Cutting Boards Market — 2026 Strategic Preview

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present a forward-looking synthesis of the Cutting Boards Market intended to sharpen executive decision‑making in 2026. This preview highlights the structural forces, competitive dynamics, and near‑term tactical levers that will determine winners and losers—while intentionally withholding the granular segment and regional breakouts contained in our full market study to encourage direct access to the detailed modeling and tables.

Cutting Boards Market

Market snapshot (what the numbers mean for strategy)

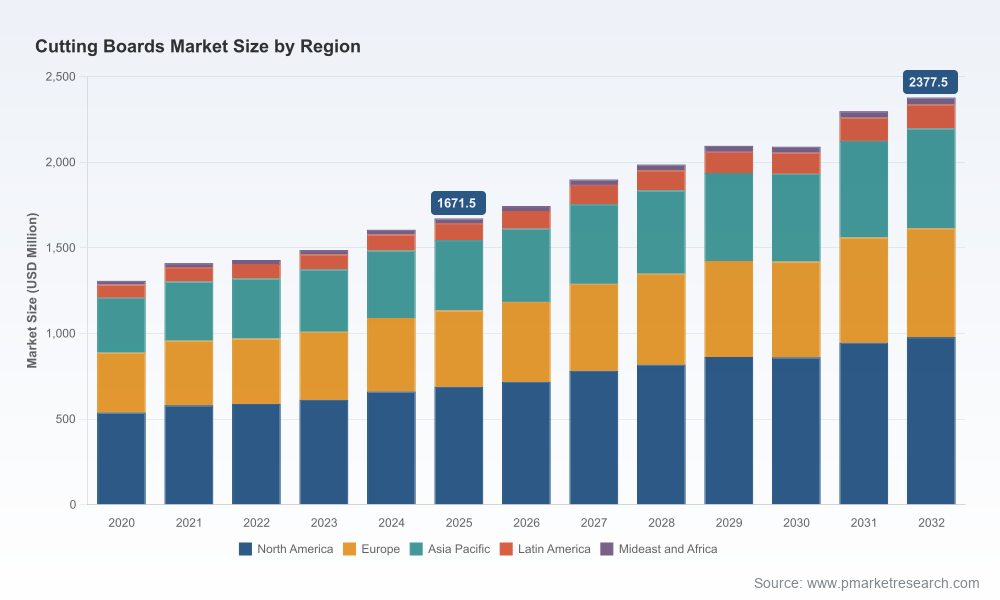

Using 2025 as our base year, PW Consulting’s study tracks the cutting boards market across a 2020–2025 historical window and produces a 2026–2032 forecast. At a compounded annual growth rate (CAGR) of 5.16% for the forecast horizon, the market demonstrates steady, mid‑single‑digit expansion driven by a mix of household replacement cycles, foodservice investment, and product premiumization. Measured in USD Million, the market rose from approximately 1.31 billion in 2020 to about 1.67 billion in 2025, with our 2026 estimate at roughly 1.74 billion and a 2032 projection approaching 2.38 billion.

Cutting Boards Market

Those headline figures are important for budget allocation and sizing initiatives: they indicate a market large enough to justify dedicated product R&D and channel investment, yet sufficiently fragmented to leave space for targeted premium plays and scale-enabled cost players. In short, organizations must balance growth capture and margin protection simultaneously in 2026.

Cutting Boards Market

Macro and industry forces shaping 2026 choices

- Material innovation and hygiene expectations: New surface technologies and engineered composites—ranging from NSF‑certified paper composites to titanium and advanced fiber materials—are altering value propositions. Recent independent verifications and university research have shifted the hygiene narrative: validated antimicrobial properties for certain hardwoods and zero‑microplastic claims for some composites change acceptance thresholds among foodservice buyers and health‑conscious consumers.

- Standards and regulation tightening: The 2025 revision of NSF/ANSI 51 introduced more specific language on glass and glass‑like materials used in food equipment, with ripple effects for manufacturers and specifiers. Simultaneously, existing public‑health guidance (e.g., USDA FSIS) continues to emphasize proper use over material absolutism—creating a compliance environment where certification and well‑documented use‑cases are decisive procurement filters.

- Raw material volatility: Hardwood lumber saw marked price swings through 2021–2025, with specific species exhibiting >35% peak price movements. That volatility compresses margin for hardwood‑centric producers and shifts the economics of substitution (bamboo, composites, engineered plastics).

- Microplastics and sustainability scrutiny: Academic work showing differential microplastic shedding across polymers has increased buyer sensitivity to polymer selection and lifecycle statements. Brands that can demonstrate low emission during use and end‑of‑life circularity gain both regulatory and consumer credibility.

- Channel evolution and premium DTC demand: Consumers are paying for design, customization, and provenance; at the same time, commercial buyers prioritize durability, sanitation certification, and total cost of ownership. These divergent demands place a premium on multi‑channel product architectures and modular SKUs.

