Moving Beyond Paper Permits: A Smarter Approach to Safer Operations

Other |

2026-04-08 11:21:01

As PW Consulting’s lead industry analyst, I present a focused strategic preview of our Advanced Wound Dressings Market study—designed to orient executive teams, corporate development leaders, and product strategists preparing plans and capital allocations for 2026. This preview synthesizes the market’s macro trajectory, regulatory and reimbursement inflection points, competitive posture, and the practical intelligence included in the full report. It deliberately illustrates analytical depth while withholding the full segment-level tables and modeling that drive transaction-grade decisions—those are accessible through our full study and interactive data package.

Advanced Wound Dressings Market

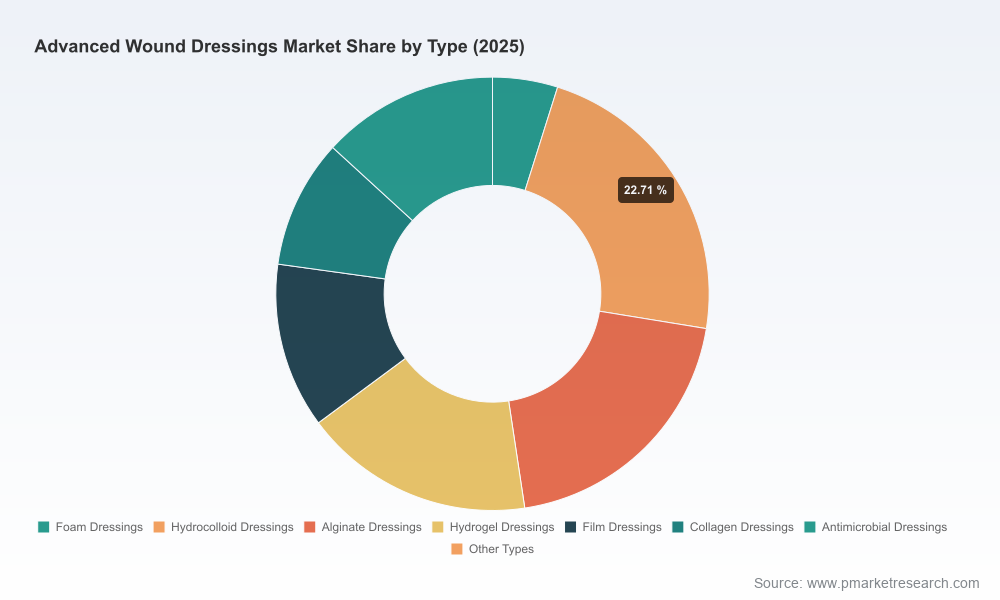

Between 2020 and 2025 the advanced wound dressings market expanded from roughly USD 7.7 billion to approximately USD 9.8 billion (base year 2025). The market enters the 2026–2032 forecast window with momentum that translates into a compound annual growth rate (CAGR) of about 6.5% through 2032, reaching approximately USD 14.9 billion by the end of the forecast period. That growth reflects a mix of demographic tailwinds, rising incidence and clinical recognition of chronic wounds, and steady product innovation across dressing technologies.

Advanced Wound Dressings Market

Capital allocation: A 6.5% multi-year growth baseline allows risk-adjusted investment in R&D and manufacturing capacity without relying on hypergrowth assumptions—critical for capex-heavy, compliance-constrained product roadmaps.

Advanced Wound Dressings Market

Portfolio prioritization: Executives must weigh incremental returns of incremental product variants versus platform investments (e.g., antimicrobial chemistries, hydrofiber matrices, multilayer foams) informed by our segment-level demand curves and margin models.

M&A and partnership timing: Market concentration metrics indicate a consolidated leader set—top three firms capture a majority share while top five approach three-quarters of the market—making strategic acquisitions a viable fast-track for scale and distribution reach.

Reimbursement paradigm shift: The CY 2026 Physician Fee Schedule Final Rule has materially changed payment for many cellular and tissue-based products (CTPs), reclassifying them from ASP+ models to an 'incident-to supplies' reimbursement with a fixed per-square-centimeter rate. That reclassification diminishes price dispersion between brands for applicable product types and places a premium on cost-to-serve, outcomes documentation, and bundled-care value propositions.

Regulatory and standards alignment: Regulators and standards bodies are converging on specific sterilization and antimicrobial testing frameworks. Notably, the FDA’s acknowledgement of ISO 22441:2022 for low-temperature vaporized hydrogen peroxide sterilization offers a clearer regulatory pathway for manufacturers using that modality. Concurrently, EN 17854:2024 establishes minimum antimicrobial activity requirements and a test method—raising the bar for claims and driving standardization of comparative evidence.

Clinical and commercial evidence expectations: Payers and health systems now demand real-world evidence linking dressing selection to measurable resource savings (reduced dressing-change frequency, fewer infections, shorter healing timelines). Companies that align clinical data generation with payor-focused economic endpoints create defensible commercial differentiation.

