Discontinuous Screen Changers Market — Strategic Preview for 2026 Decision-Makers

As PW Consulting’s lead industry analyst, I present a strategic primer on the Discontinuous Screen Changers (DSC) market that frames the commercial and technological choices companies must make in 2026. This briefing synthesizes macro growth trajectories, competitive posture, regulatory pressures and practical tools contained in our full market study. It is designed to demonstrate the analytical rigor behind our findings while intentionally withholding granular segment-level detail to preserve the commercial value of the primary report.

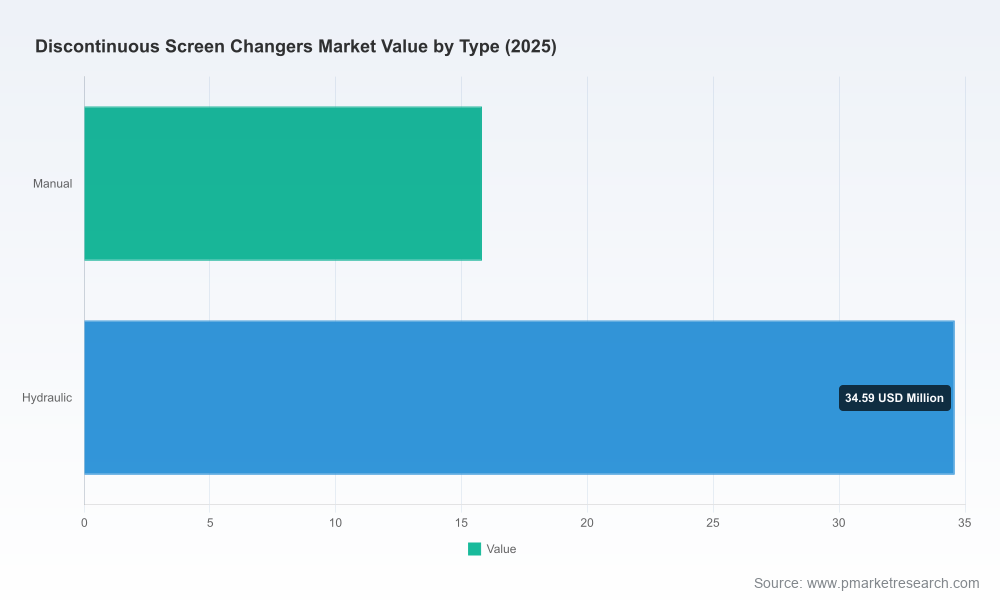

Discontinuous Screen Changers Market

Market snapshot: the headline numbers that matter for planning

The DSC market is no longer a niche of isolated machine rooms — it has matured into a steady, investible market for polymer processors, recyclers and OEMs integrating melt-filtration into extrusion platforms. From a base-year of 2025, when the market reached approximately USD 50.4 Million, the market shows a clear and sustained upward trajectory. Historically, the market expanded through the early 2020s from single‑digit tens of millions and is projected to grow at a compound annual growth rate (CAGR) of roughly 5.9% across the 2026–2032 forecast window. By the end of that horizon the market is forecast to approach the mid‑seventies (USD 74.8 Million), reflecting steady demand for filtration across packaging, recycling and specialty polymer extrusion.

Discontinuous Screen Changers Market

Why these headline metrics matter in 2026: they convert uncertainty into scale. A mid-single-digit CAGR coupled with measured absolute growth supports investment programs that are neither speculative nor stagnant — ideal for targeted product development, regional footprint optimization and supplier consolidation strategies.

Discontinuous Screen Changers Market

Strategic dynamics shaping the 2026 agenda

- Recycling and quality standards are reshaping demand patterns. Investment by recyclers and closed-loop packaging initiatives is increasing the need for robust melt filtration. At the same time, rising food‑contact and pharmaceutical packaging requirements push OEMs towards more dependable filtration, even when discontinuous solutions are chosen for cost or process reasons.

- Technology convergence: automation, AI and system integration. Recent collaborations between equipment manufacturers and polymer producers are accelerating the migration from purely mechanical designs toward systems that incorporate sensors and predictive analytics for filtration performance and downtime reduction. These capabilities are emerging as differentiators in procurement processes.

- Choice architecture: discontinuous versus continuous trade-offs. Discontinuous screen changers remain attractive where capital cost, simplicity and batch operations dominate. However, buyers must weigh these advantages against higher operational interruption costs in high‑throughput environments — a calculus that will determine whether to retain, retrofit or replace DSCs in 2026 projects.

- Market structure and consolidation pressure. The DSC market exhibits meaningful concentration: the top three players collectively account for nearly half of the market, and the top five represent well over 60%. This structure implies that strategic partnerships, selective M&A and alliance-building will be effective levers for scale-seeking suppliers and for end-users seeking supply security.

Regulatory and sustainability levers

- Safety and performance directives. The EU Machinery Directive and related regional safety standards, current through 2025 updates, continue to raise the bar for mechanical safety and machine performance. Manufacturers are incorporating compliance readiness as a default requirement for new installations.

- Substance restrictions and material stewardship. REACH and allied regulations compel vendors to validate materials and components used in screen changers. This has downstream implications for supplier selection and lifecycle documentation requested by large polymer converters.

