Transdermal Drug Delivery Systems Market — Strategic Outlook for 2026 Decision-Makers

As PW Consulting’s senior strategy advisor and industry analyst, I present an executive preview of our latest Transdermal Drug Delivery System (TDDS) Market research — a targeted briefing designed to orient executives making resource allocation, R&D, commercial, and M&A decisions in 2026. This preview highlights the structural forces, regulatory inflection points, competitive moves, and practical toolsets contained in the full study. It deliberately demonstrates analytical depth while preserving detailed segment-level figures and proprietary models for subscribers.

Transdermal Drug Delivery System Market

Snapshot: What the market trajectory means for strategy

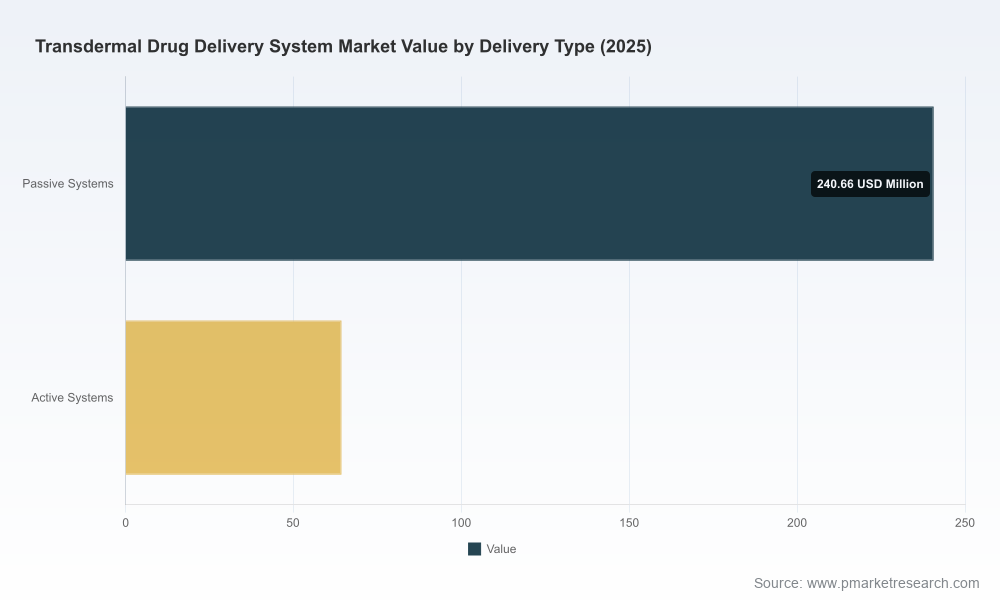

- Market scale and momentum: Our base-year modeling uses 2025 as the benchmark and projects the TDDS market to continue expanding through the forecast window. The market is estimated at approximately USD 305 million in 2025 and is projected to approach roughly USD 491 million by 2032, reflecting a compound annual growth rate of about 7.06% across the forecast period.

- Why that pace matters in 2026: That mid-single-digit growth trajectory creates a window where focused investment can achieve meaningful share shifts without the capital intensity required in hyper-growth segments. It favors targeted product innovation, selective capacity investments, and partnership models that accelerate commercialization.

- Market structure: The competitive footprint shows moderate concentration (CR3 ~45%, CR5 ~55%), leaving meaningful room for specialized challengers, contract manufacturers, and component suppliers to capture value by aligning technical capability with regulatory and payer expectations.

Core dynamics shaping near-term strategic choices

- Regulatory complexity: TDDS are combination products. Under current guidance, approval pathways require coordinated drug and device considerations (including quality systems aligned to 21 CFR Part 820 and ISO 13485). This creates higher up-front compliance costs but also raises barriers to low-cost entrants—favoring organizations with integrated regulatory-engineering capability.

- Reimbursement friction points: There is no dedicated CPT code for patch application or replacement, and hospital billing often relies on unlisted or proxy codes. Commercialization plans must therefore integrate nuanced coding strategies, payer dossiers demonstrating clinical and economic value, and adoption pilots to build real-world evidence for reimbursement conversations.

- Technology convergence and differentiation: Incremental improvements (adhesive chemistries, wear-time extensions, and user-friendly designs) coexist with step-change technologies such as microneedle systems and abuse-deterrent platforms. Strategic product roadmaps should balance near-term generics/line extensions with platform investments that create defensible product life-cycles.

- Manufacturing and supply chain imperatives: cGMP and dual regulator expectations (FDA/EMA) mean manufacturing partners must demonstrate mature quality systems. Contract manufacturing and component suppliers who can deliver validated process transfer, scale-up, and supply continuity are becoming strategic partners rather than transactional vendors.

