Trastuzumab Emtansine Market: Size, Share, and Future Growth

Networking |

2026-02-27 08:57:38

By PW Consulting — Senior Strategic Advisor & Chief Industry Analyst

Insurance Agency Software Market

The insurance agency software market has entered a consolidation-and-acceleration phase driven by the twin forces of operational digitization and responsible AI adoption. Our new market study (base year 2025, historical window 2020–2025, forecast 2026–2032) shows a clear trajectory: after steady expansion in the first half of the decade, the market reached roughly USD 403 million in 2025 and is forecast to grow at a compound annual growth rate of 6.61% through 2032, approaching the high hundreds of millions by the end of the forecast window. This report is designed as a strategic playbook for executives, CIOs, product leads, and M&A teams who must translate market momentum into durable competitive advantage in 2026.

Insurance Agency Software Market

Timing and investment prioritization — Vendors and carriers are accelerating AI and automation features into core agency management suites. Our study quantifies where enterprise buyers should prioritize spend to capture near-term operational ROI while managing incremental compliance and model governance costs.

Insurance Agency Software Market

Risk-adjusted technology roadmaps — With regulatory attention on AI and third-party risk, legacy modernization projects now require an integrated compliance and vendor-governance overlay. The report provides executable roadmaps that pair technical migrations with governance controls to reduce regulatory friction and implementation rework.

M&A and partnership playbooks — Market concentration and vendor capability clustering are reshaping buyer options. Our scenario analysis models the commercial and technical impacts of strategic acquisitions, partnerships, and white-label arrangements so acquirers can size integration effort versus revenue synergies.

Market sizing and trend analytics — A concise picture of historical growth (2020–2025) and forward projections (2026–2032) that contextualize demand drivers, substitution effects, and technology tailwinds. We provide top-line figures and growth rates to support budget planning and capital allocation.

Buyer segmentation and procurement playbooks — Profiles and decision matrices for mid-market vs. enterprise independent agencies, carrier-affiliated brokerages, and new insurtech entrants. Includes procurement checklists, SLA templates, and negotiation levers focused on implementation schedules, data portability, and vendor support models.

Vendor evaluation framework — A repeatable scoring model that balances functional coverage, integration breadth, regulatory readiness, and total cost of ownership. The framework is designed for rapid vendor shortlisting and can be adapted to organization-specific weighting.

Implementation and migration playbooks — Detailed sequences for cloud adoption, data migration, carrier connectivity, and change management. Playbooks include sprint plans, sample RACI matrices, and metrics for monitoring adoption and productivity gains.

Compliance and AI governance toolkit — Templates for AI inventory, model documentation, third-party oversight agreements, and incident response procedures mapped to the latest regulatory developments. This section is a practical primer for satisfying emerging NAIC-style expectations and state-level requirements.

Security and data privacy checklist — Practical controls and audit-ready documentation for HIPAA-compliant handling of electronic protected health information, encryption, secure integrations, and vendor security questionnaires.

Commercial models and pricing benchmarks — Negotiation levers for licensing, per-user or per-policy pricing, implementation fee design, and post-go-live support. We provide scenario-based TCO models to compare SaaS versus hosted architectures over five-year horizons.

Use cases and ROI templates — Prioritized functional use cases (policy lifecycle automation, claims workflow acceleration, underwriting triage, client servicing automation) with detailed input assumptions and payback timelines to support business-case approval.

The market is anchored by a small set of influential platform providers with deep distribution relationships, robust product suites, and differentiated go-to-market models. Our analysis covers vendor positioning, product strengths, integration posture, and likely roadmap trajectories. Key vendors profiled in the report include:

Applied Systems — Recognized for a feature-rich, enterprise-capable agency management platform that supports full policy lifecycle and accounting processes. Applied’s investments in embedded AI for reconciliation and benefits data portability point to a strategy of deep workflow automation layered on a core management backbone. Their product-led events and ecosystem orientation make them a default partner for larger independent agencies seeking scale and carrier breadth.

Vertafore — A portfolio player with multiple agency management SKUs and a growing AI and platform integration story. Vertafore’s emphasis on carrier connectivity, compliance tooling, and brokerage distribution velocity positions it well for buyers prioritizing market reach and regulatory alignment.

HawkSoft — A nimble vendor focused on cloud deployments and workflow productivity for independent agencies. Their emphasis on reporting, client portals, and AI-enabled workflows makes them a compelling option for agencies that prioritize speed-to-value and user experience.

EZLynx — A compact, feature-forward provider that combines comparative rating, CRM, and lifecycle automation. Recent moves toward AI-driven virtual assistance underline a product strategy aimed at reducing manual servicing tasks for growing agencies and startups.

Importantly, vendor differentiation is increasingly defined by ecosystem capabilities — carrier APIs, data normalization, AI governance features, and partner marketplaces — rather than baseline policy management functionality alone. Our vendor scorecards in the full report show how these factors trade off against price and integration complexity.

Product acceleration in AI — Leading vendors introduced AI-powered reconciliation and virtual assist features in early 2026. These capabilities materially reduce manual servicing effort but introduce governance and validation burdens that IT and compliance teams must plan for.

