Why Gold Trading Remains One of the Most Sought-After Markets

Other |

2026-02-05 18:06:54

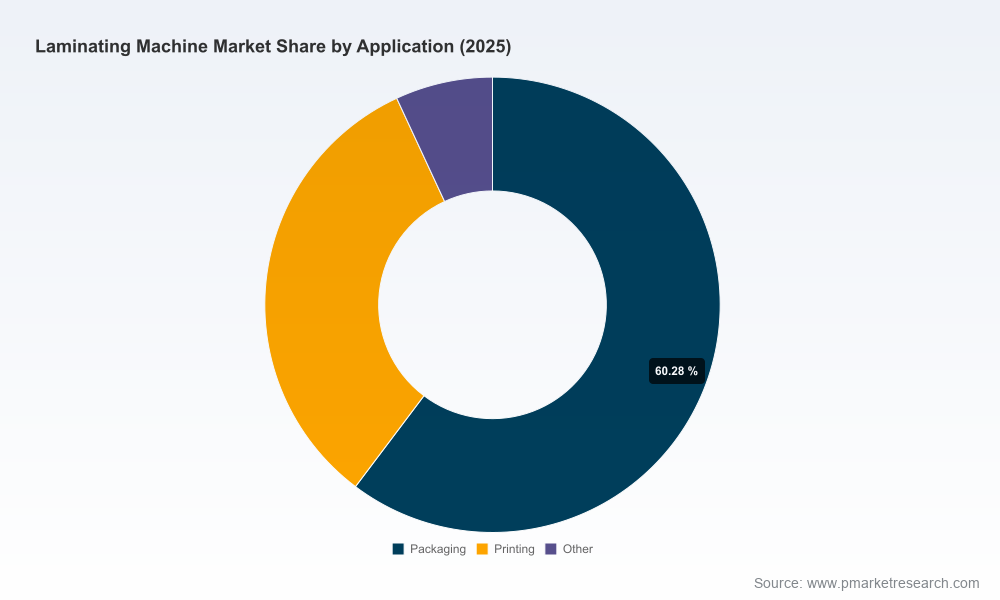

As companies finalize 2026 capital plans and update their procurement playbooks, the laminating machine market presents a mix of steady growth, accelerating technology turnover, and regulatory-driven demand shifts. PW Consulting’s upcoming market study — built on a 2025 base year and a 2026–2032 forecast horizon — synthesizes macro-market sizing, competitive positioning, technology trajectories, and operational levers. Our projections indicate the global laminating machine market expanded from roughly USD 530 million in 2020 to about USD 676 million in 2025, and is expected to grow at a compound annual growth rate (CAGR) of approximately 5.0% through 2032, approaching a near‑billion-dollar industry by the end of the forecast period. This briefing outlines the strategic value of that research for executives shaping decisions this year, while intentionally reserving detailed segment tables and line-level forecasts to the full report.

Laminating Machine Market

Investment prioritization under moderate growth: With a predictable mid-single-digit CAGR, the market rewards focused investments that improve throughput, reduce operating cost per meter, or unlock new low‑margin high‑volume applications. Our study translates headline growth into actionable investment scenarios—helping CFOs and plant leaders size ROI windows for retrofit vs. greenfield options.

Laminating Machine Market

Procurement negotiation and total cost of ownership (TCO): Equipment price competition remains intense, especially between established European OEMs and high-volume Asian manufacturers. The report provides a practical TCO framework that integrates purchase price, uptime, spare-parts lead times, energy consumption, and service contract options—enabling procurement teams to go beyond sticker price.

Laminating Machine Market

Regulatory and sustainability risk management: Regulatory drivers are reshaping product specifications and capital selection. Our analysis links compliance timelines (food-safety, VOCs, energy efficiency) to machine retrofit windows and replacement triggers, equipping regulatory, EHS, and operations teams to align CAPEX with compliance curves.

M&A and partnership screening: Fragmentation characteristics and concentration metrics in the market create differentiated M&A opportunities across the value chain. The study’s competitive maps, technology due-diligence checklists, and synergy calculators support strategic and financial sponsors evaluating bolt-on acquisitions or manufacturing partnerships.

Market sizing and forecast model: A base-year market size calibrated to 2025, growth scenarios to 2032, and sensitivity runs to test demand shocks and policy shifts. (Note: the public synopsis highlights macro figures — detailed segment and regional breakdowns are reserved for subscribers.)

Demand-driver diagnostics: Application-level dynamics, adoption curves for solventless and solvent-based technologies, and the role of packaging trends in accelerating or constraining demand.

Supplier economics and margins: Manufacturer cost structures, aftermarket service economics, spare parts pricing, and profit pool mapping—critical for pricing and negotiation strategies.

Technology and innovation roadmap: Assessment of automation, web-handling precision, high-speed designs, UV curing integration, and digital features (IIoT, predictive maintenance). Each technology is scored by maturity, capital intensity, and typical payback period.

Regulatory and sustainability overlay: Impact analysis of VOC reduction mandates, food-safety requirements, energy-efficiency rules, and how these translate into machine specifications and operational changes.

