Fresh Online Flowers Crafted for Every Special Moment

Other |

2026-05-19 06:03:25

As companies prepare investment and commercial plans for 2026, the ibuprofen market sits at a crossroads of steady demand growth, concentrated supply, and accelerating regulatory scrutiny. This preview distills the most consequential signals from PW Consulting’s full Ibuprofen Market report — a pragmatic intelligence package built to inform board-level decisions, manufacturing investments, and commercial strategies. In the spirit of a strategic “trailer,” we reveal the macro trajectory, competitive dynamics, and actionable scenarios while withholding granular segmented datapoints so that stakeholders are directed to the full report for the proprietary detail required to execute.

Ibuprofen Market

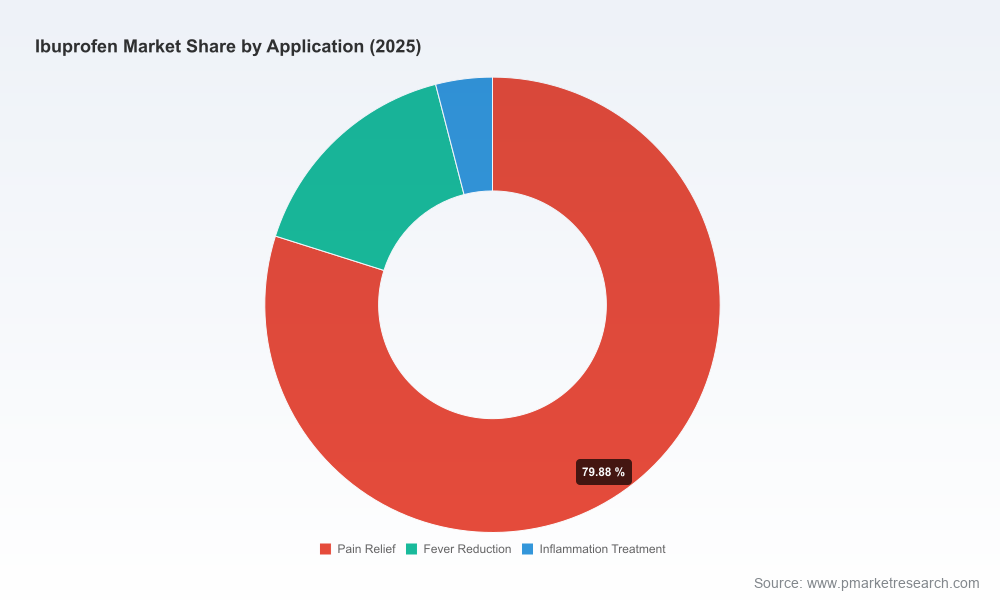

The ibuprofen market has shown resilient expansion through the early 2020s, rising from approximately 200 Million USD in 2020 to an estimated 250 Million USD in 2025 (base year). Our forecast, covering 2026–2032, projects a compound annual growth rate of 4.99%, taking the market toward roughly 349.3 Million USD by 2032. These topline dynamics reflect the compound effects of broad OTC and prescription usage, incremental label expansions, and reformulation activity in both developed and emerging markets.

Ibuprofen Market

Structurally, the market is moderately concentrated: the top three firms account for about half of the market, and the top five approach roughly seven-tenths. That level of concentration creates asymmetric power for a handful of producers in pricing, supply reliability, and formulation innovation — and it shapes the tactical levers available to purchasers, contract manufacturers, and M&A investors.

Ibuprofen Market

Three cross-cutting forces converge to make 2026 a pivotal planning horizon for manufacturers, generics companies, distributors, and healthcare purchasers:

Supply-chain concentration and geopolitics — A large share of the North American supply chain for ibuprofen APIs is sourced from China. This creates exposure to tariff regimes, export controls and logistics friction. Procurement strategies that rely on single-source or long-lead procurements will face growing risk premiums.

Raw-material and input volatility — Benchmark pricing events recorded in 2025 indicate material-level volatility. Such price spikes can compress margins for low-differentiation product lines and force commercial renegotiations if pass-through mechanisms are weak.

Regulatory intensification and quality enforcement — Recent regulatory activity highlights two opposing forces: opportunity via label or indication expansion and downside from elevated quality expectations. For example, earlier in 2026 the U.S. FDA issued draft guidance tightening expectations around dissolution testing and quality controls for acetaminophen and ibuprofen solid oral forms. At the same time, regulatory approvals expanding indications (such as an expanded postoperative pain indication for an ibuprofen injection product) create commercial upside for firms with robust clinical and regulatory capabilities.

Class II recall (March 2026): A significant recall of packaged pediatric ibuprofen due to foreign particulate contamination underscored how manufacturing issues rapidly translate into brand and supply risk.

Expanded label approval (April 2026): An injectable ibuprofen product received an expanded postoperative pain indication, illustrating the commercial value of therapeutic diversification and the returns available from clinical investment.

Our report profiles the companies that move markets and shape sourcing strategy. Three archetypes stand out in the current cycle:

Integrated multinational producer with differentiated process technologies — Example: a global chemical and pharma player operating cGMP-certified facilities in both Europe and the U.S., offering multiple powder grades, direct-compressible and fast-acting options, and investments in closed-loop sustainable processes. These capabilities create optionality for customers seeking quality, innovation, and ESG alignment.

