Oil Water Separator Market — Strategic Outlook for 2026 Decision-Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused, decision‑grade perspective on the Oil Water Separator (OWS) market crafted for executives planning capital allocation, product road maps, and go‑to‑market moves in 2026. This briefing synthesizes our primary and secondary research, scenario analysis, and competitor benchmarking to highlight where value creation will accrue over the next investment cycle — while intentionally reserving the granular segment tables and proprietary scorecards for the full report.

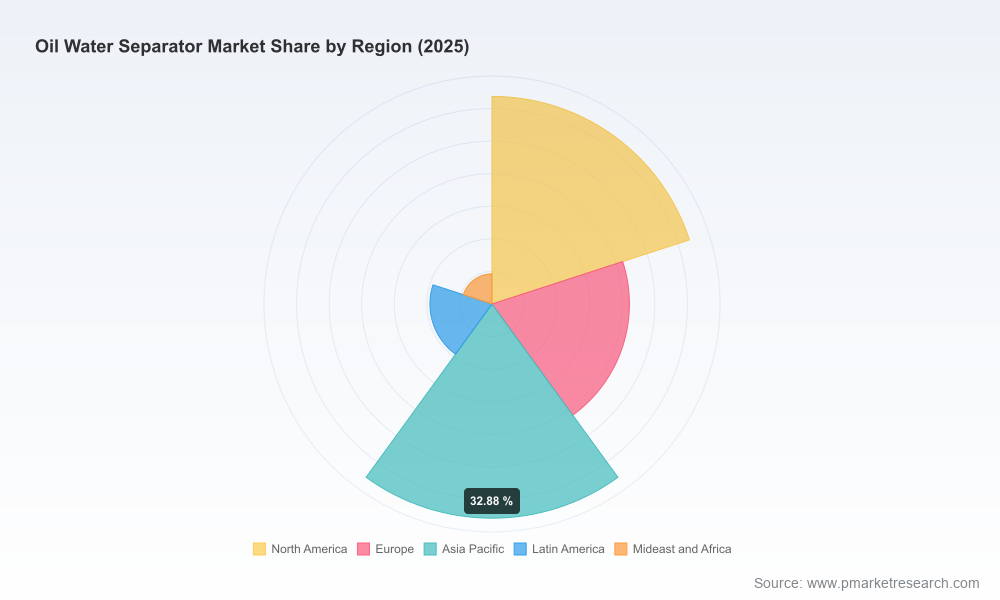

Oil Water Separator Market

Executive snapshot: market trajectory and implications

Our market model (base year 2025) finds the global OWS market positioned at roughly USD 215 million, with a compound annual growth rate (CAGR) of approximately 5.8% through the 2026–2032 forecast window. Under our base case, the market expands steadily, reflecting a mixture of regulatory-driven retrofits, replacement demand from aging infrastructure, and technology upgrades across industrial, marine, and upstream sectors. For 2026 planning cycles, this trajectory implies predictable demand growth but increased competition for high‑margin retrofit and after‑sales opportunities.

Oil Water Separator Market

Why this matters for 2026 corporate decisions

- Regulatory enforcement is a primary demand engine. Stricter effluent limits and standardization (for example, recent national and industry controls) are accelerating upgrade cycles for many facilities. Compliance windows in 2026 will force many operators to prioritize spending on proven solutions.

- Capital allocation must balance capex and lifecycle cost. Buyers are increasingly evaluating total cost of ownership (TCO) — not just purchase price — which elevates aftermarket services, remote monitoring, and low‑maintenance media as decision criteria.

- Supply‑side differentiation is technological and service‑oriented. From electrostatic coalescers to permanent media systems and modular centrifugal units, technology choice will determine installation scope, footprint, and maintenance budgets.

- Macroeconomic volatility alters project timing. Raw material and energy price shocks (notably oil price spikes observed in early 2026) increase the cost of capital and can compress margins for OEMs and contractors — but also create arbitrage opportunities for firms with flexible manufacturing and inventory strategies.

What our full report delivers (practical contents)

We designed the report as an execution toolkit for 2026 and beyond. Highlights include:

Oil Water Separator Market

- Transparent market sizing and forecast models with downloadable workbooks for scenario stress‑testing.

- Regulatory matrix and compliance timelines mapped to buyer segments, enabling prioritized retrofit roadmaps.

- Technology stack assessment that compares coalescing plates, gravity systems, electrostatic coalescers, permanent media, and centrifugal separators on metrics that matter to procurement teams (footprint, throughput, maintenance cadence, monitoring capabilities).

- Competitive benchmarking and supplier scorecards (capability, channel reach, certification status, aftermarket strength) to accelerate sourcing decisions or M&A screening.

- Eight case studies with plant‑level ROI models and payback sensitivity tables — purpose built for capital committees.

- Go‑to‑market playbooks: retrofit prioritization, OEM partnerships, licensing, and a template for service network expansion.

