EPDM Rubber Granules Market 2033 Outlook: Sustainable Growth Trajectory

Technology |

2026-06-04 10:17:05

As industrial automation, electrification of buildings, and resilient power distribution accelerate across developed and developing markets, the junction box market is entering a phase of steady expansion and technical maturation. Our PW Consulting market model (base year 2025) shows a global market that reached approximately USD 4.3 billion in 2025 and is forecast to grow at a mid-single-digit compound annual growth rate (CAGR) of about 6.0% through the 2026–2032 horizon, reaching roughly USD 6.47 billion by 2032. For corporate leaders planning capital allocation, product roadmaps, and M&A activity in 2026, this technical-growth window creates both opportunity and complexity: opportunity to capture higher-margin, specification-led business; complexity from tightening regulatory regimes, fragmented supplier bases, and differentiated product lifecycles.

Junction Box Market

Timing: The market growth is steady but not explosive — companies that optimize certification, channel coverage, and product modularity in 2026 will disproportionately capture share as specifications increasingly drive procurement.

Junction Box Market

Regulatory inflection: Standards updates and more rigorous safety testing are raising the bar on product compliance and go-to-market timelines. Companies that front-load testing and compliance investments will see reduced time-to-spec and improved bid success rates.

Junction Box Market

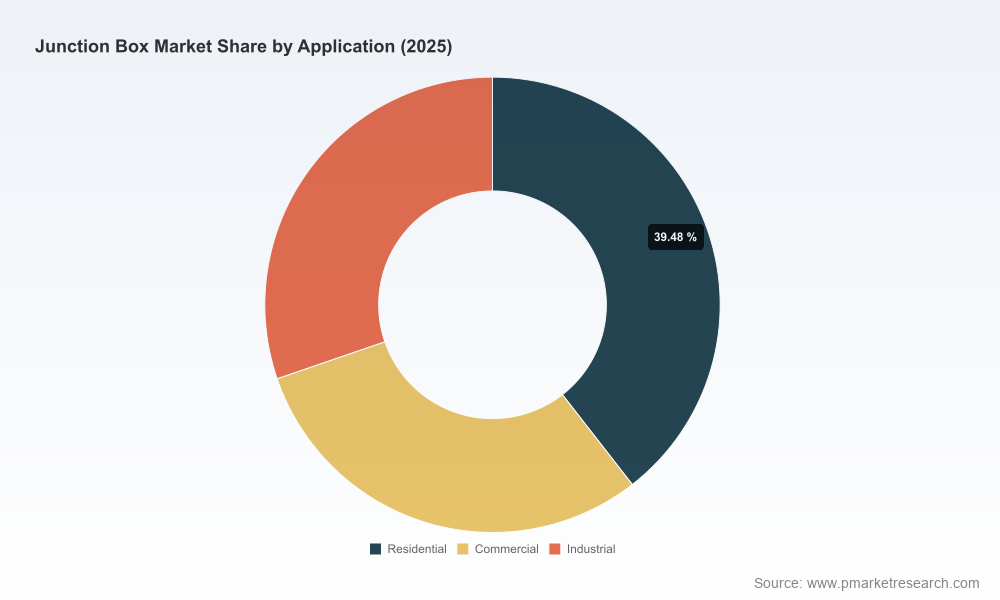

Product differentiation: The intersection of environmental protection ratings (NEMA/IP), material choices (plastic vs. metal), and application-specific performance (residential, commercial, industrial) is creating niches where premium pricing and specification-led wins are available to suppliers with the right capabilities.

Value chain complexity: Sourcing, manufacturing footprint, and the need for quick-turn customization put a premium on supply-chain agility — a decisive factor for OEMs and system integrators in 2026.

Our full study is built to be operational for commercial leadership, product management, and corporate strategy teams. Highlights include:

An interactive market model covering 2020–2032, with baseline historicals, bottom-up forecasts, and scenario analysis that lets planners test alternate demand and pricing assumptions.

Regulatory and standards tracker identifying immediate compliance risks and testing timelines that materially affect product launch calendars.

Go-to-market playbooks for OEM, distribution, and direct-spec channels, including specification capture tactics and retrofit opportunities for installed bases.

Supplier benchmarking and capability maps that evaluate product certifications, manufacturing footprint, customization speed, and channel reach. (Note: the full report contains granular supplier scores and supplier revenue splits—these are intentionally held for the full report).

Pricing and margin benchmarks by product archetype, plus a toolset for modeling the margin impact of certification, material choice, and logistics decisions.

M&A and partnership heatmaps identifying logical consolidation targets and strategic tuck-in profiles for 2026 transactions.

Risk and resilience playbooks addressing supply-chain disruption, tariff shifts, and inventory optimization under multiple demand scenarios.

The competitive field combines large, standards-driven incumbents with agile regional manufacturers. The market concentration indicators show a moderately fragmented industry: the top three players do not dominate the sector, and the top five together represent a minority share — a structural condition that favors both organic growth and consolidation plays.

