Plant Growth Regulators Market — Strategic Briefing for 2026 Decision-Makers

Executive teaser: why PW Consulting’s new study matters to your 2026 strategy

As the global agri-input landscape pivots toward sustainability, precision management, and resilience, Plant Growth Regulators (PGRs) are re-emerging as strategic levers for value capture across high-value horticulture, cereals and grains, and export-oriented crops. Our PW Consulting Plant Growth Regulators Market study (base year 2025; forecast 2026–2032) consolidates five years of historical performance and a forward projection that is essential for leaders planning portfolios, R&D budgets, supply-chain moves, and M&A in 2026.

Plant Growth Regulators Market

Key macro context you need immediately: the sector has shown steady expansion from 2020 to 2025 and continues into the forecast window at a compound annual growth rate (CAGR) of 9.5% — a pace that materially outstrips many traditional crop protection categories. By the start of the forecast period, the market reaches a new inflection point, and our projection through 2032 quantifies the opportunity set and risk vectors that will determine winners and losers over the next strategic planning cycle.

Plant Growth Regulators Market

What the macro numbers tell you (without giving away the playbook)

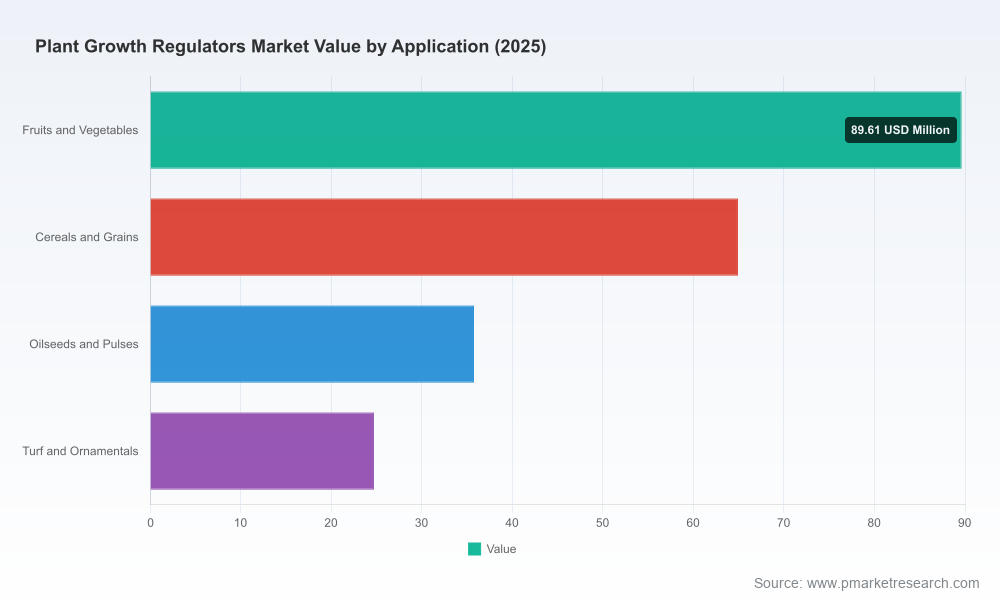

Between 2020 and 2025 the market expanded from an established base to a mid-hundreds million USD landscape in nominal terms, demonstrating both resilience and incremental adoption across multiple crop systems. Our 2026 baseline and subsequent 2032 horizon detail a clear growth runway at a 9.5% CAGR — reflecting the combined effects of yield-optimization strategies in cereals, premiumization in fruits and vegetables, and an accelerating adoption of bio-based and biological PGRs for sustainability- and certification-driven markets.

Plant Growth Regulators Market

Two structural attributes stand out for strategy: (1) moderate market concentration — the three- and five-firm concentration ratios indicate room for scale but also opportunity for nimble challengers — and (2) uneven adoption across crop types and geographies driven by regulatory regimes, registration complexity, and the pace of organic/bio-input demand. These dynamics imply that both global leaders and regional specialists can create differentiated value propositions if they align product, regulatory, and channel strategies effectively.

What PW Consulting’s report delivers — pragmatic, decision-grade outputs

- Market sizing and forward-looking revenue stacks (2026–2032), with scenario sensitivity to policy shifts, raw-material cost paths, and adoption curves for bio-based solutions.

- Regulatory mapping and operational checklists for major jurisdictions — highlighting registration pathways, common failure points, and timing assumptions for approvals that materially affect time-to-revenue.

- Commercial playbooks: go-to-market templates for seed-stage entrants, scale-up manufacturers, and incumbent multinationals. These include channel economics, lead-customer archetypes, and pricing corridors under several competitive scenarios.

- Supply-chain and raw-material risk assessments. We quantify exposure to petroleum-derived intermediates, identify alternates, and propose mitigation strategies including backward integration, tolling partnerships, and green-chemistry sourcing.

- Competitive and M&A opportunity screens. A curated list of bolt-on and capability-acquisition targets, with rapid assessment metrics to expedite diligence in 2026.

- Field-level impact frameworks for growers: ROI models for PGR programs across representative crop-management systems (calibrated for climate and crop cycles) and sensitivity to input-cost shocks.

Note: the public summary intentionally omits granular regional and segment revenue splits and individual crop-registration counts to preserve the value of the full intelligence package; those detailed tables and deal-ready annexes are available in the complete report.

Competitive landscape: what incumbents and challengers are doing now

The market is populated by a mix of specialized formulators, broad-spectrum chemical manufacturers, and emerging biologicals players. Our review of leading participants highlights three strategic positions you must anticipate in 2026:

- Specialists and formulators — companies focused on PGR chemistry and niche crop segments retain deep formulation expertise and existing ORP (operational registration portfolios). Their advantage is speed to market for incremental label extensions and ornamental or greenhouse buyers who value precision tools.

