Effervescent Tablet market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-11 09:12:28

As retailers, hardware vendors, systems integrators and private equity sponsors prepare plans for 2026, the Retail Touch Screen Display market presents a blend of accelerated demand and fragmentation that rewards decisive strategy. PW Consulting’s latest market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes primary interviews, device-level observations and vendor intelligence to translate technical evolution into actionable commercial options. At the top line, the market has expanded sharply through the last five years and is forecast to continue growing at a compound annual growth rate (CAGR) of 11.7% over our forecast window, more than doubling from the mid‑2020s to the late 2030s under our base scenario. This preview explains why that trajectory matters to 2026 planning and what senior executives should prioritize before committing capital, pilots or partnerships.

Retail Touch Screen Display Market

Timing and scale: The market’s acceleration through 2023–2025 crystallized several inflection points—wider acceptance of self‑service, integration of payments at the edge, and rising adoption of interactive merchandising. For 2026, those inflection points become investment decision nodes: whether to accelerate rollouts, consolidate supplier lists, or defer to next‑generation platforms that integrate compute and analytics at the display level.

Retail Touch Screen Display Market

Commercialization of software: Touch displays are no longer passive hardware; software platforms and content orchestration determine long‑term returns. The winners will be vendors and integrators that combine durable hardware with cloud‑native device management, modular payments and attention‑economy retail media capabilities.

Retail Touch Screen Display Market

Consolidation and partner economics: Despite strong growth, market concentration remains low—our CR3 and CR5 measures show an industry where bespoke innovators coexist with larger systems vendors. That structure creates acquisition and alliance opportunities in 2026 for organizations seeking rapid capability expansion without building in‑house expertise.

Risk and compliance: Security, payment certifications, and software maintenance cycles are now mission‑critical. Maintenance releases and lifecycle policies materially affect TCO and upgrade cadences; procurement teams that evaluate firmware roadmaps alongside hardware specs reduce surprise costs.

We designed the report as a decision tool for commercial leaders, not merely an academic exercise. Highlights include:

The vendor landscape is a mix of established hardware specialists, vertical OEMs and software‑first entrants. Recent, material developments sharpen strategic implications for 2026:

Elo Touch Solutions (Milpitas, CA): A long‑standing leader in retail and POS touch displays, Elo expanded its integrated payments portfolio in early 2025 and subsequently became part of a larger automation and frontline‑technology player through an acquisition announced in late 2025. That integration accelerates route‑to‑market access for end‑to‑end retail solutions and raises the strategic bar for rivals that remain hardware‑only.

Teguar (Charlotte, NC): A specialist in rugged industrial displays and panel PCs, Teguar continued to position itself for regulated or harsh environments with new medical and industrial products in late 2024 and ongoing customization options. For accounts prioritizing durability and lifecycle support, Teguar remains an attractive integrator partner.

eyefactive GmbH (Hamburg): A software‑and‑hardware innovator in interactive multi‑touch installations, eyefactive reinforced its position with product updates and industry awards through 2025. Its focus on curated multi‑touch experiences highlights the commercial opportunity in experiential retail and omni‑channel merchandising.

Collectively, these developments illustrate two concurrent forces: acceleration toward integrated systems that bundle payments, edge analytics and device management; and continued specialty innovation from smaller players focusing on niches such as medical, ruggedized or immersive multi‑touch experiences. The combined effect is a market offering both scale economies and niche upward pricing pressure—hence the strategic importance of a differentiated go‑to‑market in 2026.

Edge and compute integration: Displays increasingly embed compute for local analytics, payment processing and vision-based services. Procurement teams must budget for compute refreshes as part of hardware lifecycles.

Software ecosystems and retail media: The commercial value of a display is measured by the revenue it enables—retail media, targeted promotions and loyalty integration are now central to ROI modeling.

Touch modality and UX: While capacitive multi‑touch remains foundational, shops and kiosks are experimenting with form factors (curved walls, multi‑touch tables) that require software customization and longer deployment timelines.

