, shock teams).

Getinge AB — A legacy player in counterpulsation systems, Getinge’s regulatory journey in 2025 illustrates the fragility of market access. With CE-mark reinstatement for a leading system, Getinge’s European route-to-market is restored—but lingering perception risk remains. Strategic partners should weigh near-term availability gains against reputational repair timelines.

Abiomed Inc. — While best known for percutaneous left-ventricular support, Abiomed’s platform interoperability and IABP-compatible strategies are important competitive signals: cross-platform compatibility and broad clinical use-cases can defend against single-product commoditization.

Regional manufacturers and niche suppliers — Multiple Japanese and US-based firms continue to supply differentiated catheters and low-cost kits. These suppliers are attractive targets for supply-chain partnerships and private-label agreements, especially where GPOs and hospital systems seek price-competitive alternatives.

Notable market incidents — Several product recalls and contract wins in 2025 re-aligned procurement flows. One supplier faced a Class 2 recall of catheter kits tied to labeling and training inconsistencies; another saw a contract award with a major purchasing organization that expanded a compatible-kit footprint. These events underscore the twin importance of regulatory hygiene and channel penetration strategy.

Executives and procurement leaders should treat 2026 as a window to shore up resilience while selectively pursuing growth. Our prioritized recommendations:

Immediate (0–6 months): Conduct a supplier resilience audit. Map second-source options for both consoles and consumables; require evidence of post-market surveillance, updated Instructions for Use, and rapid field-replacement plans.

Near-term (6–18 months): Re-model procedure-level economics under the 2026 CPT structure. Use database-driven analyses to quantify reimbursement delta per index case and stress-test pricing strategies against hospital margins. Where reimbursement favors IABP use, prioritize clinical adoption programs; where it compresses margins, push for bundled pricing or service contracts.

Strategic (12–36 months): Invest in real-world evidence (RWE) and comparative-effectiveness studies that position your product as a cost-effective, protocol-friendly option within shock and perioperative pathways. RWE is now table stakes for both procurement negotiations and regulatory defenses.

M&A and partnership posture: The concentrated nature of the market creates opportunities to buy scale in consumables or secure exclusive distribution agreements in targeted regions. Conversely, incumbents should consider bolt-on acquisitions that strengthen compatibility matrices and reduce recall exposure.

Commercial tactics: Offer compatibility guarantees, bundled consumable agreements, and transport-ready solutions for tertiary and emergency networks. Train-the-trainer programs and digital onboarding can materially reduce perceived risk after high-profile recalls.

Our comprehensive study goes beyond this high-level preview and contains the operational detail teams need to act in 2026. Highlights include:

A robust market-sizing model (2020–2032) with sensitivity testing across reimbursement, regulatory, and adoption levers;

Quantitative scenario analyses (base, downside, upside) that translate the 2.8% CAGR into procurement volumes, consumable draw rates, and revenue implications under multiple clinical-adoption assumptions;

Supplier risk matrix and contract-playbook templates designed for GPOs and hospital procurement to rapidly implement contingency sourcing;

Clinical pathway impact models that quantify time-to-benefit and hospital margin effects for IABP use in cardiogenic shock, complex PCI, and perioperative care (detailed application-level segmentation is exclusively contained in the full report);

Competitor benchmarking, including product-level strengths/weaknesses, regulatory posture, and recent commercial events parsed for strategic relevance;

Actionable 12–36 month roadmaps for vendors, acquirers, and health systems including prioritized investments, pilot designs, and KPIs to monitor.

For 2026, decision-makers should treat the IABP market as a disciplined-play opportunity: steady overall growth provides a stable backdrop, but near-term opportunity and risk will be dictated by regulatory developments, reimbursement realignment, and the competitive response to product incidents. Tactical moves—such as diversifying suppliers, adjusting pricing models to new CPT realities, and investing in RWE—will determine which organizations can convert modest market growth into outsized returns.

This preview is intentionally focused on strategy and high-level consequences. PW Consulting’s full study contains proprietary segmentation, region/application-by-type modeling, and granular competitor revenue breakdowns that operational teams require to execute. To access the complete dataset, scenarios, and playbooks needed to shape your 2026 roadmap, please refer to the primary report release.

For detailed analysis of this topic, please visit the official page:Intra-Aortic Balloon Pump (IABP) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com