Polyetherimide (PEI) Market — Strategic Outlook for 2026 Decision‑Makers

Executive summary

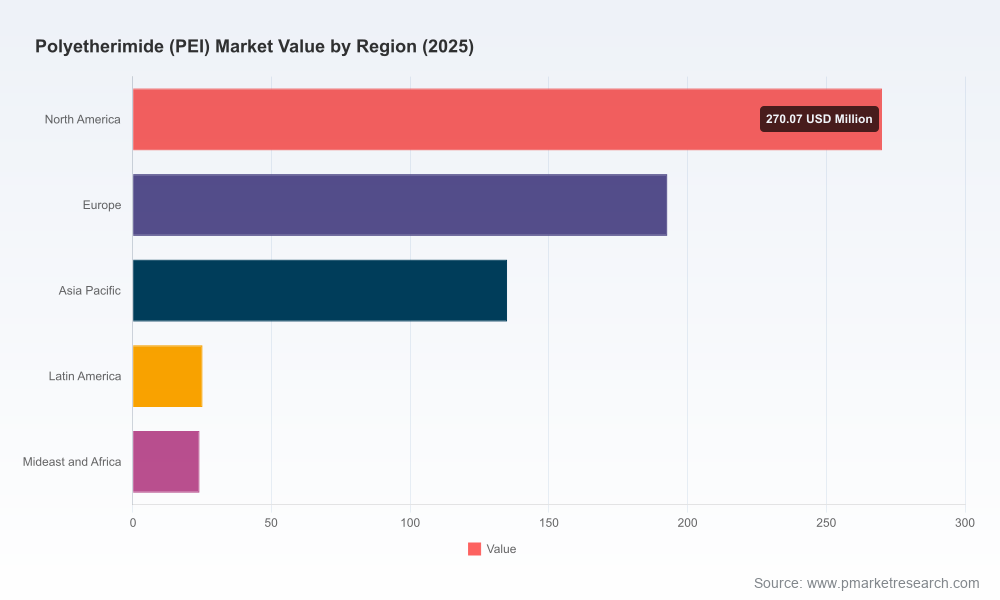

By 2025 the global Polyetherimide (PEI) market had consolidated a clear growth trajectory: the sector expanded steadily through the 2020–2025 period to reach an estimated global market size of approximately USD 646.7 million (base year 2025). Our forecast model shows continued expansion through 2032 at a compound annual growth rate (CAGR) of roughly 4.8%, underpinned by durable end‑market demand and new supply-side developments that will reshape cost, capacity and innovation dynamics. For corporate leaders contemplating capital allocation, partnerships or product roadmaps in 2026, this research provides a focused lens on where value is concentrating and where margin pressure will appear.

Polyetherimide (PEI) Market

Why this research matters for decisions in 2026

- Timing matters: 2026 sits at the inflection where new production capacity and novel PEI chemistries begin to alter availability and application economics — decisions taken this year will determine who captures the composite and high‑performance niches in the next three-to-five years.

- Risk versus opportunity: feedstock volatility and differentiated material capabilities create parallel risks (raw material price shocks, supply bottlenecks) and opportunities (new composite formulations, higher‑value applications). A deliberate strategy — informed by granular scenarios — is required to convert volatility into competitive advantage.

- Execution focus: the market’s moderate fragmentation and the concentration of technical know‑how in a handful of players mean successful entrants must combine supply security, product differentiation, and targeted go‑to‑market moves rather than broad commodity plays.

Core market signals and dynamics

Three interlocking dynamics will shape PEI economics in 2026 and beyond:

Polyetherimide (PEI) Market

- Demand acceleration in performance applications. Electrification in automotive, weight reduction drives in aerospace, and miniaturization/thermal management needs in advanced electronics continue to elevate demand for high-temperature, low‑creep materials like PEI. These use cases are moving from prototyping into scaled adoption, creating higher volume and stricter specification requirements.

- Supply-side transformation. Large-scale investments by incumbent producers and compounders are increasing global PEI availability. Notably, the entrance of new capacity in the Asia‑Pacific basin alters lead times and logistics economics for offshore buyers. Simultaneously, compounders and formulators are offering more application‑specific solutions that blur the line between resin vendor and systems supplier.

- Raw material and price pressure. PEI production depends on specialty raw inputs (e.g., bisphenol‑A dianhydride and aromatic diamines). As of mid‑2025, observable price differentials across regions reflected sustained feedstock pressure: reported U.S. price points were meaningfully higher per kilogram than several Asian and Japanese benchmarks. These differentials have direct consequences for sourcing strategy, hedging programs and cost pass‑through frameworks.

What the full PW Consulting report delivers (high‑value, operational intelligence)

Our market study combines macro forecasting with executable playbooks. Key, practical deliverables include:

Polyetherimide (PEI) Market

- Validated market size and a seven‑year forecast (2026–2032) with scenario variants that stress test demand under three macroeconomic and supply disruption profiles.

- Bottom‑up supply mapping and capacity tracking that identifies likely pinch points by product family and manufacturing technology (resin, compounding, molded components).

- Raw‑material sensitivity and pricing model tied to feedstock indices, enabling buyers and producers to simulate margin outcomes under different procurement strategies and pass‑through clauses.