High-volume, vertically integrated API leader — Example: a low-cost, large-capacity producer with extensive backward integration and a multiregional regulatory dossier. Capacity scale and regulatory approvals across major markets make this type of supplier a cornerstone for volume supply agreements and a disruptive force in pricing.

Regional volume suppliers with formulation partnerships — Example: large producers based in Asia supplying high-volume API and tailored formulations to generic manufacturers worldwide. Their competitive edge is price and fast ramp-to-volume for contract manufacturing partners.

Given current concentration metrics, alliances, capacity expansions, and process differentiation will determine which of these profiles gain share. Publicly disclosed capacity increases and investments by major API producers suggest the next 18 months will see pressure on mid-tier suppliers and opportunity for downstream players who can secure long-term supply at predictable cost.

For senior leaders, the question is not whether to act, but how to prioritize scarce capital and management attention. Our recommended 2026 playbook groups actions into three practical horizons:

Immediate (0–6 months): Harden quality oversight and supplier contingency. Implement tightened incoming inspection and finished‑goods surveillance aligned with the latest regulatory guidance on dissolution and QC. Re-sequence near-term procurement to add dual-sourcing options for critical API lots and secure contractual protection for price pass-throughs.

Near-term operational (6–18 months): Rebalance supply exposure through selective onshoring, regional sourcing hubs, or strategic partnership agreements. For manufacturers, prioritize investment in direct-compressible and rapid-action formulations that command higher margins and shorten time-to-market for line extensions. For OTC brands, accelerate packaging and loss-prevention protocols to reduce recall risk and build consumer trust.

Strategic (18+ months): Pursue capacity ownership or long-term equity stakes in high-quality API producers where supply security and process sustainability deliver pricing resilience. Evaluate bolt-ons that provide niche formulation capabilities, clinical evidence for expanded indications, or geographical regulatory approvals that unblock new markets.

Our full report includes scenario-based P&L simulations that quantify the impact of: raw material price shocks, tariff-triggered cost increases, recall-related revenue erosion, and upside from successful indication expansion. These models show how modest changes in input cost or a single regulatory event can alter breakeven timelines for new formulations or CAPEX projects — and they provide transparent decision thresholds for when to accelerate, pause, or pivot investments.

Proprietary market-sizing and demand forecast (2026–2032) that links clinical trends, OTC consumption patterns, and formulary shifts to revenue drivers.

Supplier scorecards and a supply‑risk heatmap that combine quality history, regulatory standing, capacity commitments, and ESG performance into actionable sourcing ranks.

Regulatory tracker and compliance playbook aligning the latest agency guidance, recall drivers, and label expansion pathways to tactical steps for QA/RA teams.

Commercial playbooks for manufacturers, generics, and branded OTC firms: go-to-market steps, pricing strategies, and channel tactics for 2026 rollouts.

Scenario P&L and investment case templates for capex, M&A, and partnership decisions — calibrated to different market concentration and price outcomes.

M&A and partnership shortlist informed by capacity, dossier coverage, geographic approval footprint, and cultural fit criteria — with prioritized action recommendations.

Note: The full report contains granular segmentation, proprietary regional and application-level splits, and supplier-specific volume/price matrices. These core datasets are intentionally excluded from this preview to preserve the report’s commercial value and to ensure stakeholders engage directly with PW Consulting for tailored intelligence.

Tariff and trade disruption risk — Maintain a continuous trade-impact model and embed trigger clauses in supplier contracts; evaluate bonded stock and insurance to blunt short-term shocks.

Quality and recall risk — Invest in upstream analytics (PAT and rapid dissolution screening) and third-party audit programs. Strengthen recall simulation and consumer communications protocols.

Price compression — Differentiate through formulation, service (rapid supply), and sustainability credentials rather than competing on base API price alone.

For executive teams building 2026 plans, the pragmatic next steps are:

Commission a 2–4 week supplier resilience review using our supplier scorecard template to identify critical single points of failure and feasible alternatives.

Run a targeted clinical/regulatory feasibility study for any potential label expansion or injectable projects, leveraging our regulatory tracker to prioritize markets.

Engage PW Consulting for a tailored workshop that maps our scenario outputs to your specific portfolio, balance sheet and risk appetite — producing a prioritized 12–24 month execution roadmap.

Ibuprofen remains a stable market with pockets of high strategic value for companies that combine supply security, regulatory execution, and formulation differentiation. The decisions made in 2026 — around supplier commitments, quality systems, and targeted clinical investments — will determine who captures the incremental upside from sustained demand growth and who bears the brunt of episodic shocks. PW Consulting’s full Ibuprofen Market report equips decision-makers with the commercial, operational, and regulatory tools to convert that strategic choice into measurable outcomes. For the complete datasets, supplier matrices, and executable playbooks, access the full report or reach out to PW Consulting for a private briefing tailored to your organization.

For detailed analysis of this topic, please visit the official page:Ibuprofen Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com