Regulatory intensification — Regulatory bodies have moved from discussion to implementation. Notably, NAIC-level activity in 2026 has crystallized around vendor registries for AI models and state-level guidance that requires inventories, governance, and third-party oversight. These developments mean procurement teams must include model provenance and auditability as mandatory selection criteria.

Data security and privacy — HIPAA requirements remain a gating factor for any software that stores or processes protected health information. Security posture, encryption standards, and breach-response readiness are now first-order considerations in vendor selection.

Commercial clarity on licensing — Regulatory and agricultural insurance nuances (such as documentation requirements around third-party software licensing fees for certain crop insurance contracts) are forcing clearer contractual language and fee disclosure in commercial agreements.

Adopt a two-track modernization approach — Protect critical operations with incremental automation (claims triage, reconciliation) while running parallel proof-of-concepts for larger platform consolidations. This reduces disruption risk while capturing early productivity gains.

Embed AI governance into procurement — Require suppliers to provide model inventories, validation artifacts, and third-party audit options. Evaluate vendors on both performance and explainability, not just feature checklists.

Require carrier connectivity roadmaps — Ensure prospective vendors commit to API standards, data normalization timelines, and a plan for sustaining carrier integrations through releases.

Stress-test total cost of ownership — Use multi-year TCO models that include hidden costs: data migration, dedicated integration engineering, license escalators, and incremental compliance controls.

Prioritize security and HIPAA readiness — Make security certifications, encryption at rest/in transit, and incident-response SLAs non-negotiable for any system touching PHI.

Factor in ecosystem and reseller dynamics — For buyers considering M&A or platform partnership, assess how a vendor’s channel agreements and marketplace strategy will affect future monetization and distribution.

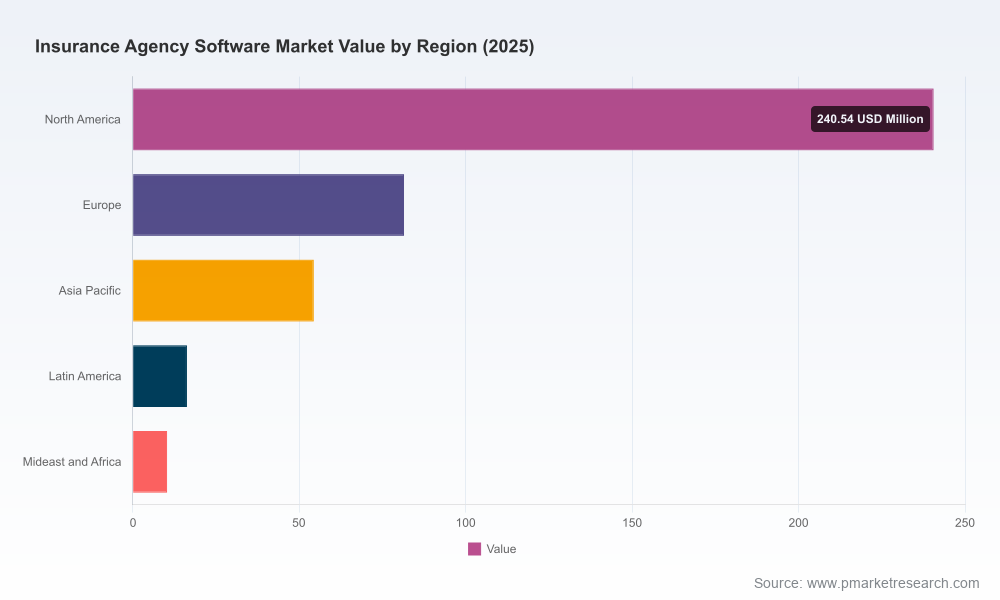

To preserve strategic value for executives and buying teams, this preview omits the full, granular segmentation tables, region-and-application-specific revenue shares, and detailed vendor market-share numbers. Those elements — including the precise regional splits, application-level forecasts, and the complete vendor scoring matrices — are included in the full report and are essential to informed vendor selection, budgeting, and M&A modeling. This “preview” approach demonstrates the analytical framework and core conclusions while reserving the detailed inputs that are operationally decisive.

Immediate (0–90 days): Run a short vendor due-diligence using our procurement checklist; prioritize pilots for AI-assisted reconciliation and claims triage.

Medium term (90–360 days): Map three-year modernization roadmaps with embedded compliance gates; evaluate potential M&A targets using the report’s vendor scorecards.

Longer term (12–36 months): Reassess platform strategy against evolving regulatory standards and carrier API adoption; lock in partnerships that deliver both depth (functionality) and breadth (distribution).

For executive teams preparing budgets and strategic plans for 2026, our study provides the frameworks, operational playbooks, and compliance toolkits needed to convert market growth into defensible, compliant business outcomes. To access the full dataset, regional and application-level segmentations, and the detailed vendor scorecards that underpin these strategic recommendations, please refer to the PW Consulting report landing page.

For detailed analysis of this topic, please visit the official page:Insurance Agency Software Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com