Data‑driven insights you can act on in 2026

Our analysis yields several operationally actionable conclusions:

- Prioritize retrofit pipelines over greenfield in the near term. Regulatory deadlines and the economics of upgrading existing assets produce faster procurement cycles and higher win rates for firms that can offer turnkey, certified solutions.

- Aftermarket & subscription services unlock margin expansion. Predictive maintenance, sensorized monitoring, and consumables are where vendors convert one‑time sales into recurring revenue — a key strategic lever in a market growing at mid‑single digits.

- Certification and third‑party validation matter more than ever. Compliance‑oriented buyers privilege suppliers with recognized testing and standards compliance; recent certification progress by a leading manufacturer is an early indicator of competitive repositioning.

- Modularization shortens sales cycles. Prefabricated and containerized units reduce installation risk for industrial and marine applications, enabling faster procurement approval compared with large civil works solutions.

- Technology mix will diverge by application economics. High‑throughput industrial wastewater favors low‑maintenance, scalable systems; upstream oil and gas and marine applications continue to demand compact, high‑efficiency electrostatic or centrifugal solutions with retrofit capabilities.

Competitive landscape — who’s shaping options for buyers

The vendor landscape blends engineering-focused regional fabricators, niche technology developers, and large system integrators. A few representative players illustrate strategic positioning:

- Highland Tank (Stoystown, PA) — Strong pedigree in API‑compliant separators and custom fabrication, appealing to industrial and municipal projects where code compliance and turnkey delivery are prerequisites.

- HydroFloTech (Elgin, IL) — Specialist in inclined plate systems, offering compact solutions for industrial wastewater and commercial applications with a focus on separation efficiency.

- Ecologix Environmental Systems (Alpharetta, GA) — Marketed solutions designed for garages, washdowns, and facility maintenance shops that emphasize American manufacturing and compliance orientation.

- Oil Water Separator Technologies (OWS Tech) — Custom design house for larger contractors and power plants; strengths in bespoke integration and containment systems.

- Mohr Separations Research (MSR) — Developer of low‑maintenance, permanent media separators that reduce lifecycle service cost — a differentiator in TCO negotiations.

- NOV Inc. (Houston, TX) — Provider of electrostatic coalescers and stabilization systems tailored to upstream oil and gas clients seeking process upgrades and retrofits.

- Striem (Kansas City, KS) — Emerging credentialed player with recent compliance achievements; certification progress is reshaping purchaser confidence in high‑efficiency systems.

- Alfa Laval (Lund, Sweden) and Veolia (Aubervilliers, France) — Global suppliers offering modular and centrifugal options as well as packaged treatment units for marine and industrial clients, combining scale with integrated services.

Regulatory, raw material, and certification trends to monitor

Three near‑term external factors will materially change procurement and product strategy:

- Enforcement of effluent limits: Tighter national and sectoral limits are shortening investment horizons for buyers who must comply or face operational constraints.

- Standards adoption: New performance standards for high‑efficiency residential and commercial separators are creating a certification premium that can be monetized through pricing and preferred vendor lists.

- Commodity and energy shocks: Recent oil price volatility has raised contractor and OEM input costs and is increasing client sensitivity to total installed cost and operating efficiency.

Scenario planning: stress cases that should inform 2026 budgets

We recommend boards and CFOs run three scenarios as they set 2026 budgets: a base case aligned with the forecast CAGR, a downside with delayed capital projects and compressed margins due to higher input costs, and an upside accelerated by aggressive regulatory enforcement and government stimulus for water infrastructure. Each scenario alters the optimal mix between product development, service expansion, and M&A activity.

Practical recommendations for 2026

- Accelerate certification and test validation to capture retrofit tenders driven by compliance windows.

- Develop bundled service offers (installation + maintenance + monitoring) to extend customer lifetime value and lock in aftermarket revenue.

- Invest in modular product variants and standardized interfaces to reduce installation time and shorten sales cycles.

- Pursue targeted partnerships or tuck‑in acquisitions to close geographic service gaps and secure channel access to industrial buyers.

- Embed TCO calculators and plant‑level ROI tools into commercial proposals to win on value rather than on price alone.

Next steps — how PW Consulting helps

This briefing outlines the strategic contours you need for immediate planning in 2026. The full PW Consulting Oil Water Separator Market report provides the unlocked toolkit: detailed segmentation tables, downloadable financial models, prioritized target lists for M&A, supplier scorecards, and plant‑level ROI case files that support board‑level decisions. For teams preparing capex proposals, procurement strategies, or product road maps, the report converts market insight into executable plans.

To obtain the complete dataset, proprietary scenario models, and actionable templates referenced here, access the full PW Consulting report and annexes through our client portal or contact your account lead. The granular segmentation and company performance matrices are available exclusively in the full deliverable — designed to convert 2026 uncertainty into competitive advantage.

For detailed analysis of this topic, please visit the official page:Oil Water Separator Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com