The market is led by well-capitalized medical-device companies with complementary strengths: product innovation, global manufacturing, direct provider relationships, and distribution partnerships. Our study profiles each core player and assesses where they are likely to compete and to cooperate in 2026 and beyond.

Smith & Nephew — Known for layered foam platforms and integrated wound-care systems; recent launches demonstrate a focus on multi-functional dressings designed to simplify clinician workflows. Their global sales footprint and clinical partnership model position them to monetize scale-driven RWE programs.

3M — Brings adhesive and thin-film technologies, with differentiation in adhesive science and skin-interface ergonomics. 3M’s strength is translating material science into user-friendly formats that reduce per-procedure time and device-associated complications.

Coloplast — Competes on niche, clinician-focused product design and close ties with ostomy and continence channels; their approach emphasizes patient comfort and long-dwell solutions that align with home-care delivery models.

Mölnlycke Health Care — Strong in advanced dressing matrices and surgeon-facing product lines; their global reach and investments in clinician education are key advantages in surgical and acute-care segments.

DeRoyal Industries — An agile manufacturer with flexible production capability and a value-oriented portfolio; well-suited to capture demand from cost-constrained channels and private-label partnerships.

Avery Dennison — Leverages materials science and adhesive platform capabilities to deliver differentiated dressing interfaces and intelligent labeling solutions that aid inventory and usage tracking.

ConvaTec — Focused on hydrofiber and biologically active matrices; recent regulatory clearances and product updates position them to expand share in both acute and chronic wound pathways.

Recent industry activity underscores the competitive themes above: early-2025 and mid-2025 regulatory clearances and product launches (including new chitosan-based devices receiving 510(k) clearance and major firms launching multi-layer foam offerings) highlight the ongoing race for claimable clinical benefit and simplified clinician workflows.

The full report is built for practitioners. Highlights include:

Granular demand models (2020–2032) with downloadable scenario-based Excel workbooks that allow users to stress-test pricing, reimbursement, and volume assumptions.

Segment-level demand and margin analysis across product types and applications (with adjustable inputs to model alternative reimbursement scenarios).

Comprehensive competitor intelligence: product portfolios, recent launches and clearances, patent landscaping, manufacturing footprint, and route-to-market assessments.

Regulatory and standards tracker with actionable compliance timelines (including implications of ISO 22441:2022 and EN 17854:2024 for product claims and sterilization strategy).

Reimbursement playbook: payer segmentation, coding and billing implications of the 2026 Physician Fee Schedule changes, and negotiation tactics for bundled-care contracts.

Commercialization blueprints: clinical evidence plans, KOL engagement frameworks, digital wound-assessment pilots, and contracting templates for IDNs and home-care providers.

Supply chain and sourcing risk maps with near- and mid-term mitigation strategies for raw-material volatility and capacity constraints.

M&A and partnership screening matrices calibrated to maximize scale, fill portfolio gaps, or accelerate access to high-growth channels.

Practical checklists and KPIs to operationalize the strategy—including time-bound milestones for regulatory filings, clinical studies, and reimbursement negotiations.

Re-price and redesign for the new reimbursement baseline: Where CTP reimbursement has been standardized, companies should shift from monetizing premium brand differentials to optimizing cost-to-serve, improving clinical efficiency, and demonstrating downstream savings.

Invest selectively in sterilization and antimicrobial claim proof: Adoption of recognized sterilization standards and alignment with EN 17854 antimicrobial testing will reduce regulatory friction and strengthen clinical claims; prioritize investments that accelerate compliance.

Double down on RWE that ties to cost outcomes: Real-world studies that show fewer dressing changes, reduced infection rates, or shorter healing times will be decisive in contracting with payers and health systems.

Use M&A to fill capability gaps rather than to chase volume alone: Given the market’s concentration, targeted acquisitions—manufacturing scale, adhesive platform enhancements, or digital wound-assessment capabilities—can be higher-return than broad bolt-on deals.

Prepare for an outcomes-based commercial model: Pilot bundled-care agreements with a small set of IDNs that include outcome KPIs and shared-savings constructs to de-risk broader price pressure.

Optimize channels for home care growth: The shift toward outpatient and home-based wound management favors products that simplify administration and reduce dressing-change frequency—retool commercialization and distribution accordingly.

For executives preparing 2026 budgets and strategic plans, the central question is not whether the market will grow—the macro baseline and multi-year runway are clear—but how to capture durable, margin-accretive share as reimbursement, standards, and clinical expectations tighten. Our full PW Consulting Advanced Wound Dressings Market report supplies the operational models, competitor playbooks, and regulatory timelines necessary to convert insight into executable actions.

To explore the full dataset, interactive models, and bespoke advisory options that support M&A diligence, portfolio optimization, and reimbursement negotiations, access the full report and accompanying Excel workbooks on the PW Consulting portal.

For detailed analysis of this topic, please visit the official page:Advanced Wound Dressings Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com