Competitive landscape — who’s moving the market

The competitive environment is shaped by a mix of specialty developers, large pharma with product pipelines, and dedicated contract manufacturers and component suppliers. Key profiles and recent events that should inform 2026 planning include:

Transdermal Drug Delivery System Market

- Nutriband Inc. (United States) — An active developer with a clear focus on abuse-deterrent transdermal systems. Recent regulatory activity shows a push toward differentiated formulations and labeling strategies aimed at addressing safety concerns tied to opioid delivery. Their FDA submissions in 2026 mark them as a firm to watch for product-level disruption.

- Avera Drug Delivery Systems (Miramar, FL, United States) — A contract and commercial manufacturer with recent successful approvals for generics that expand access to established TDDS products. Their ability to convert regulatory approvals into market launches demonstrates the strategic importance of manufacturing scale and regulatory execution in 2025–26.

- Corium Innovations (Grand Rapids, MI, United States) — A developer with a broad intellectual property base and specialty in extended-wear (e.g., 7-day) patch technologies, representing an example of platform-driven differentiation supported by patent estates and development expertise.

- AdhexPharma (Europe) — A European contract manufacturer providing cGMP-compliant solutions for dermal and transdermal formats. Their presence underscores the cross-border supply chain considerations and the value of multi-jurisdictional compliance capabilities.

- Viatris Inc. (Canonsburg, PA, United States) — Active in the branded and generic TDDS space with late-stage clinical/regulatory filings (including a weekly contraceptive patch NDA accepted by FDA). Large pharma players can change the competitive dynamics rapidly when bringing scale-backed, differentiated products to market.

- Solventum (United States) — A supplier of core components and technologies necessary for patch construction; component suppliers can strongly influence cost structure and manufacturability for both incumbent and entrant strategies.

Notable near-term developments (regulatory approvals and NDA activities) and their strategic implications are summarized in the full report’s timeline to help prioritize engagements, alliance timing, and competitive monitoring.

Transdermal Drug Delivery System Market

What the full PW Consulting report delivers (practical, executable content)

Our full study is structured as a decision-grade playbook for 2026. It combines quantitative market modeling with qualitative operational guidance and includes:

- Proprietary market model (base year 2025; historical 2020–2025; forecast 2026–2032) with scenario toggles for pricing, generic erosion, and platform adoption rates.

- Regulatory engagement roadmap and checklist that maps typical combination-product submission pathways, required technical dossiers, and inspection readiness milestones for FDA and EMA jurisdictions.

- Commercialization playbooks tailored to different company types (innovator, generic manufacturer, CMO, component supplier) covering payer strategy, coding approaches, and launch sequencing.

- Manufacturing due-diligence templates, supplier qualification scorecards, and cost-to-serve models for patch production versus alternative formats (e.g., films, microneedles).

- Competitive intelligence modules: patent landscape summaries, facility footprint mapping, and a timeline of recent approvals and submissions to support tactical watchlists.

- M&A and partnership frameworks including valuation sensitivity to regulatory risk, revenue concentration, and manufacturing scalability — practical for 2026 negotiation posture.

We intentionally keep granular segment tables, unit economics, and customer-level pricing in the subscriber deliverable to preserve the commercial edge of clients who implement these recommendations.

Strategic imperatives and recommended actions for 2026

- For incumbent innovators: prioritize platform durability — invest selectively in abuse-deterrent, extended-wear, and minimally invasive delivery technologies that materially increase switching costs and extend product life-cycles.

- For generics and challengers: align manufacturing readiness with rapid regulatory execution. Generic approvals and launches in 2024–25 show that speed-to-market via proven CMOs pays off — but codify supply continuity and quality performance to avoid launch stalls.

- For CMOs and component suppliers: position capabilities as regulatory partners. Offer turnkey transfers with validated processes, inspection-ready documentation, and multi-jurisdictional filing support to capture higher-value contracts.

- For investors and M&A teams: target assets that reduce time-to-market for differentiated patches (e.g., process patents, validated manufacturing lines, or established payer relationships). Use scenario-based valuation that internalizes regulatory timelines and reimbursement uncertainty.

- For market access teams: build real-world evidence strategies early — when no dedicated CPT code exists, payer acceptance hinges on robust clinical and health-economic data demonstrating comparative value versus oral, injectable, or infusion alternatives.

How to use this preview

This preview maps the strategic contours; the full PW Consulting report contains the actionable analytics you need to operationalize the recommendations: the interactive model, the competitor scorecards, facility maps, and regulatory submission timelines. If your 2026 investment case or go-to-market plan depends on accurate timing and scenario-tested outcomes, you will need the full dataset and playbooks to operationalize execution.

Contact PW Consulting to schedule a bespoke briefing where we will walk your leadership team through scenario runs tailored to your asset base and strategic objectives, and deliver the granular segmentation, pricing sensitivity, and competitive benchmarking excluded from this preview.

For detailed analysis of this topic, please visit the official page:Transdermal Drug Delivery System Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com