What Advances Are Improving Outcomes for Children with Growth Hormone Deficiency?

Networking |

2026-06-09 10:20:55

As PW Consulting’s Senior Strategic Advisor and Head Industry Analyst, I present a concise but high-fidelity preview of our newest Metal Composite Panel (MCP) Market study. This briefing is designed to demonstrate the analytical depth and practical utility of the full report while preserving the proprietary segment-level intelligence that drives real competitive advantage. Use this preview to judge fit: if your 2026 commercial, procurement, or investment decision depends on durable, regulation-ready, and scalable panel solutions, the full study is the working intelligence you need.

Metal Composite Panel Market

The MCP market is moving from steady growth to strategic inflection. Our base-year analysis (2025) establishes a total market value of USD 7.8 Billion and a projected trajectory that reaches roughly USD 11.16 Billion by 2032, reflecting a compound annual growth rate (CAGR) of 5.2% across the forecast horizon. That cadence of expansion—modest but persistent—creates distinct windows for value capture across product innovation, regional manufacturing footprint, and regulatory-compliant product differentiation. Companies that can align R&D, supply chain resilience, and go-to-market timing in 2026 will lock in outsized returns over the next five years.

Metal Composite Panel Market

Growth drivers: ongoing urbanization, retrofit demand in mature markets, rising specification of fire-retardant and insulated variants, and sustainability-driven preference for recyclable composites.

Metal Composite Panel Market

Market structure: moderate concentration at the top end—our concentration metrics indicate leading groups control a meaningful share but leave room for nimble regional players and specialized techno-product entrants.

Cost pressure & input volatility: upstream commodity movement—especially alumina and bauxite—has driven cost increases into 2025, elevating raw-material risk premia for manufacturers and buyers alike.

The full report examines incumbent leaders and high-impact challengers across manufacturing capability, product portfolio, certification status, and go-to-market coverage. Representative profiles included in the study:

3A Composites (Switzerland) — a global product innovator focusing on premium ALUCOBOND® PLUS and ALUCOLUX lines, increasingly emphasizing fire-retardant cores and pre-painted custom-length offerings.

Alubond USA (United States) — positions itself on non-combustible, recyclable core solutions for high-visibility facade and canopy projects.

Alpolic (Japan) — expanding regional manufacturing to improve supply reliability while increasing recycled-content content in façade-grade panels.

Alcoa (United States) — pushing insulated ACM variants and running field trials in high-growth markets to validate retrofit and energy-efficiency claims.

Eurobond Industries and Viva Composite Panel (India) — regional scale players advancing capacity and fire-class performance, with Viva’s investment in a high-mineral-content A2 core plant as a market-significant development.

Mitsubishi Chemical (Japan) — leveraging polymer chemistry and sustainability positioning through its Mitsubishi Plastic channels.

Each company analysis in the report includes manufacturing map overlays, product-portfolio heatmaps, commercial strengths & weaknesses, channel strategies, and an investment/de-risking scorecard that highlights where M&A, JV, or greenfield playbooks are viable in 2026.

Escalating code and certification expectations: recent NFPA 285 approvals for certain composite stacks have shifted acceptable specification sets in major metro jurisdictions, effectively raising the bar for facade system acceptance.

EN 13501-1 and A2 performance: the commissioning of mineral-rich A2 core production facilities in 2025 demonstrates how manufacturers are closing technical gaps between regulatory demands and market-preferred aluminum composite formats.

Regional code convergence: as large municipalities update fire-safety and sustainability codes, procurement teams must layer certification risk into supplier selection criteria—our report models several realistic paths for acceptance timelines and claims validation.

Input-cost movements are central to 2026 planning. Our study integrates primary pricing intelligence—e.g., 2025 upward movement in imported bauxite and metallurgical-grade alumina—to quantify margin exposure across product families and to simulate supplier pass-through behavior under different contract terms. We model scenarios that show how a 5–10% movement in alumina pricing affects panel cost stacks, typical OEM margins, and bid competitiveness in competitive tenders.

Capacity & certification investments: the commissioning of A2 fire-retardant core capacity (May 2025) reshapes the product availability curve for Class A2-compliant panels, compressing lead times for certified offerings in some regions.

Product rebranding & portfolio rationalization: 2025 rebrand and expansion moves by major producers signal an industry pivot toward higher-margin, specification-driven SKUs (e.g., recyclable and pre-finished lengths).

Field validation & product trials: on-the-ground trials of insulated panel variants indicate manufacturers are preparing to capture retrofit and energy-performance projects—this matters for developers and contractors choosing preferred suppliers in 2026.

Our study is structured to convert market intelligence into executable action plans. Key deliverables:

Market sizing and forecast model (base year 2025; forecast 2026–2032) with customizable scenario toggles for commodity prices, regulatory adoption rates, and construction activity indices.