Lifecycle governance: Firmware maintenance, payment certification cycles and platform updates (for example, periodic Android maintenance releases) directly impact device uptime and upgrade costs; teams should insist on public maintenance roadmaps in RFPs.

Supply chain and sourcing: Even in a growing market, component shortages and logistics volatility require diversified sourcing strategies and options for managed inventory or consignment arrangements.

Reconcile strategy with vendor capabilities: Use our vendor diagnostics to map current suppliers to capability gaps (payments, edge analytics, maintenance). Prioritize one pilot to test integrated payment + analytics stacks and one to validate experiential formats (multi‑touch or curved videowalls).

Lock down lifecycle economics: Require total cost of ownership proposals in upcoming RFQs that include firmware/OS maintenance, payment recertification and field swap SLAs. Run our TCO template to compare proposals on a like‑for‑like basis.

Scan for partnership or acquisition opportunities: Given the industry’s low concentration, strategic buyers can secure capability quickly through partnerships or tuck‑ins. Use our shortlists to prioritize targets by strategic fit, not just price.

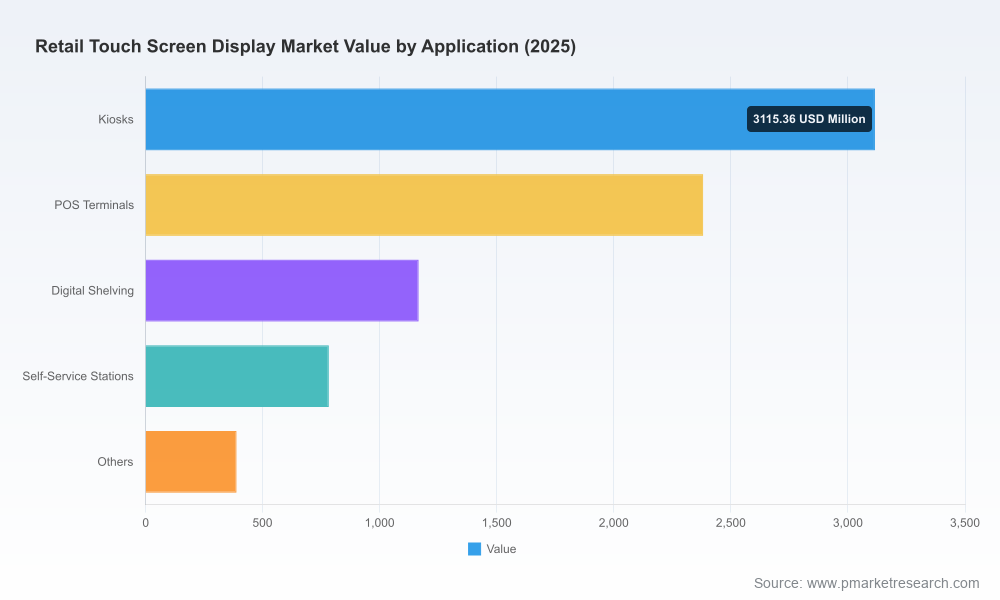

To preserve the strategic value of our primary, granular work and to encourage rigorous procurement discipline, this preview omits detailed regional and application splits, granular unit shipment forecasts by touch modality, and vendor revenue breakdowns. Those datasets, plus downloadable financial models and customizable scorecards, are available in the full PW Consulting Retail Touch Screen Display Market report and accompanying data pack.

For 2026, the key decisions are not whether touch displays will matter—market momentum makes that clear—but how you organize resources, partners and pilots to capture the asymmetric upside. PW Consulting’s study converts device‑level trends into commercial roadmaps: vendor selection frameworks, procurement templates and scenario models that translate growth forecasts into prioritized investments. If your 2026 plan includes rollouts, M&A, or a rethink of your in‑store technology stack, the full report provides the datasets and operational playbooks to move from hypothesis to execution with confidence.

To access the complete analysis, including the segmented datasets, vendor scorecards and executable templates, consult the PW Consulting Retail Touch Screen Display Market report and request a briefing to align its findings with your 2026 agenda.

For detailed analysis of this topic, please visit the official page:Retail Touch Screen Display Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com