DIN Rail Terminal Blocks Market — Strategic Briefing for 2026 Decision-Makers

As companies plan investments, product roadmaps, and supply‑chain commitments for 2026, a clear understanding of the DIN rail terminal blocks market is essential. This briefing distills the strategic takeaways from PW Consulting’s full DIN Rail Terminal Blocks Market study (base year 2025, historical window 2020–2025, forecast 2026–2032). It demonstrates how a quantitative growth narrative, competitive mapping, materials & regulation dynamics, and actionable playbooks converge into high‑confidence choices for product, commercial and M&A leaders. Note: this introduction surfaces the study’s methodology, trends, and implications while intentionally withholding granular segment figures — consult the full report for the detailed numerical breakdowns that underpin recommended actions.

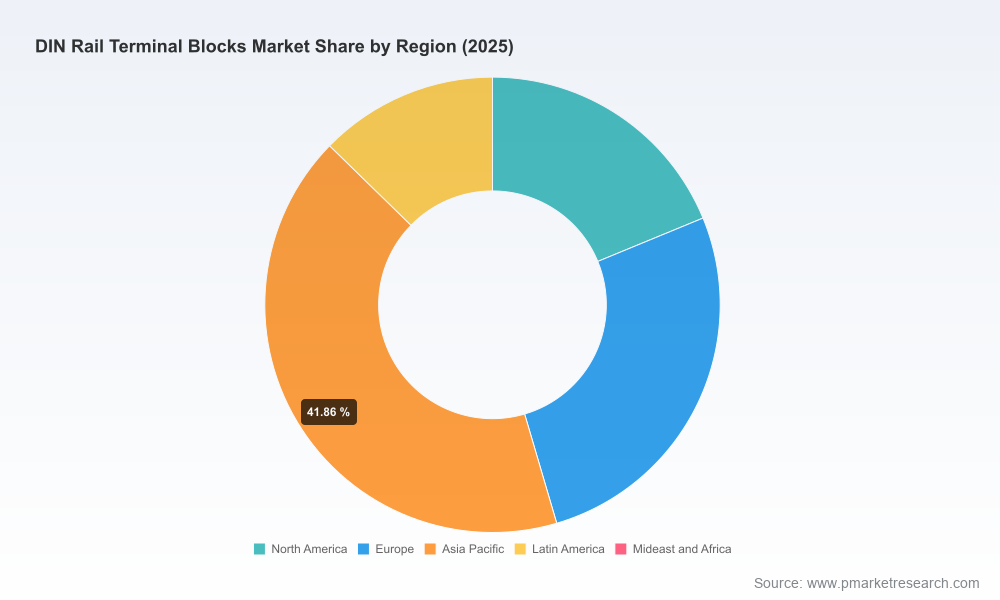

DIN Rail Terminal Blocks Market

Market trajectory: a clear growth runway

The market for DIN rail terminal blocks has shown steady expansion through the early 2020s, with our historical series tracking growth from roughly USD 1.62 billion in 2020 to around USD 2.15 billion in 2025 (base year). Looking ahead, the market is projected to continue on an upward path, reaching approximately USD 3.19 billion by 2032. The forecast period (2026–2032) assumes a compound annual growth rate (CAGR) of 5.8%, reflecting robust demand driven by industrial automation, electrification of infrastructure, and modernization of legacy control cabinets.

DIN Rail Terminal Blocks Market

For executives, the arithmetic is instructive: the market’s steady expansion creates capacity for new product introductions, higher value engineering, and selective regional investments — but it also rewards focus. Growth at this scale supports multiple winners; it does not guarantee success for undifferentiated suppliers.

DIN Rail Terminal Blocks Market

Competitive structure and what it means for strategy

- Market concentration: The top three players account for a mid‑teens to low‑twenties share of the market (CR3 ~27%), and the top five reach roughly a third (CR5 ~32%). This indicates a market that is neither highly consolidated nor atomized — an economically attractive zone for both incumbent expansion and targeted new entrants.

- Incumbent strengths: Established names such as Phoenix Contact, Weidmüller, WAGO, Molex, TE Connectivity, ABB and regional leaders like Dinkle exhibit complementary strengths. These range from system platforms and patented connection technologies to broad channel networks and regulatory pedigree. Their R&D roadmaps emphasize modularity (push‑in, spring cage, screw variants), power distribution modules, and “smart” terminal blocks for condition monitoring.

- Strategic inference: Given the moderate concentration, strategic plays that have high ROI potential include bolt‑on acquisitions to complete product portfolios, selective licensing of connection technologies, and regional partnerships that expedite certification and localization.

Technology and product vectors to prioritize in 2026

- Connection technology differentiation: Push‑in and spring‑cage connection systems compete on speed of wiring, maintenance ergonomics, and resistance to vibration. Screw‑type solutions retain relevance for high‑torque, legacy applications. Companies should map product specifications against prioritized verticals (industrial automation, rail, power distribution) to avoid feature bloat.

- Modularity and systemization: Leading vendors promote platform strategies (e.g., multi‑technology carriers, combinable blocks, and integrated power distribution modules). For OEMs, platform compatibility reduces engineering overhead; for component suppliers, it raises switching costs — a desirable commercial dynamic.

- “Smart” enablement: Terminal blocks with sensing/communication capabilities are emerging as value‑add layers (condition monitoring, temperature and torque sensing). Early pilots exist; 2026 is the window to test integrations with PLC/edge ecosystems and to quantify the willingness to pay among system integrators.