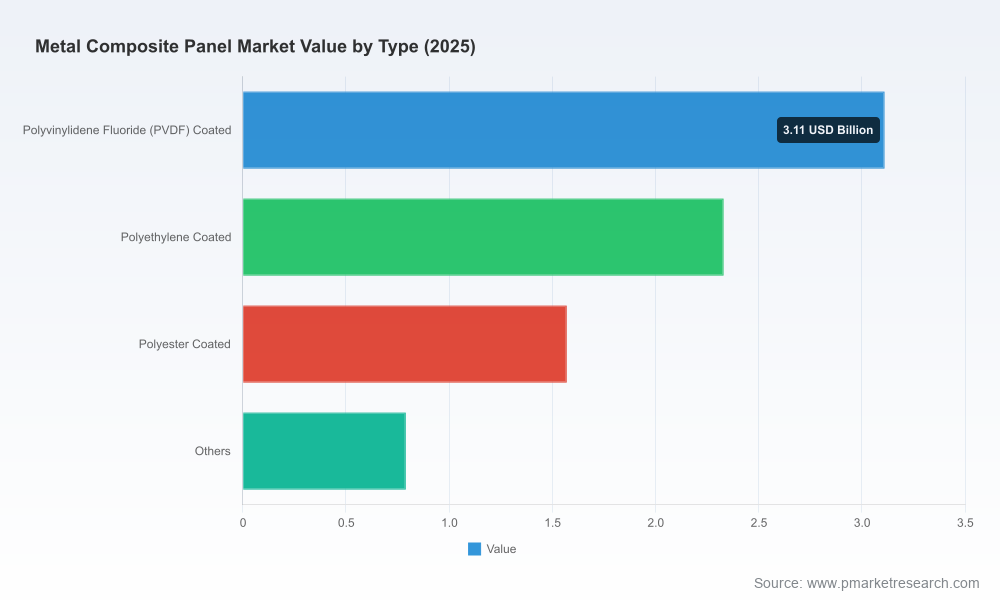

Granular segmentation (coating types, core technologies, applications, regional demand drivers) — note: these granular splits are part of the proprietary appendices available in the full report.

Competitive intelligence dossiers covering product portfolios, manufacturing footprints, certification status, and go-to-market strength—scored and benchmarked for rapid comparative analysis.

Supply-chain risk matrix and hedging playbook: practical contracting levers, buffer-capacity playbooks, and inventory sizing recommendations to protect gross margin.

Regulatory impact matrices: jurisdiction-by-jurisdiction adoption likelihood for elevated fire-safety codes, plus compliance pathways for A2 and NFPA-class systems.

Commercial playbooks for 2026: tender-win pricing templates, specification-change management workflows, and retrofit-market entry sequencing.

M&A & partnership target list and valuation heuristics tuned to vertical integration, core-competency acquisition, and regional footprint expansion.

Primary interview transcripts & supplier checklists—actionable questions procurement teams should ask OEMs and raw-material refiners in 2026.

Procurement: layer certification risk and alumina-price sensitivity into long-term purchase agreements; our model shows how different contract types (fixed-price, price-indexed, or hybrid) affect landed-cost volatility.

Product strategy: prioritize development of fire-class and insulated offerings where code momentum and retrofit opportunity align—timing matters given certification lead-times.

CapEx prioritization: use our manufacturing footprint analysis to decide whether to partner for local production, expand existing lines, or secure off-take agreements with certified suppliers.

M&A and JV decisions: target mid-sized regional producers that bring certificate-ready capacity or mineral-core technology to accelerate market entry without protracted R&D cycles.

Commercial bidding: deploy our tender templates and competitive scorecards to quantify trade-offs between price, certification, and delivery lead time—crucial for win-rate optimization in 2026 tenders.

To protect the commercial value of the full analysis, this preview omits the detailed segmentation matrices, exact regional and application-level revenue shares, and the granular pricing curves that inform supplier-specific margin stress tests. Clients who require those inputs—deliverable in an exportable model and a confidential appendix—will find them in the full PW Consulting report and in the accompanying Excel tool.

If your 2026 plans include re-specifying facade partners, launching an insulated-panel line, negotiating long-term alumina-linked contracts, or evaluating acquisition targets, the full report provides the playbooks, models, and supplier intelligence to act with conviction. Contact PW Consulting to gain access to the complete report, the forecast model, and the confidential competitive dossiers that translate market signals into executable 90–180 day plans.

In a market expanding from USD 7.8 Billion in 2025 toward a projected USD 11.16 Billion by 2032 at a 5.2% CAGR, the difference between a good decision and a strategically timed one can be millions of dollars in realized value. The full study is designed to make that difference tangible—and actionable—for your 2026 agenda.

For detailed analysis of this topic, please visit the official page:Metal Composite Panel Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com