Optical Glass Market — Strategic Outlook for 2026 Decision-Makers

Executive snapshot

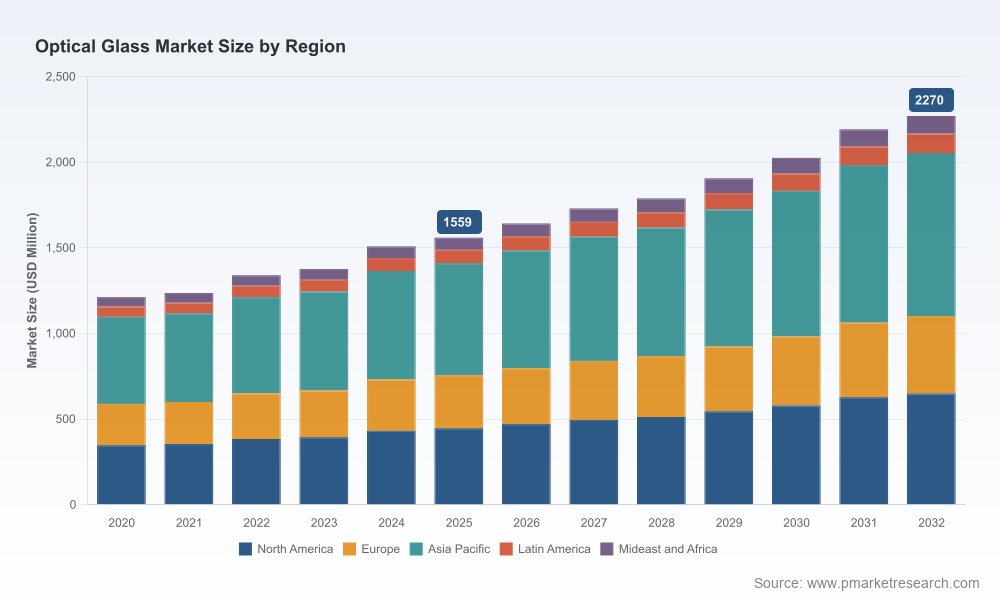

The optical glass industry is entering 2026 from a position of steady, technology-driven growth. Using 2025 as the base year, the global market was estimated at approximately USD 1,559 Million and—under the central forecast—continues to expand through the 2026–2032 horizon at a compound annual growth rate of roughly 5.5%, reaching an expected market size in the ballpark of USD 2,270 Million by 2032. This trajectory reflects a confluence of secular demand from imaging, consumer optics and medical devices, the ramp-up of new photonics and AR/VR platforms, and incremental price effects driven by raw-material and logistics dynamics.

Optical Glass Market

Why this study matters for 2026 strategic decisions

- Rapidly changing supplier economics: The industry’s near-term margins and cost bases are being re-priced by raw-material volatility (notably silica inputs) and transport bottlenecks. Procurement strategies developed in 2026 will determine competitive positioning for the remainder of the decade.

- Technology-led value capture: Advances in precision glass types and manufacturing (e.g., low-expansion, high-purity fused silica, specialized low-Tg formulations, and waveguide-capable substrates) are shifting capture from commodity suppliers to specialized technology owners. Companies that position R&D and IP strategy now can secure higher returns as demand scales.

- Supply security and regulatory compliance: New environmental permitting regimes and export-control regimes have lengthened project timelines and introduced new risk vectors; firms must integrate regulatory and geopolitical scenarios into capital and sourcing plans for 2026.

- M&A and partnerships window: Market concentration metrics indicate meaningful incumbent scale. For growth-seeking OEMs and investors, 2026 is a pivotal year to evaluate bolt-on acquisitions, capacity alliances, and licensing deals that can shorten time-to-market for specialty glass solutions.

What our Optical Glass Market report delivers (practical, transaction-focused content)

- Validated market sizing and a detailed forecasting model covering historical performance (2020–2025), base-year validation (2025), and scenarios to 2032 (including downside, baseline and upside cases).

- Segment-level demand-driver maps and heatmaps that translate macro trends into application-level growth levers and timing for go-to-market execution.

- Supply-side intelligence: a supplier capability matrix, capacity maps, technology readiness assessments, and an operations risk register tailored to midstream glass producers and downstream optics integrators.

- Regulatory and raw-material impact analysis: quantified scenarios showing the effect of silica-price swings, transportation cost shocks, and permitting delays on delivered glass costs and margins.

- Competitive benchmarking toolkit: CR analysis, capability scoring for leading players, M&A screening criteria, and a prioritized shortlist of acquisition/partner targets by strategic objective.

- Commercial playbooks and pricing-sensitivity models: tactical recommendations for procurement, hedging approaches, contractual terms, and near-term CAPEX prioritization.

- Raw-data deliverables: downloadable datasets, model workbooks, and slide-ready charts to support investment committees, sourcing negotiations, and board-level briefings.

Market dynamics shaping near-term strategy

Three interlocking dynamics will disproportionately influence decisions made in 2026:

Optical Glass Market

- Raw-material and logistics pressure: High-purity silica feedstock has become a focal point. Recent market monitoring shows silica pricing and transport costs have moved materially, creating regional delivered-cost differentials that change the economics of siting new capacity or shifting supply chains.