- Large chemical and agri-platform companies — incumbents are defending shelf space by investing in bio-based variants, expanding registrational coverage for major cereal and row-crop applications, and leveraging global channels to scale new launches.

- Bio-based and integrator entrants — players focused on biostimulants and biological PGRs are carving out premium pathways for organic and sustainability-focused buyers; success for these entrants depends on scalable efficacy data and navigating organic-certification pathways.

Selected company signals from our surveillance highlight tactical and strategic moves you should model in your 2026 plans:

- Fine Americas continues to consolidate a leadership position in specialty PGRs for ornamentals and greenhouse markets through a portfolio approach targeting growth-regulation and quality enhancement.

- Valagro is doubling down on biological actives and phytoingredients, seeking to translate sustainability credentials into field-proven stress-resilience offerings for high-value horticulture.

- Eastman Chemical remains a key supplier of synthetic actives used in cereals to control vegetative growth and reduce lodging — a reminder that grain-centric PGR demand remains tied to mechanization and yield stability economics.

- Zhejiang Sega and DH Crop Guard illustrate the competitive dynamic in Asia: regional manufacturers combining cost-competitive formulations with locally relevant product innovation targeted at tuber and fruit expansion, and at export-quality parameters.

- Market signals such as BASF’s new bio-based PGR (Aug 2025), Zhejiang Sega’s PANG launch (Jul 2025), and strategic acquisitions like PI Industries’ 2024 deal underline two converging imperatives — biological innovation and consolidation to secure capability breadth.

Regulatory and raw material friction — a 2026 priority

Regulation is not a static backdrop for PGRs. They are classified and regulated as pesticides in many jurisdictions, and registration timings materially influence addressable market windows. Key regulatory realities to factor into 2026 decisions include:

- Mandatory pre-market registration in major markets (e.g., the EPA/FIFRA framework in the United States), with label-specific use case approvals that constrain cross-crop redeployment.

- Country-level registration necessities (for example, checkpoints in India’s CIB&RC) that create elongated lead times and localized dossier requirements.

- Certification pathways for organic and specialty markets that favor biological and bio-derived alternatives — a fast-growing corridor but one with high evidentiary thresholds for efficacy and residue profiles.

Compounding regulatory complexity is raw-material sourcing: many current PGR actives derive from petroleum-based intermediates, creating exposure to feedstock price volatility and geopolitical supply interruptions. This structural dependency makes green-chemistry substitution and toll-manufacturing partnerships strategic levers for 2026.

Strategic implications and playbook for 2026

As you set budgets and execute plans for 2026, PW Consulting recommends a triage of actions that combine optionality with rapid value capture:

- Prioritize registration-first product launches. Given the approval-driven nature of PGR deployment, sequence product investments around markets and crops with faster, more predictable registration pathways to accelerate payback.

- Invest in biologicals selectively but seriously. Bio-based PGRs are not a peripheral trend — they represent a structural demand growth vector in organic and sustainability-aware supply chains. Fund field trials, invest in formulation science, and secure certification capability partnerships in 2026.

- Diversify raw-material sourcing. Reduce price and availability risk via dual-sourcing, strategic inventory, and backward-integration options. Evaluate tolling arrangements with regional formulators to lower capex while securing capacity.

- Use M&A tactically. With market concentration moderate, bolt-on acquisitions of niche formulators or biological players can accelerate capability delivery and market access without the integration complexity of mega-deals.

- Build grower economics tools. Deliver field-level ROI proofs that translate product efficacy into farm profitability across weather and price scenarios — sales cycles in PGRs are shortened when growers see clear, repeatable payback.

- Engage regulators early. Pre-submission meetings, targeted residue studies, and harmonized data packages shorten approval timelines and reduce surprise holds; allocate compliance budget explicitly in 2026 plans.

Scenario lens: three near-term paths (and what each means for your 2026 budget)

- Base growth (most likely): Continued adoption at the projected 9.5% CAGR driven by incremental uptake in cereals and horticulture, modest success for bio-based entrants, and steady regulatory throughput. Implication: invest in scale and targeted biological capability.

- Accelerated bio-shift (plausible): Faster-than-expected substitution to bio-based PGRs driven by retailer and buyer mandates. Implication: fast-track R&D and commercial pilots in premium supply chains; reallocate CAPEX toward formulation and certification.

- Regulatory drag (risk): Slower approvals or tightened residue limits in key markets that delay launches. Implication: shift resources to markets with predictable timelines, de-risk pipelines with reformulations, and extend cash runway via partnerships.

Why PW Consulting’s study is decision-essential for 2026

Our research translates market-scale dynamics into executable choices: where to invest, when to buy or partner, how to align supply chains, and which regulatory terrains to prioritize. It balances model-driven projections (with sensitivity ranges) and pragmatic field intelligence — from formulators to growers — so executives and investors can convert macro opportunity into defensible, near-term returns.

To preserve strategic value for leadership teams, detailed segment-level tables, registration-by-crop matrices, and target-company profiles are reserved for the full report. If you are planning product launches, M&A screens, or regulatory investments in 2026, PW Consulting’s Plant Growth Regulators Market study should be the foundational intelligence in your playbook.

Contact PW Consulting to access the full report and tailored briefings that align the market forecast with your organization’s risk appetite and growth objectives for 2026.

For detailed analysis of this topic, please visit the official page:Plant Growth Regulators Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com