- Energy and waste considerations. Environmental rules and corporate sustainability targets are creating a paradox for discontinuous systems: while lower upfront capital cost can attract buyers, the operational profile of discontinuous systems — notably energy consumption during restarts and throughput interruptions — will increasingly factor into total cost of ownership (TCO) assessments and procurement decisions.

Competitive landscape — who matters and why

The market features a mixture of global OEMs, specialized filtration vendors and regional producers. Strategic positioning varies from integrated extrusion system suppliers to component-focused firms that serve retrofit markets. Key players covered in our study include:

- Nordson Corporation (United States) — https://www.nordson.com. Known for BKG® NorCon™ discontinuous piston screen changers tailored to extrusion lines that require intermittent screen changes, Nordson’s channel strength and aftermarket reach make it a natural focal point for strategic sourcing.

- MAAG (Switzerland) — https://maag.com. MAAG’s DSC portfolio emphasizes single-piston robustness for demanding polymer processes; the firm’s engineering pedigree positions it well for OEM partnerships and high-reliability applications.

- Trendelkamp Technology (Germany) — https://www.trendelkamp.com. Trendelkamp’s hydraulically assisted devices (TSD/TASD) represent a performance-oriented approach that appeals to quality‑sensitive converters and equipment integrators.

- PSI-Polymer Systems (United States) — https://www.psi-polymersystems.com. PSI focuses on DSCs suited to batch polymer and hot-melt adhesive operations where accessibility and ease of maintenance are prioritized.

- EREMA (Austria) — https://www.erema.com. With systems integrated into recycling and extrusion lines, EREMA’s melt-filtration expertise supports circular-economy projects and large-scale recyclers.

- Parkinson Technologies (United States) — https://parkinsontechnologies.com. Parkinson’s Key Filters brand serves thermoplastic extrusion lines with modular DSC solutions optimized for retrofit scenarios.

- Alpha Marathon (Canada), ECON (China) and JC Times (China) — regional manufacturers that compete on cost, local service and fast delivery for small-to-mid-scale processors in their respective markets.

Recent market moves underscore these strategic themes: partnerships between machinery OEMs and major polymer producers to co-develop next‑generation filtration, turnkey contract wins for extrusion lines with advanced discontinuous screen changers, and product launches that emphasize pressure-drop reduction and reduced downtime. These events signal vendor focus on differentiating through system-level integration rather than component feature lists alone.

What the full PW Consulting study delivers — practical content for 2026 action

Our full report is engineered to be a working document for executives, product managers and procurement leads. Highlights include:

- Proprietary market-sizing and forecasting methodology (base year 2025; historical window 2020–2025; forecast 2026–2032) with scenario analyses to stress-test investment cases.

- Supplier benchmarking and scorecards that evaluate capability across engineering quality, aftermarket support, integration readiness and compliance documentation.

- TCO models and upgrade/retrofit decision frameworks that allow users to compare discontinuous and continuous approaches across throughput, downtime, energy and capital metrics.

- Regulatory and standards matrix covering machinery directives, substance restrictions and food-contact requirements to streamline supplier pre‑qualification and risk assessment.

- Procurement playbooks and negotiation levers tailored to OEMs, recyclers and contract manufacturers, including contract clauses for performance guarantees, spare-parts availability and firmware/sensor IP.

- Case studies and engineering notes from recent projects illustrating how to reduce pressure-drop, accelerate screen change workflows and integrate predictive filtration monitoring.

Note: This preview intentionally omits the chapter containing granular regional splits, application-level volumes and unit-price matrices. Those sub-segment models are a central value proposition of the full report and are available through the report landing page.

How buyers and suppliers should use this intelligence in 2026

- Buyers (Converters, Recyclers, OEMs): Use the report’s TCO and scenario tools to determine where DSCs remain the optimal choice and where investments in continuous filtration or hybrid architectures pay off. Prioritize suppliers with demonstrated integration capability and documented regulatory compliance.

- Suppliers and OEMs: Differentiate by offering integrated solutions — sensorized DSCs, quicker-change ergonomics, partnership-based service models — and by clarifying aftermarket promises (spare parts, turnaround times, digital diagnostics) that matter to large converters.

- Investors and M&A teams: Leverage market concentration data to identify scale targets and geographic coverage gaps. The current market structure rewards add‑on acquisitions that fill capability or regional-service voids.

Closing perspective and next steps

In 2026 the Discontinuous Screen Changers market presents a pragmatic growth opportunity: steady expansion, concentrated supplier positions and accelerating system-level differentiation. Strategic winners will be those who translate headline growth into usable procurement and engineering actions — adopting decision frameworks that balance capital outlay with operational continuity and regulatory compliance.

PW Consulting’s full Discontinuous Screen Changers Market report contains the segment-level intelligence, unit economics, supplier scorecards and executable playbooks omitted from this preview. For procurement teams, technical leads and corporate strategists preparing budgets and roadmaps in 2026, the full report converts these macro insights into immediately actionable workstreams.

To access the comprehensive dataset, proprietary models and appendices referenced above, consult the report landing page where full segmentation, per-region and per-application matrices, and downloadable Excel models are available.

For detailed analysis of this topic, please visit the official page:Discontinuous Screen Changers Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com