Continuous Screen Changers Market: Strategic Imperatives for 2026 Decision‑Makers

As manufacturers confront accelerating pressure from sustainability mandates, higher-purity product specifications, and volatile input costs, continuous screen changers (CSCs) have moved from nice‑to‑have equipment to a strategic linchpin in polymer processing value chains. PW Consulting’s new market study — anchored on a 2025 base year and projecting through 2032 — synthesizes operational metrics, competitive intelligence, and investment frameworks that executives, investors, and plant managers need as they set 2026 budgets and three‑to‑five‑year roadmaps.

Continuous Screen Changers Market

Market trajectory at a glance

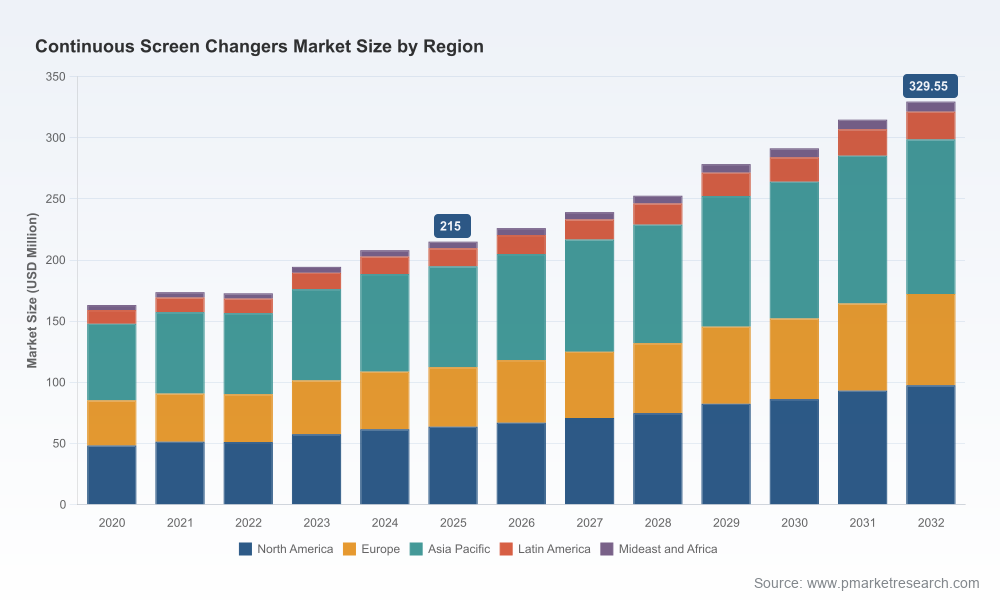

The market has expanded steadily since 2020, tracking industrial recovery and growing demand for consistent melt filtration in extrusion, compounding and recycling. From the 2020 baseline through 2025 the industry scaled noticeably, and our forecast for 2026–2032 is set to grow at a compound annual growth rate of 6.5%. By 2032 the market is projected to be materially larger than the 2025 base, reflecting both replacement cycles and incremental sales driven by higher throughput, regulatory compliance in food/medical applications, and the recycling boom.

Continuous Screen Changers Market

Why this research matters in 2026

- CapEx prioritization — Choosing between retrofitting lines with self‑cleaning backflush systems, switching to mesh‑belt solutions for post‑consumer feedstocks, or investing in high‑throughput curved‑flow units requires granular ROI modeling across throughput, downtime, and energy profiles.

- M&A and partnership scouting — The sector’s low concentration creates opportunities for bolt‑on acquisitions and strategic alliances; identifying technical fit and service footprint is essential before committing capital.

- Product roadmap and differentiation — OEMs need evidence‑based choices on which product families to scale and where to invest in R&D (e.g., energy‑efficient start‑up positions, wider filtration areas to manage contamination peaks).

- Regulatory and supply‑chain resilience — Firms must align equipment investments with tightening purity rules for food/medical packaging and the growing circular‑economy requirements for recycled polymer streams.

What the PW Consulting report delivers — practical, decision‑ready content

- Bottom‑up market sizing and seven‑year forecasts (2026–2032) with scenario analysis that isolates demand by technology pathway, operating model, and regulatory pressure points.

- Actionable go‑to‑market playbooks for OEMs and aftermarket service providers: channel mapping, pricing benchmarks, and service revenue models.

- Capital planning tools: TCO calculators that incorporate energy, downtime, spare parts, and labor savings for retrofit vs. greenfield decisions.

- Competitive landscaping and capability maps: engineering differentiators, patent activity summaries, regional manufacturing footprints, and partner ecosystems.

- Supply chain risk heat maps and materials cost sensitivity analysis to forecast margin exposure under varied metal/alloy price regimes.

- M&A scorecards and a short list of strategic acquisition targets by capability and geography (detailed profiles in the full report).

Note: this introduction highlights themes and macro sizing; the full report contains detailed regional and application splits, price points, and product‑level revenue estimates reserved for subscribers.

Continuous Screen Changers Market

Dynamics reshaping demand and technology choices

Four interlocking forces are driving equipment selection and procurement cadence across polymer processing markets.

- Regulation and product specification — Stricter requirements around polymer purity in food and medical packaging are accelerating demand for continuous filtration solutions that ensure contaminant‑free output without process interruption.