- Technology and applications dossier: comparative properties of reinforced vs. unreinforced grades, resin vs. compounded solutions, and the commercial pathways for oligomeric reactive chemistries in composite systems.

- Commercial playbooks for B2B sellers: segmentation of customer value propositions, pricing strategies, contract structures (fixed vs indexed), and channel mixes for direct vs distributor routes.

- M&A and partnership prioritization framework with an actionable shortlist methodology to identify bolt‑on acquisitions, JV targets and preferred contract manufacturers aligned with specific strategic objectives.

- Supplier scorecards and a procurement due diligence checklist for Tier‑1 OEMs and compounders seeking supply security and technical collaboration.

Competitive landscape — what incumbents signal about market evolution

The current supplier ecosystem is a blend of global resin producers, specialty compounders and regional formulator/distributors. The market is neither a pure oligopoly nor fully commoditized; a small group of global players hold significant technical leadership while numerous regional competitors serve niche or localized demand.

- SABIC — As the industrial‑scale steward of the ULTEM™ family, SABIC’s strategy combines broad grade depth with recent capacity expansion and targeted product innovation. The company’s 2024 manufacturing investment in Asia‑Pacific materially increased global availability, and its 2026 launch of a reactive PEI oligomer for aerospace composites signals a push into value‑added, system‑level offerings. For partners and competitors, SABIC’s dual move — scale plus application‑specific chemistries — redefines competitive benchmarks for speed‑to‑market in aerospace and other high‑performance segments.

- RTP Company — A U.S.‑based custom compounder, RTP differentiates through tailored formulations and close collaboration with part designers. RTP-style players are uniquely positioned to capture OEM demand for application‑specific compounds where off‑the‑shelf resin grades fall short.

- Specialist suppliers and formulators (Ensinger, Mitsubishi Chemical Advanced Materials, Avient, PolyOne/Axyon, Centroplast, Röchling, Lehmann & Voss) — These firms occupy complementary roles: some supply branded resin lines and molded components; others focus on compound development, distribution and value‑added services. Collectively they reinforce a market structure where technical service and local presence can offset scale disadvantages.

Recent moves — especially large capacity additions and the introduction of reactive oligomers compatible with thermoset composite workflows — indicate that competition will increasingly play out on the product innovation and system integration front rather than conventional price levers alone.

Strategic implications and recommended actions for 2026

Based on our synthesis of demand signals, supply shifts and company positioning, we recommend the following priority actions for executive teams considering exposure to PEI in 2026.

- Secure multi‑tier sourcing and adopt dynamic procurement clauses. Given feedstock volatility and regional price differentials, buyers should establish multi‑source agreements and include indexed pricing triggers tied to feedstock indices. Parallelly, evaluate tolling or local compounding arrangements to reduce landed cost exposure.

- Invest selectively in application‑specific capabilities. For companies targeting aerospace and high‑temperature electronics, co‑development with resin innovators (especially firms offering reactive oligomers compatible with thermoset processes) can accelerate qualification and lock in tier‑one OEM programs.

- Differentiate through systems, not just resins. Successful players will bundle material supply with design support, molded parts expertise, or composite layup protocols. Consider building or acquiring compounding and molding capabilities rather than relying solely on traded resin purchases.

- Pursue regional presence aligned to customer clusters. The Asia‑Pacific capacity buildout has changed logistics economics; manufacturers that localize compounding or distribution can reduce lead times and improve responsiveness to OEM development cycles.

- Prioritize margin protection strategies. Use the report’s pricing model to stress test product‑level profitability under different raw material scenarios and implement contractual protections (caps/floors, hedging where feasible) for large OEM contracts.

- Evaluate consolidation and partnership plays. Market structure — moderate fragmentation with significant technical leadership at the top — favors bolt‑on M&A for firms looking to scale quickly into specialized segments. Joint ventures with established compounders can be a lower‑risk path to capability ownership.

How PW Consulting’s analysis reduces execution risk

Our report translates macro projections (the market’s established growth path through 2025 and our 2026–2032 forecast) into executable roadmaps. We combine quantitative models with vendor diligence and application‑level testing outcomes so that procurement, product and corporate development teams can take calibrated steps rather than speculative bets. For example, our raw‑material sensitivity module enables procurement to model the impact of a 10–25% feedstock move on product P&L and to design appropriate contract structures in response.

Next steps — where to find the detailed, proprietary intelligence

This briefing is designed as a strategic trailer: it highlights the pivotal forces and competitive moves firms must contend with in 2026 while deliberately withholding the full segmentation tables, regional and application revenue breakdowns, and the proprietary supplier scorecards that underpin our recommendations. For teams preparing capital budgets, sourcing decisions, or R&D roadmaps this year, accessing the full PW Consulting PEI Market study provides:

- Granular regional and application segmentation with scenario sensitivity;

- Supplier scorecards with capacity timelines, grade coverage and qualification hurdles;

- Compendium of commercial negotiation templates and a prioritized list of potential M&A targets and JV candidates.

Contact PW Consulting to obtain the full report and the companion workshops that translate strategic intent into a 12–18 month execution plan. In a market where supply shifts and material innovations are redefining value, having the right intelligence now will determine who leads the PEI value chain through 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Polyetherimide (PEI) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com