Loratadine Market 2026: Strategic Preview for Decision-Makers

As the global allergy therapeutics landscape enters a period of incremental growth and regulatory recalibration, PW Consulting's latest Loratadine Market study offers a focused, decision-grade briefing for executives planning through 2026 and beyond. Anchored on a 2025 base year and a 2026–2032 forecast horizon, the market remains a modest, stable specialty within respiratory/allergy care — valued at approximately USD 162.4 Million in 2025 and projected to reach roughly USD 196.0 Million by 2032, reflecting a compound annual growth rate (CAGR) of 2.71% across the forecast window.

Loratadine Market

Why this market matters for 2026 strategic planning

- Predictable growth, high operational leverage: The moderate CAGR belies significant operational levers that can shift profitability—manufacturing scale, channel positioning (Rx-to-OTC pathways), and formulation differentiation (e.g., flavored oral solutions) materially influence margins and market share dynamics.

- Regulatory inflection points: Recent and pending regulatory guidance is lowering technical barriers for generics and reformulations, creating windows for market entry or product relaunch that planners must time precisely.

- Consolidation and concentration: The market exhibits mid-level concentration: the top three firms capture a meaningful share of sales, while the top five increase that dominance—conditions that favor scale players but leave tactical niches for focused competitors.

- Operational tailwinds and risks: Low unit-cost generics maintain widespread reimbursement and retail accessibility, yet supply-chain concentration for APIs and evolving bioequivalence requirements create both risk and arbitrage opportunities.

What PW Consulting’s report delivers — practical, transaction-ready intelligence

The study is designed as an operational playbook for commercial leaders, M&A teams, regulatory affairs, and supply-chain managers. It is structured to enable immediate action while preserving full transparency of assumptions and models for in-house validation. Key deliverables include:

Loratadine Market

- Market-sizing and demand modeling (2020–2032) with scenario analyses that stress-test volume and price under alternative regulatory and competitive outcomes.

- Go-to-market playbooks for Rx-to-OTC conversions and line extensions (e.g., flavored syrups, pediatric presentations), including channel economics and promotional ROI matrices.

- Regulatory timelines and bioequivalence strategy guidance aligned with recent FDA communications, enabling sponsors to design BE packages that minimize approval risk.

- Supply-chain and sourcing maps that identify single-supplier risks for key intermediates and APIs, plus prioritized mitigation actions (dual-sourcing, geographic diversification, strategic inventory buffers).

- Competitive scorecards and capability heat-maps for manufacturers, formulators, and distributors — linked to likely M&A targets and potential partnership fits.

- Pricing and reimbursement sensitivity analyses calibrated to current wholesale pricing and payor behavior, with tactical levers for SKU-level optimization.

- Customizable dashboards and Excel models for internal forecasting, deal valuation, and post-merger integration planning.

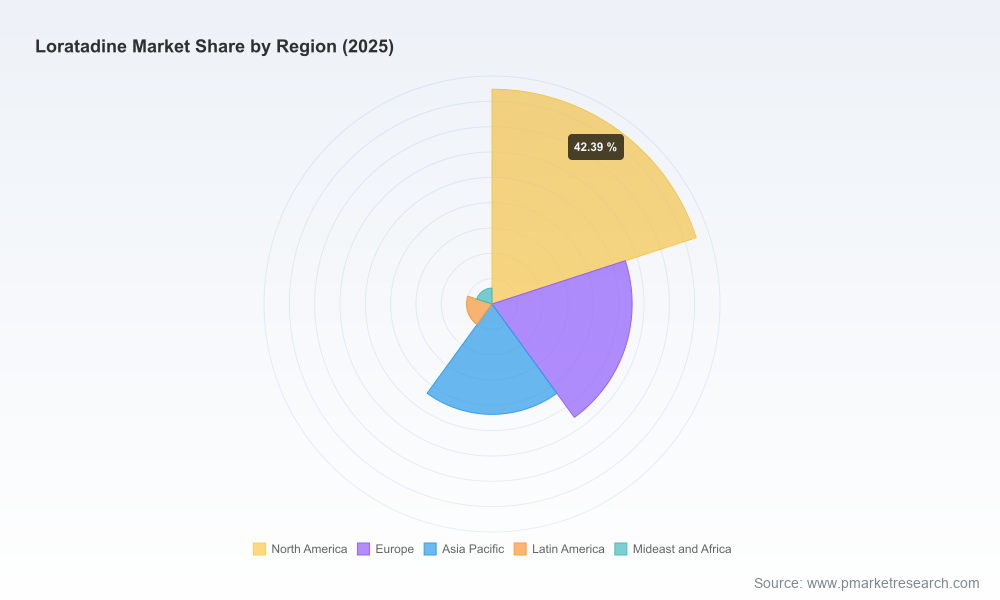

Note: this overview intentionally highlights the report’s utility while omitting granular subsegment shares and revenue breakouts; full segmentation tables, regional splits, and application-level data are available within the full report and dashboards.

