Building Materials Market 2026: Strategic Outlook for Decision‑Makers

As organizations finalize 2026 strategies, the building materials sector presents a paradox: large absolute scale and steady medium‑term growth, yet pronounced fragmentation and intensifying regulatory and input‑cost pressures. This preview of PW Consulting’s Building Materials Market research synthesizes the essential market trajectory, competitive posture, regulatory tailwinds and headwinds, and the concrete uses executives should make of the full study. It is designed to equip boards, corporate strategy teams, investors, and procurement leaders with the analytical lens required to prioritize action — while directing readers to our full report for the granular segment and scenario data that underpin these recommendations.

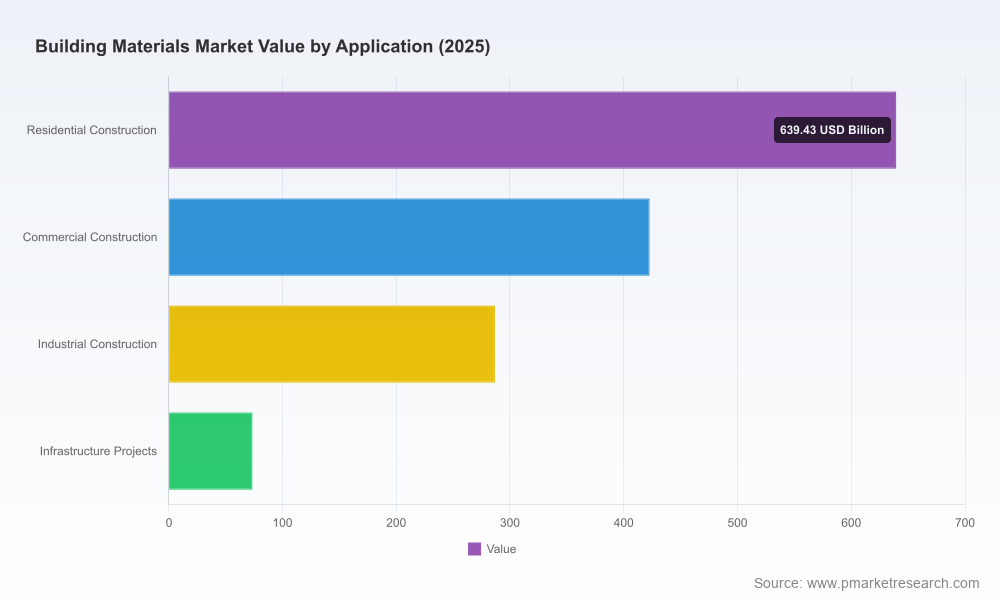

Building Materials Market

Market trajectory and what the numbers mean for 2026

Measured on a global revenue basis (USD, base year 2025), the building materials market expanded materially through the 2020–2025 period, increasing from roughly USD 1.10 trillion in 2020 to about USD 1.42 trillion in 2025 — a near‑30% rise over five years. After a stabilization around the 2024–2025 horizon, our forecast environment anticipates a return to steady expansion through the 2026–2032 window. The market is projected to grow at a compound annual growth rate (CAGR) of 4.1% during the forecast period, reaching approximately USD 1.88 trillion by 2032.

Building Materials Market

Why these topline dynamics matter in practical terms for 2026 planning:

Building Materials Market

- Scale creates options: With a multitrillion‑dollar market, even small shifts in share or margin translate to material P&L and cash‑flow outcomes for mid‑cap and large players.

- Stability with upside: The modest CAGR implies predictable demand baselines, enabling staged capital deployment rather than all‑in capacity bets — provided companies hedge near‑term input volatility.

- Fragmentation influences strategy: Market concentration remains low (CR3 ≈ 24%, CR5 ≈ 26%), signaling opportunities for bolt‑on consolidation, regional roll‑ups and differentiated product plays rather than winner‑take‑all national monopolies.

Five dynamics reshaping competition and investment through 2026

- Input cost volatility and trade policy. Expanded US tariffs on steel and aluminum and new global tariff measures have increased pass‑through risks for materials that rely on metal or imported feedstocks. Procurement strategies that previously relied on open cross‑border sourcing now require robust scenario planning and supplier diversification.

- Decarbonization as a capital allocation axis. Leading producers are shifting capex and M&A into low‑carbon cement, circular aggregates and product solutions that credibly reduce lifecycle emissions. These moves are not purely ESG signaling — they reshape cost curves and future regulatory compliance costs.

- Regulatory compliance and permitting pressure. Enhanced greenhouse‑gas permitting requirements for cement and specialty plants mean longer lead times for new capacity and higher ongoing compliance costs. Companies must bake permitting risk into plant economics and acquisition valuations.

- Infrastructure and housing demand duality. Public infrastructure programs and ongoing residential activity underpin base demand; however, the composition of growth (e.g., retrofit vs new build, multifamily mix, public works cadence) will determine winning product portfolios.

- Fragmentation enabling tactical M&A and niche specialization. Low aggregated concentration leaves room for regional champions, vertical integration (from aggregates to ready‑mix), and digital or sustainability‑led product differentiation to capture outsized margins.

