Buy Upwork Account Introduction

Fitness |

2026-05-31 10:32:07

PW Consulting presents an executive introduction to our in-depth Stem Cell Banking Market study. This briefing surfaces the critical market signals, competitive dynamics, and decision levers that will matter most to corporate leaders in 2026 — while preserving the full analytical granularity for subscribers to the complete report. Think of this as a trailer: rigorous, directional and actionable, but intentionally non-exhaustive so that senior teams will consult the full model and annexes for transaction-level decisions.

Stem Cell Banking Market

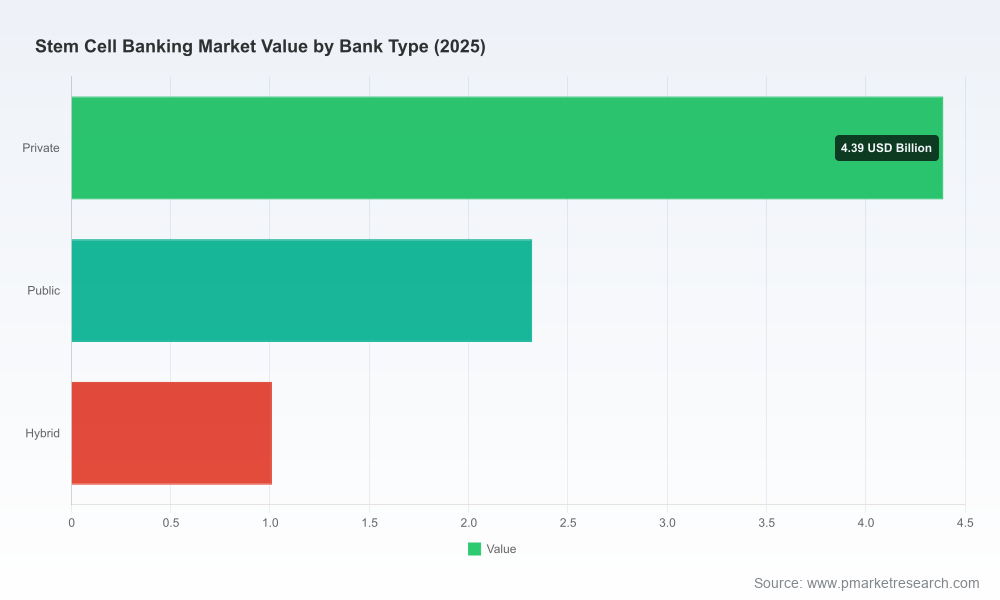

The stem cell banking market reached a base-year value of USD 7.72 Billion in 2025 and is positioned for continued acceleration through our forecast window. Our consolidated market model projects growth to roughly USD 8.98 Billion in 2026, and a long-term expansion trajectory that culminates near USD 17.5 Billion by 2032 under a compounded annual growth rate of approximately 12.4% (2026–2032). This pace reflects a combination of evolving clinical use-cases, portfolio diversification by bank operators, and persistent consumer interest in newborn and adult cell preservation.

Stem Cell Banking Market

Regulatory and standards tightening. From the European Health Technology Assessment implications for ATMPs to updated guidance from global societies, compliance complexity is rising. Expect materially higher infrastructure costs for banks that aim to support clinical translation and hospital partnerships.

Stem Cell Banking Market

Accreditation as a market-access gatekeeper. Independent accreditations (NetCord-FACT, AABB) are becoming a de facto requirement for clinical referral pathways and certain insurer conversations. Accreditation status now influences commercial partnerships and pricing power.

Reimbursement headwinds in mainstream prophylactic banking. U.S. payer policies continue to classify storage for healthy individuals as non-covered in many contexts; as a result, operators must compensate through direct-to-consumer sales effectiveness, ancillary services, or by building clinical evidence that supports reimbursable use-cases.

Service model evolution. Operators are broadening portfolios beyond cord blood — integrating cord tissue, adult stem sources and genetic screening — shifting the competitive battleground to bundled offerings and data-driven value propositions.

Fragmentation with meaningful dominant players. Market concentration metrics indicate a market that is consolidated at the top but open to disruption: the three-largest firms account for meaningful shares of the market, while the top five account for under half of total market value — creating strategic runway for mid-market consolidators and well-capitalized entrants.

Cryo-Cell International, Inc. (Oldsmar, Florida) — Positioning: quality and accreditation leader. Core strengths include a validated processing platform and FACT reaccreditation, which underpins commercial claims for clinical-grade storage. Strategic implication: Cryo-Cell leverages accreditation as a commercial moat for hospital and clinician referrals.

Cord Blood Registry (CBR) (Rockville, Maryland) — Positioning: scale and consumer reach. CBR emphasizes family banking and inventory breadth, with partnership strategies that amplify distribution. Strategic implication: scale enables premium product bundling and investment in direct-to-parent acquisition channels.

ViaCord (Rockville, Maryland) — Positioning: integrated clinical and genetic services. ViaCord’s value proposition blends newborn banking with genetic testing, enabling differentiated clinical pathways. Strategic implication: vertical integration into diagnostics enhances lifetime client value.

LifeCell International (India) — Positioning: emerging-market reach with regenerative medicine services. LifeCell balances domestic scale with cross-border offerings, reflecting a model that incumbent Western players may seek to emulate via partnerships.

StemCyte, Inc. (USA) — Positioning: focus on derived cell therapies. StemCyte couples banking with downstream therapeutic development, aligning commercial banking revenue with R&D pipelines.

Future Health Biobank (UK) — Positioning: premium private banking with genetic screening. The UK-based model emphasizes high-touch services and clinical network integration.

CellSave Arabia (UAE) — Positioning: regional expansion and adult stem cell services. Rapid service extension and regional distribution exemplify the growth approach in MENA markets.

Recent industry events further underline strategic pressure points: Cryo-Cell’s FACT re-accreditation (2026) reinforces quality differentiation; ISSCR guideline updates (2025) require revised oversight for advanced laboratory models; new entrants and service launches in the Gulf and Southeast Asia are expanding addressable markets; and prominent national recertifications attest to the rising bar for operational standards.

Use this document as the strategic hypothesis generator: it distills the most consequential trends and immediate choices facing executives as they finalize 2026 budgets and growth plans. However, granular execution requires the full report — specifically the bank-level scorecards, the market-by-service-module forecast, accreditation timelines, and the annexed financial model. Those deliverables provide the transaction-level inputs necessary to size an acquisition, model accreditation-driven revenue uplift, or run a payer negotiation simulation.

We deliberately withheld detailed regional and application splits in this briefing to preserve the integrity of those competitive insights for subscribers. If your board is considering capital deployment, partnership agreements, or a market entry, engage our team for the full intelligence pack and a 48–72 hour tailored briefing that maps our findings to your balance sheet and risk appetite.

For access to the full report and bespoke advisory services, contact PW Consulting’s Life Sciences and Healthcare Strategy practice. Our team combines market modeling, regulatory foresight, and M&A execution experience to help clients convert the opportunity in stem cell banking into durable, compliant, and profitable businesses.

For detailed analysis of this topic, please visit the official page:Stem Cell Banking Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com