Competitive landscape — archetypes and implications

The competitive field is diverse: handcrafted hardwood artisans, engineered composite specialists, scaled bamboo suppliers, NSF‑certified plastic players, and private‑label/wholesale manufacturers coexist. The following archetypal mappings synthesize the strategic posture of leading names we track (profiles summarized from public sources and market activity):

- Premium hardwood artisans (e.g., John Boos & Co., J.K. Adams, The Boardsmith, Catskill Craftsmen): These firms compete on provenance, craftsmanship, and institutional trust (including longstanding commercial foodservice relationships). Their strategic advantage is brand equity and product differentiation, but they are exposed to hardwood supply swings and rising production costs.

- Engineered/composite specialists (e.g., Epicurean, The Cutting Board Company / Richlite): Offering NSF‑certified or independently verified hygiene and performance claims, these players excel at selling into regulated commercial channels and health‑sensitive consumer segments. Their playbook is certification, performance testing, and articulating lifecycle impacts.

- Sustainable scale players (e.g., Totally Bamboo, Proteak, Lipper International): These companies leverage material sustainability narratives and cost efficiencies (bamboo, managed plantations, or mixed materials). They are positioned to win mainstream retail shelf space and price‑sensitive DTC segments.

- Wholesale and private‑label manufacturers (e.g., Adeo Wood Products): Focused on volume, customization for retailers, and charcuterie trends, these firms are natural partners for retailers seeking margin improvement and rapid SKU variety.

- Innovators and new‑entrants (Titan Cut Pro, KatuChef, STEELPORT expansions): Recent product launches and surface innovations (titanium, medical‑grade surfaces, 2‑in‑1 systems) are testing the boundaries of material science and marketing claims, prompting incumbents to reassess R&D investment.

Strategic implication: incumbents that combine trusted hygiene credentials, resilient raw material sourcing, and clear sustainability claims will dominate specification lists for commercial buyers, while nimble DTC brands can capture premium household spend through design and personalization.

What the PW Consulting Cutting Boards Market report delivers (practical, plug‑and‑play content)

- Scenario‑based revenue forecasts (2026–2032) across macro assumptions—available at national and segment levels in the full report—enabling investment case modeling and sensitivity analysis for pricing and volume shocks.

- Supplier risk and cost‑pressure heatmaps that quantify exposure to hardwood price swings, wood supply chains, and polymer feedstock variability, along with recommended hedging and sourcing playbooks.

- Product portfolio prioritization framework: SKU rationalization logic, margin‑vs‑growth matrices, and recommended SKU architectures for mixed channel strategies (retail, foodservice, DTC).

- Regulatory and standards compliance toolkit covering NSF/ANSI 51 (2025) implications, certification timelines and cost estimates, plus sample technical dossiers to accelerate spec wins with commercial buyers.

- Innovation tracker that ranks new material technologies (paper composites, Richlite, titanium finishes, advanced HDPE blends) by maturity, cost impact, and hygiene profile—paired with supplier shortlists for co‑development.

- Go‑to‑market playbooks for three priority buyer types: premium consumers, national foodservice chains, and private‑label retail buyers—complete with sample pitch decks and channel economics models.

- An M&A and partnership screening matrix identifying targets by strategic fit—complemented by valuation heuristics and integration checklists to accelerate inorganic growth.

Seven strategic priorities for 2026 (executive checklist)

- Hedge material cost and diversify supply: Lock long‑dated contracts for critical species or accelerate substitution strategies (bamboo/composites) where lifecycle analysis supports equivalence.

- Invest in hygiene certification: Secure NSF/ANSI or equivalent verification early for commercial product lines; fund independent testing that addresses microplastic shedding and antimicrobial performance for consumer marketing claims.

- Rationalize SKUs and upsell premium tiers: Reduce underperforming SKUs, introduce modular premium options (edge finishes, personalization), and price to capture rising consumer willingness to pay for design and provenance.

- Develop channel‑specific products: Create separate architectures for foodservice (durability, sanitation, total cost of ownership) versus retail/DTC (design, gifting, customization).

- Leverage sustainability for differentiation: Publish lifecycle analyses, pursue credible third‑party claims (e.g., verified low microplastic emissions, certified sourcing), and pilot circular take‑back programs.

- Explore adjacent product plays and co‑branding: Partnerships with knife manufacturers, foodservice equipment suppliers, and premium kitchen retailers can amplify distribution and brand resonance.

- Assess consolidation opportunities: Where scale benefits procurement or certification costs are significant, prioritize bolt‑on M&A to acquire engineered material competence, certification status, or high‑value commercial accounts.

Why PW Consulting’s report matters for 2026 decision cycles

Boardrooms and product leadership teams will face tradeoffs in 2026 between margin protection and growth capture. Our study provides the evidence base—forecasting scenarios, cost impact analyses, certification timelines, and competitor strategic positions—to move from intuition to executable strategy. The preview above surfaces the high‑level implications; the full report contains the granular segmentations, regional forecasts, and SKU‑level modeling that procurement, R&D, and M&A teams require to action these priorities with confidence.

To convert these insights into a 90‑day execution plan or a three‑year portfolio strategy, contact PW Consulting for the full report and a tailored briefing. The market is expanding and evolving: companies that align material strategy, certification, and channel configuration early will capture disproportionate value as the market matures through 2026 and beyond.

For detailed analysis of this topic, please visit the official page:Cutting Boards Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com