Competitive landscape: how incumbents are repositioning

The market is being actively shaped by a set of global and regional leaders whose strategic levers vary but whose common focus areas are sustainability, supply resilience and selective growth. Our full report includes a detailed competitive heatmap and strategic scorecards; below is a high‑level synthesis.

- CRH plc — With broad upstream and downstream exposure, CRH is leveraging scale to invest in low‑carbon products and operational efficiencies. Recent quarterly results underscore resilient demand in core markets and continued emphasis on sustainability and margin improvement.

- Holcim Ltd — Holcim’s acquisition activity and integrated sustainability agenda position it as a product‑innovation leader in low‑carbon cement and circular aggregates. The firm’s 2025 integrated reporting highlights deliberate moves to capture the decarbonization premium through both organic R&D and strategic M&A.

- CEMEX — CEMEX’s reputation and governance focus are increasingly strategic assets. Recognition for ethical practices complements its push into urbanization solutions and differentiated service offerings across key markets.

- Vulcan Materials & Martin Marietta — As North American heavy materials suppliers, these companies are emphasizing reserve management, operational discipline and selective vertical integration into downstream concrete and asphalt solutions. Their public filings and earnings releases provide important signals on future investment and pricing behavior in aggregates markets.

- Heidelberg Materials — A classical industrial incumbent with a global footprint, its strategic playbook centers on integrated production efficiency and product portfolio optimization in high‑margin building systems.

Collectively, these players demonstrate two strategic patterns: (1) incumbents are monetizing sustainability investments through new product lines and premium pricing where buyers accept lifecycle valuations, and (2) regional specialization and logistics control remain critical sources of defensibility, especially in materials with high transport intensity.

What PW Consulting’s full report delivers (practical, operational outputs)

Our research is structured to be directly actionable for corporate and investment decision‑makers. Key deliverables include:

- Base and alternative forecast models (2026–2032) with scenario toggles for macro growth, tariff regimes, and carbon‑cost pathways.

- Detailed supply‑chain maps and logistics cost sensitivity analyses to quantify the break‑even distance for centralized vs localized production strategies.

- Regulatory risk matrix and permitting lead‑time playbook tailored to cement, specialty plants, and aggregates operations.

- Competitive benchmarking dashboards, including capex schedules, ESG investment profiles, and likely M&A targets by strategic intent.

- Commercial playbooks for procurement, pricing, and product mix optimization that translate demand signals into gross margin targets and SKU rationalization guidance.

- Value‑creation templates for post‑merger integration, asset monetization, and carbon investment ROI modeling.

Note: In keeping with our “trailer” approach, the report’s granular regional, application and product splits — the line‑by‑line datasets that power valuation and go‑to‑market decisions — are available exclusively in the full report and subscriber data portal.

How to use this research in 2026 planning cycles — nine immediate actions

- Embed the 4.1% mid‑term CAGR and base‑case forecasts into capital budgeting to avoid overcommitment in cyclical commodities while preserving optionality for decarbonization investments.

- Restart supplier qualification and dual‑sourcing pilots focused on non‑metal inputs and regional aggregates to mitigate tariff and transport shocks.

- Re‑score acquisition targets using our regulatory lead‑time matrix; prioritize assets with decarbonization pathways and short permitting horizons.

- Reprice product portfolios where lifecycle value can be demonstrated — secure pilot customers for low‑carbon cement and circular aggregate solutions to validate premium acceptance.

- Accelerate digitalization in downstream logistics and inventory forecasting to minimize working capital and optimize fill rates amid variable demand pockets.

- Stress‑test plant economics against higher carbon‑cost scenarios and potential new permitting constraints; identify early retirements and repurposing candidates.

- Deploy scenario planning for trade‑policy shocks and include tariff impacts in tender pricing and long‑term contracts.

- Prioritize internal ESG reporting and external communications to capture reputational value, given investors’ rising attention to credible decarbonization roadmaps.

- Use the report’s M&A playbooks to sequence deals that build regional scale in logistics corridors rather than chasing national headline targets alone.

Conclusion — the strategic value of a data‑led, scenario‑based approach

The building materials market in 2026 is large, stable in the near term, and fertile for strategic moves that combine operational resilience with sustainability‑led differentiation. Our topline numbers — a market size of roughly USD 1.42 trillion in the 2025 base year and a 4.1% CAGR through 2032 — frame a landscape where smart capital allocation and focused execution will separate winners from laggards. At the same time, low concentration and regional complexity mean there is no one playbook: success will be defined by rigorous, locality‑specific analysis backed by scenario modeling, regulatory foresight, and disciplined integration capabilities.

For executives preparing 2026 budgets, M&A roadmaps, or investor communications, the full PW Consulting Building Materials Market report supplies the detailed segmentations, financial models, and tactical playbooks required to translate these strategic imperatives into measurable value. Access the complete analysis, datasets, and interactive tools through our subscriber portal to convert insight into advantage.

For detailed analysis of this topic, please visit the official page:Building Materials Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com