- Regulatory and permitting friction: Environmental scrutiny of silica extraction and processing has lengthened lead times for greenfield projects and introduced compliance costs that must be baked into any expansion model. In parallel, export-control measures and tariffs on specialty optical materials originating from certain jurisdictions have caused intermittent stoppages and raised counterparty risk for downstream manufacturers.

- Technological bifurcation: Commodity flint and crown-type glasses continue to serve high-volume lenses and consumer optics, but high-value niches—ultra-low-expansion substrates, specialized filter and colored glass, and waveguide-compatible materials—are growing faster. Companies that can align material capabilities with end-market roadmaps (e.g., AR optics, semiconductor lithography, medical imaging) will capture premium margins.

Competitive landscape — strategic implications

The market displays a mixed structure: meaningful incumbent scale exists at the top (our concentration metrics show a significant share held by the largest three and five firms), but opportunities persist for specialist players and regional champions. Below are strategic readouts for the principal competitors covered in the study.

Optical Glass Market

- Corning Incorporated — A clear leader in high-purity fused silica and ultra-low-expansion glass for precision and semiconductor optics. Corning’s strength lies in scale, materials science investments, and deep OEM relationships in semiconductors and laser optics. Strategic focus: further vertical integration with semiconductor and photonics supply chains; selective high-value product customization.

- SCHOTT AG — A specialty glass innovator with capabilities spanning quartz and specialty optical substrates. SCHOTT has demonstrated aggressive innovation-to-scale moves (for example, recent commercial milestones around waveguide production and a new hermetic optical MEMS lid family). Strategic focus: commercializing AR/photonic components and expanding licensing/venture partnerships.

- Ohara Corporation, Hoya Corporation, AGC Inc., Nikon Corporation, Sumita Optical Glass — These firms collectively represent depth in lens-grade and precision glass with strong positions in imaging, medical optics and precision instrumentation. Their strengths are high optical purity, tight tolerances, and long-standing customer relationships. Strategic focus: defend premium lens segments, co-develop application-specific materials, and pursue manufacturing excellence initiatives.

- Nantong Guoguang Optical Glass and regional specialists — Growing vendors that emphasize colored and filter glasses, and price-competitive offerings. Their acceleration is enabled by local market proximity and cost structures. Strategic focus: move up the value chain through quality benchmarking, differentiation via coatings or integrated optics, and partnerships with global integrators.

Recent developments to watch (signal vs noise)

- Product innovation as a leading indicator — SCHOTT’s introduction of hermetic optical MEMS lids in March 2026 and its prior progress on scaling geometric reflective waveguides are examples of how material innovation is migrating into system-level components. These moves often presage new OEM design-ins and multi-year adjacencies for glass suppliers.

- Raw-material and regulatory headlines — Elevated silica prices (observed benchmark levels in early 2026) and prolonged permitting timelines have direct P&L and timeline implications for both new entrants and incumbents pursuing expansions. Firms that underprice these risks will face margin erosion or project delays.

- Trade controls and tariffs — Geopolitical export constraints enacted in recent years have shown that reliance on single-country supply for specialty materials can translate into sudden operational exposure. Diversified sourcing and inventory strategies are therefore tactical priorities for 2026.

A pragmatic 2026 playbook — actions by stakeholder

- For downstream OEMs (optics integrators and device manufacturers): institute dual-sourcing strategies for critical glass types, negotiate forward-volume contracts with price-adjustment clauses tied to validated silica indices, and allocate R&D co-investment with material suppliers to secure differentiated supply.

- For glass manufacturers: prioritize modular capex that can be scaled with demand, invest in low-emissions extraction and closed-loop recycling to reduce permitting risk, and develop product bundles (material + coating + assembly) to move up the value chain.

- For investors and private-equity sponsor teams: target bolt-on plays that add specialty capabilities or regional logistics advantages; stress-test returns under silica-price and tariff scenarios; and favor assets with validated long-term offtake agreements.

- For policymakers and industry associations: accelerate clear guidance on permitting timelines and create transparent silica-quality certification regimes to reduce uncertainty for investors and customers.

Data integrity and how we validated the forecast

The report’s forecasts combine bottom-up supply-capacity modelling, proprietary demand mapping across key applications, and a triangulation of primary interviews with supplier operational data and macroeconomic indicators. Scenario sensitivity tests—run against raw-material price shocks, transport-cost escalations, and accelerated adoption curves for AR and semiconductor applications—are included to help executives stress-test investment cases.

Next step — what you’ll find in the full report

This article is a strategic primer designed to highlight the value of a data-driven approach for 2026 decision-making. To preserve the utility of the full intelligence package—and to support targeted commercial and investment actions—we have intentionally omitted detailed subsegment tables and granular regional/application-level figures from this summary. The full PW Consulting Optical Glass Market report provides those segmented models, downloadable datasets, supplier scorecards, and transaction-opportunity maps that operational teams require to act with confidence.

For procurement teams, R&D leaders, corporate development executives and investors preparing decisions in 2026, the report is a practical toolkit: not only does it quantify the market baseline and growth path, it shows the tactical moves that materially change outcomes in a market growing at a mid-single-digit CAGR but reshaped by technology and regulatory shifts. Visit PW Consulting’s Optical Glass Market report page to access the complete dataset, scenario models, and our prioritized action plan.

For detailed analysis of this topic, please visit the official page:Optical Glass Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com