- Circularity and high‑contamination feedstocks — As recyclers scale post‑consumer streams, the need for self‑cleaning backflush and mesh‑belt technologies has risen. Systems able to handle frequent contamination surges without operator intervention command premium value.

- Cost and material volatility — Fluctuations in metals and alloys that comprise screen changer components directly affect manufacturing costs and pricing strategies. Procurement teams need hedging and supplier diversification plans to protect margins.

- Labor and uptime economics — Continuous operation reduces stoppages and operator workload. In high‑volume lines, equipment that eliminates production stops for manual screen changes delivers immediate OPEX benefits and faster payback.

These dynamics are reflected in recent vendor activity: there is clear movement toward designs that improve throughput, enable compact layouts, and reduce energy intensity while providing robust start‑up handling for sensitive polymers.

Competitive landscape — strengths, weaknesses, and strategic positioning

The continuous screen changer market remains fragmented (our concentration metrics indicate the top three players collectively control under a quarter of the market and the top five remain modestly larger). That fragmentation creates spaces for specialized engineering firms, regional champions, and global OEMs to coexist and compete on distinct value propositions.

- HI TECH Extrusion Machinery (United States) — A long‑standing specialist in fully automatic continuous units. Strengths: proven automation and consistent melt‑temperature management; appeals to customers prioritizing zero‑downtime performance. Consideration: scaling beyond core markets requires broader service networks and localized spare parts strategies.

- MAAG Pump Systems AG (Switzerland) — Known for robust CSC series products optimized for high throughput and PET processing. Recent product introductions emphasize curved flow designs and integrated start‑up positions to save energy and footprint. Strategic implication: MAAG is positioning for high‑volume food and PET producers seeking compact, energy‑efficient upgrades.

- Cofit (Spain) — Developer of self‑cleaning cartridge and belt solutions targeted at high‑contamination post‑consumer plastics. Strength: creative filtration approaches for recycling streams; opportunity: converting pilot deployments into scale sales via stronger service and retrofit offerings.

- Trendelkamp Technologie GmbH (Germany) — Focus on backflush and recycling applications; active in trade‑show launches signalling R&D cadence. Competitive edge: engineering suited to the rigorous demands of European circularity mandates.

- Chinese OEMs (e.g., Batte, Kalshine, Jwell Group) — Offer broad portfolios across plate, piston, mesh belt and other formats, typically at highly competitive price points. Strategic tradeoffs: cost advantages vs. perceived differentiation in high‑specification markets and aftermarket service reach.

- Regional manufacturers (e.g., Rajhans India) — Localized solutions with strong installed‑base relationships and competitive retrofit offerings. These players are often first choice for regional converters driven by price and proximity.

For investors and strategic buyers, this competitive map indicates two clear pathways: acquire specialized engineering firms to gain technology differentiation and service depth, or scale low‑cost manufacturing with aggressive aftermarket monetization. Both approaches require rigorous diligences centered on IP, service networks, and spare‑parts economics.

Strategic playbook for 2026 — six high‑impact recommendations

- Prioritize retrofit pilots — Run two to three short pilots comparing backflush vs. belt vs. curved‑flow units on identical lines to quantify uptime and energy delta before broad rollouts.

- Design service‑first offers — OEMs should build subscription models around inspection, spare parts, and predictive filter schedules. Service revenue will increasingly cushion equipment price competition.

- Secure alloy supply and second‑tier suppliers — Lock in procurement agreements for critical metals and diversify machining partners to mitigate input‑cost shocks.

- Target recycling hubs — Investors: prioritize assets and partners that can service European and APAC recycling initiatives where mandate‑driven demand is highest.

- Embed regulatory intelligence — For converters supplying food/medical markets, require equipment vendors to provide compliance mapping and traceability features as contract conditions.

- Use M&A to buy service capabilities — Small, service‑oriented players with strong local installed bases are efficient bolt‑on targets to expand aftermarket coverage and shorten payback for acquired units.

Decision checklist for executives

- What is the incremental uptime value of continuous filtration for our highest‑margin lines, and how quickly does that offset capex? (Use a TCO model.)

- Which product families demonstrably reduce energy and start‑up losses for our polymer mix? (Compare vendor performance data under identical line conditions.)

- Do our suppliers have proven solutions for high‑contamination recycled feedstocks and the service footprint to support scale deployment?

- How will alloy price movements change unit economics at different purchase volumes over a 24‑month horizon?

- What consolidation moves make sense to secure aftermarket and spare‑parts revenues in target regions?

PW Consulting’s full Continuous Screen Changers Market report supplies the models, vendor scorecards, and region/application‑level breakdowns needed to answer each question with data—not intuition. Our CR3/CR5 concentration analysis, competitive dossiers, and case studies of retrofit pilots provide the evidence base procurement and strategy teams require to defend capex proposals.

For decision‑makers preparing budgets and strategic plans in 2026, adopting a data‑driven, service‑enabled approach to continuous filtration will be a differentiator. The full report contains the detailed segmentation, pricing benchmarks, and country‑level demand drivers that underpin the strategic recommendations summarized here. Visit PW Consulting’s report page to access the complete dataset, proprietary models, and advisory options tailored to executive teams and investors.

For detailed analysis of this topic, please visit the official page:Continuous Screen Changers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com