Loratadine Market

Market dynamics shaping 2026 decisions

- Regulatory momentum: The FDA’s rulemaking to expand OTC access pathways (finalized in January 2025) coupled with updated draft guidance on loratadine bioequivalence (issued across 2024–2025) materially lower the effort required to support OTC switches and generics lifecycle actions. These changes reduce regulatory timeline uncertainty but demand careful study design and dossier strategy.

- Product differentiation is still decisive: Reformulation moves — for example, flavored oral solutions approved at the end of 2024 — demonstrate that small, low-cost formulation changes can reinvigorate mature molecules in retail channels. These tactics shift consumer preference and retail placement, especially in pediatric and OTC categories.

- Price compression and reimbursement: Generic pricing remains highly competitive; wholesale unit prices are anchored at very low per-unit levels, reinforcing the need for scale, low-cost manufacturing, and efficient distribution to protect margins.

- Safety signal dynamics: Periodic regulatory communications (e.g., May 2025) highlighting comparative safety or tolerability concerns for other antihistamines can accelerate demand for established agents like loratadine, but they also trigger closer post-market scrutiny.

- Supply-chain concentration risk: As with many small-molecule generics, API sourcing and supplier reliability are non-trivial strategic considerations. Single-source dependencies and lead-time variability can flip a production advantage into a market-access failure.

Competitive landscape — who to watch and how they play

The loratadine arena is dominated by well-established generic manufacturers and OTC players. PW Consulting’s competitive assessment focuses on capability vectors that move the needle in 2026: manufacturing scale, regulatory track record, OTC commercialization capability, and portfolio adjacency to allergy and cold remedies.

- Large generics and multinational OTC firms: Companies such as Teva, Viatris, Perrigo and other global generics firms maintain strong manufacturing footprints and broad distribution networks. Their advantage lies in rapid scale-up of production, global supply logistics, and access to retail placement for OTC formulations.

- Indian generics producers: Firms headquartered in India (including vertically integrated manufacturers and API specialists) continue to be efficient low-cost producers of finished forms and APIs, and they are active exporters to regulated markets. Their strategic play is volume-led competition and opportunistic tender capture.

- Smaller, agile manufacturers: Regionally focused players with FDA approvals or niche strengths can secure profitable niches via targeted approvals, specialty formulations, or co-marketing partnerships. Recent FDA approvals for certain manufacturers underscore the steady entry of credible rivals.

- Innovators via formulation moves: Branded players that pursue differentiated formulations — for example, flavored oral solutions or pediatric-friendly dosing — can extract price-premia in retail channels, creating pockets of favorable margin despite an otherwise commoditized market.

Recent, market-relevant events include FDA generic approvals for new entrants (May 2025), regulatory product approvals for flavored oral solutions (August 2024), and updated draft guidance on bioequivalence testing (2024–2025). These developments lower entry friction but also intensify competition in certain delivery formats.

Strategic implications and recommended moves for 2026

- Prioritize regulatory-aligned launches: If you are planning a launch or a product reformulation, align study designs with the latest FDA bioequivalence guidance and consider pre-submission stakeholder engagement to accelerate review timelines.

- De-risk supply now: Build supplier scorecards and secure dual API sources; negotiate volume options with contract manufacturers to hedge lead-time volatility.

- SKU and channel economics: Use SKU-level profitability analyses to decide where to invest (OTC flavored syrups vs. base tablets). Small premium SKUs with retail differentiation can yield outsized returns versus competing head-to-head on price in commoditized tablet formats.

- M&A and partnership filters: Target assets that add either immediate commercial reach (retail shelf placement, pharmacy channels) or significant manufacturing cost advantage. Plug-and-play acquisitions should be evaluated through the lens of integration cost and time-to-synergy.

- Market-access readiness: With payor and retail dynamics keeping unit prices compressed, align contracting strategies with total-cost-of-care narratives and bundle opportunities (e.g., allergy-care combos) to protect margin.

How to use the full PW Consulting report

Consider this brief as a strategic orientation. The full report contains the granular segmentations, interactive dashboards, and sensitivity models needed for executable decisions — including region- and application-level demand curves, channel-level gross margins, competitor product matrices, and prioritized action plans for regulatory submissions and manufacturing investments. For deal teams, the report supplies valuation-ready forecast scenarios and a shortlist of acquisition candidates mapped to integration blueprints.

Conclusion — read this if you plan to act in 2026

Loratadine’s market profile in the coming years is one of stable, low-single-digit growth punctuated by discrete opportunities tied to regulatory moves, formulation innovation, and supply-chain strategy. Firms that combine regulatory foresight, manufacturing resilience, and retail/OTC execution will convert modest market growth into differentiated returns. PW Consulting’s Loratadine Market study is built to translate those strategic priorities into concrete, prioritized actions for 2026. For the full segmentation, proprietary dashboards, and our step-by-step implementation playbooks, access the complete report.

For detailed analysis of this topic, please visit the official page:Loratadine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com