Competitive profiling and strategic positioning: Detailed profiles of leading OEMs, channel footprint assessments, and a CR-based market-concentration analysis to guide partnership strategies.

Buyers’ playbook and procurement checklist: A step-by-step template to evaluate offers, run pilot installations, and structure performance-based service agreements.

M&A playbook and valuation guidance: Scenario-based valuation multiples, integration risk matrices, and a list of strategic acquisition targets by capability gap.

Primary research appendix: Executive interviews, plant-level site visits, and supplier surveys underpinning the quantitative model, plus methodology notes for replication and customization.

The laminating machine market is neither a pure commodity arena nor a closed oligopoly. Market concentration is meaningful: the three largest players collectively account for a substantial share of equipment sales, with the top five extending that influence further. This structure produces distinct competitive dynamics:

Modularity and short‑run flexibility as differentiation. Established European players emphasize high automation, modular platforms, and customization for converters targeting short runs and premium flexible packaging. These attributes map to higher average selling prices but also stronger aftermarket revenue and deeper integration into customers’ production planning.

Speed and scale from high-volume manufacturers. Several Asian OEMs compete on throughput, cost efficiency, and export reach—offering high-speed solventless lines and aggressive lead times. For buyers focused on unit-cost reduction and high-volume corridors, these suppliers present compelling TCO propositions.

Sustainability and low-emissions positioning. A clear trend among progressive suppliers is the migration to solventless adhesives and low-VOC systems, responding to both regulation and buyer preferences. Leaders investing early in energy-efficient and zero-VOC technologies are building durable barriers in regulated markets.

Aftermarket as a margin engine. Given the installed base and criticality of uptime, service, spare parts, and upgrade paths represent a substantial profit pool. OEMs that convert capital sales into long-term service relationships capture outsized lifetime value.

Representative vendor signals — distilled from product portfolios and recent market activity:

Bobst Group (Lausanne, Switzerland) — Driving high-automation, solventless modular systems for flexible packaging with an emphasis on customization and short-run economics.

Nordmeccanica (Italy) — Focused on process stability and advanced web handling for packaging converters through simplex and triplex solventless platforms.

Comexi Group Industries (Spain) — Positioning on high productivity and sustainable, zero-VOC laminating solutions targeted at large-scale flexible packaging lines.

SINSTAR (Chongqing, China) — Leveraging scale and high-speed capabilities to serve export markets, with an installed-unit base that underpins service and parts businesses.

Selected specialist OEMs — including manufacturers of fully automatic cardboard laminating systems, narrow-format converters, and precision industrial laminators — are occupying niche positions that matter for label, RFID, and specialty packaging applications.

Regulatory push toward solventless adhesives: Our sector analysis quantifies the emissions, compliance and retooling implications. Transitioning to solventless systems reduces VOC exposure materially and is becoming a procurement requirement in regulated supply chains—creating urgency for both converters and OEMs to prioritize compatible technology paths.

Food and beverage safety regulations: Increased demand for laminates that extend shelf life and satisfy hygiene protocols is reshaping specification checklists, particularly for contract packagers and private-label brands.

Energy-efficiency mandates in key markets: Energy-focused regulations in Europe and other regions are pushing buyers toward low-carbon footprint machines. Vendors that can demonstrate lifecycle energy savings and retrofit options will gain competitive advantage.

Volatility in raw material costs: Fluctuations in plastics, adhesives, and film prices continue to compress margins for converters and affect the economics of replacing lines versus optimizing existing assets.

Digitalization and IIoT: Predictive maintenance, remote service, and performance analytics are evolving from “nice-to-have” to differentiators in high-throughput operations where downtime is costly.

CapEx planning: Use scenario-based thresholds from our model to decide between phased upgrades and full-line replacements. Prioritize investments that shorten changeover time and lower energy per meter.

Procurement strategy: Leverage the TCO comparator and aftermarket scorecards in the report to reframe supplier negotiations around lifecycle costs and service SLAs rather than only capital price.

Product roadmap alignment: R&D and product teams should benchmark against the technology maturity matrix to set timelines for solventless integration, UV curing, and IIoT-enabled retrofits.

M&A screening: Apply the report’s strategic fit matrices to identify targets that close capability gaps in automation, sustainability, or geographic service presence.

This briefing intentionally surfaces the strategic signals and high‑level metrics executives need to begin planning for 2026. For practitioners requiring transaction-grade numbers, regional and application-level forecasts, and the full suite of segment tables, PW Consulting’s full Laminating Machine Market report provides the complete dataset, primary-source appendices, and executable deal and procurement playbooks. Access to that intelligence accelerates confident decisions—whether you are optimizing an existing manufacturing footprint, evaluating OEM partnerships, or sizing an acquisition target.

PW Consulting’s role is to translate market dynamics into operational choices. Our laminated methodology pairs rigorous top‑down modelling with ground-level interviews and plant audits, so clients can move from insight to investment with clarity and speed.

For detailed analysis of this topic, please visit the official page:Laminating Machine Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com