Supply chain, materials and compliance — immediate operational levers

- Materials reality: Housings are predominantly high‑performance thermoplastics meeting flammability classifications (UL94 V‑0), while conductive parts use corrosion‑resistant copper alloys, zinc‑plated brass and similar metals. Material selection influences cost, manufacturability, and certification timelines.

- Standards and approvals: International standards (e.g., IEC 60947‑7‑1/7‑2/7‑3 and UL 1059) govern spacing, temperature rise, dielectric withstand, and pull‑out tests. Leading suppliers often exceed these thresholds, which shortens time‑to‑market for their OEM customers — a commercial differentiation worth quantifying when selecting suppliers.

- Risk mitigation: For procurement teams, three immediate actions are recommended: diversify metal alloy sourcing to reduce exposure to copper volatility; qualify alternative polymer suppliers to avoid single‑source shocks; and prioritize suppliers with demonstrated testing records and cross‑jurisdiction approvals to minimize re‑testing costs for global projects.

Competitive snapshots and tactical implications

- Phoenix Contact (Blomberg, Germany): Known for multi‑technology CLIPLINE systems and Push‑X innovations. Strategic implication — partner or benchmark on modular system architecture and certification depth.

- Weidmüller (Detmold, Germany): Strength in Klippon Connect series and diverse feed‑through/power terminal offerings. Strategic implication — examine their approach to marine/rail certifications for new vertical entry.

- WAGO (Herzogenaurach, Germany): Push‑in CAGE CLAMP® technology in the TOPJOB S family emphasizes installation speed. Strategic implication — consider speed and ergonomics as core differentiators in service‑intensive segments.

- Molex (Aurora, Illinois, USA): Focused on industrial power connectivity; commercially strong in North American OEM channels. Strategic implication — evaluate channel partnerships in targeted OEM verticals.

- Dinkle (Taiwan): Active in modular push‑in designs and visible at regional trade events. Strategic implication — regional sourcing or joint‑development agreements can fast‑track price–performance wins.

- TE Connectivity and ABB: Large incumbents emphasizing power distribution blocks and smart terminal solutions; they are natural partners for electrification programs and large system integrators.

Recent market activity underlines these dynamics. Industry showcases through 2025, including product launches and trade‑show rollouts, indicate supplier focus on modular push‑in architectures and automation‑friendly features. For competitive strategy, treat trade events and product showcases as intelligence nodes — early signal of roadmaps and certification priorities.

What the full report delivers (operationally actionable)

PW Consulting’s full study translates market dynamics into operational workstreams that product, commercial, and corporate strategy teams can immediately adopt. Key contents include:

- Granular demand modelling: time‑series data (2020–2025 historical), base‑year normalization (2025), and scenario forecasts through 2032 segmented by technology, application and region (note: segmented figures are available only in the full report).

- Vendor deep dives: 360° profiles for leading suppliers, including product line maps, patented technologies, distribution models, and a comparative vendor scorecard for selection and sourcing decisions.

- Supply‑chain heatmaps: bill‑of‑materials sensitivity (key metals and polymers), supplier concentration analysis, and alternative sourcing playbooks tied to procurement lead times and cost delta estimates.

- Regulatory & testing matrix: which standards matter by end market and how long typical certification cycles take — essential for go‑to‑market sequencing and capex planning.

- Commercial playbooks: pricing archetypes, channel strategies, and value‑capture approaches for OEMs, panel builders, and electrical contractors.

- M&A and partnership signal engine: prioritized list of subscale targets, rationales and estimated accretion timelines for inorganic growth.

- Engineering comparators & case studies: side‑by‑side technical comparisons (torque, current rating, wiring density), and diagnostics from real installations to guide product roadmaps.

How to use these insights in 2026 planning

- Product roadmap prioritization: Target a limited set of high ROI features (e.g., reduced wiring time via push‑in systems, or integrated power distribution modules) and validate with two pilot customers before full commercialization.

- Procurement & manufacturing: Lock multi‑year raw‑material agreements for critical alloys and polymers; qualify a second supplier in a different geography to lower geopolitical and logistic risk.

- Channel and go‑to‑market: For premium “smart” blocks, focus on system integrators and panel builders that can demonstrate value capture. For commodity offerings, optimize unit economics through contract manufacturing and volume discounts.

- M&A & partnerships: Use the moderate concentration environment to pursue tuck‑ins that add complementary technologies (sensing, power distribution) or expand certification portfolios.

Conclusion — what this means for decision‑makers

The DIN rail terminal blocks market presents a predictable growth corridor underpinned by automation and electrification trends. The environment favors firms that combine engineering differentiation (connection tech, modular platforms, smart features) with pragmatic supply‑chain discipline and targeted commercial execution. PW Consulting’s full report supplies the granular segmentation, financial models, vendor scorecards, and certification roadmaps needed to convert the market’s growth into profitable scale. This briefing has sketched the strategic contours; the complete dataset and tactical annexes are required to operationalize the recommended moves.

To access the full numerical breakdowns, vendor profiles, and tactical templates that enable 2026 budget approvals and product launches, please refer to the PW Consulting report page. Our team stands ready to run tailored workshops that map these insights directly to your portfolio, channel footprint, and M&A appetite.

For detailed analysis of this topic, please visit the official page:DIN Rail Terminal Blocks Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com