Eaton Corporation plc (Dublin, Ireland) — A standards-focused OEM with deep expertise in UL- and NEMA-rated products for industrial and commercial use. Eaton’s strengths include brand trust, extensive channel relationships, and system-level integration capabilities that appeal to specification-driven buyers.

Schneider Electric SE (Rueil-Malmaison, France) — Strong in custom configurations across residential to industrial markets. Schneider integrates electrical protection with digitized building and power management ecosystems, enabling bundled-solution selling.

ABB Ltd. (Zurich, Switzerland) — Positioned for industrial automation and outdoor heavy-duty applications, ABB brings stainless-steel and heavy-duty designs suited to harsh environments and automation-enforced specifications.

Hammond Manufacturing Company (Guelph, Canada) — Known for heavy-duty NEMA-rated stainless-steel boxes and recent catalog expansion tailored to outdoor and industrial customers.

Bud Industries (Cleveland, USA) — A specialty manufacturer focused on hinged and terminal boxes for factory automation and industrial wiring, with strengths in quick-turn customization for integrators.

Southwire Company (Carrollton, USA) — Leverages power-distribution expertise to supply custom metal junction boxes aligned with power-system installers and contractors.

KDM Steel (China) — Cost-competitive manufacturer delivering customizable industrial enclosures; attractive to buyers prioritizing custom form factors and competitive pricing.

Polycase (USA) — Emphasizes UL-listed enclosures with a portfolio of NEMA/IP-rated options and a recent wave of certifications that improve market access in regulated sectors.

AWI Manufacturing (USA) — Specialist supplier of stainless NEMA 4X enclosures meeting hygiene and washdown requirements for food, dairy, and life-science customers.

ZCEBOX (China) — Rapid product portfolio updates and catalog refreshes signal a focus on iterative innovation and aggressive catalog-based sales in industrial markets.

Recent product and certification moves (catalog expansions and UL updates) demonstrate a near-term race to meet higher specification thresholds and reduce barriers to project-level procurement. For buyers, this creates short-term renegotiation opportunities; for suppliers, it raises the marginal cost of entry and increases the value of certified catalog breadth.

UL 3730 updates (effective through 2026) increase the rigor of sample testing for fire and safety compliance. The effect is twofold: longer lead times for new SKUs and higher testing budgets for manufacturers and private-label suppliers.

NEMA standard clarifications for Type 3 and 3R enclosures emphasize protection against falling rain, sleet, and ice formation — technical demands that push design, sealing technologies, and material specification choices.

UL 50 listings and CSA requirements increasingly feature in procurement checklists for outdoor-rated junction boxes, which raises the certification premium buyers are willing to pay for guaranteed field performance.

Strategic implication: certification is not a compliance checkbox — it is an entry barrier and competitive moat. Firms that can operationalize certification processes and embed them into product platforms will compress time-to-spec and command pricing power.

Build a certification-first product roadmap: Prioritize UL/NEMA/CSA compliance early in development. Treat certification timelines as critical path items in your product launch calendar.

Platformize enclosures: Invest in modular platforms (shared lids, gasket systems, mounting interfaces) to reduce SKU proliferation while supporting customization demands from OEMs and system integrators.

Target specification-led accounts: Allocate sales and engineering resources to specification writers (engineers, consultants, procurement committees) and embed samples/testing support into pre-sales.

Monetize aftermarket and retrofit: Create kit-based offerings and value-added services (e.g., pre-installed glands, factory wiring, IoT-ready sensor integration) to boost ASPs and lock in post-install revenue.

Harden supply chain resilience: Regionalize key components, establish dual-sourcing for critical materials (gaskets, seals, stainless sheets), and model inventory buffers against regulatory-driven SKU freezes.

M&A checklist for roll-ups: Seek regional manufacturers with certification footprints, niche industrial credentials (e.g., food-grade 4X), or digitized quoting platforms that can scale into value accretive consolidation.

For executives preparing 2026 plans, our research delivers executable outputs: an interactive financial model you can re-run under bespoke assumptions, product-to-specification mapping templates, a prioritized supplier shortlist for sourcing pilots, and an M&A target screening tool tuned to certification credentials and channel synergies. The full report provides the granular regional, type, and application splits that underpin these deliverables — those detailed tables and supplier-level revenue estimates are withheld from this preview to protect the integrity of our proprietary modeling and to encourage direct engagement.

If your 2026 strategy hinges on specification capture, cost-to-certification optimization, or targeted consolidation, the timing to act is now. The junction box market is evolving from a commoditized, price-driven domain into a specification- and service-driven market where certified breadth, platform engineering, and supply-chain agility determine winners.

To access the full dataset, scenario tools, and supplier scoring matrices that underpin these recommendations, please consult the PW Consulting Junction Box Market report and model on our website or contact your PW Consulting analyst for a tailored briefing.

For detailed analysis of this topic, please visit the official page:Junction Box Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com