Thermoplastic Vulcanizates (TPV) Market — Strategic Preview for 2026 Decision‑Makers

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a focused industry primer designed to orient executives, product leaders, and investors preparing strategic moves in 2026. This preview synthesizes macro growth dynamics, competitive posture, regulatory headwinds and tailwinds, and the pragmatic levers organizations must control to convert a growing market into sustainable advantage. It intentionally showcases our analytical depth while withholding the full segment-level tables and granular numbers to incentivize direct access to the complete report for transaction‑critical details.

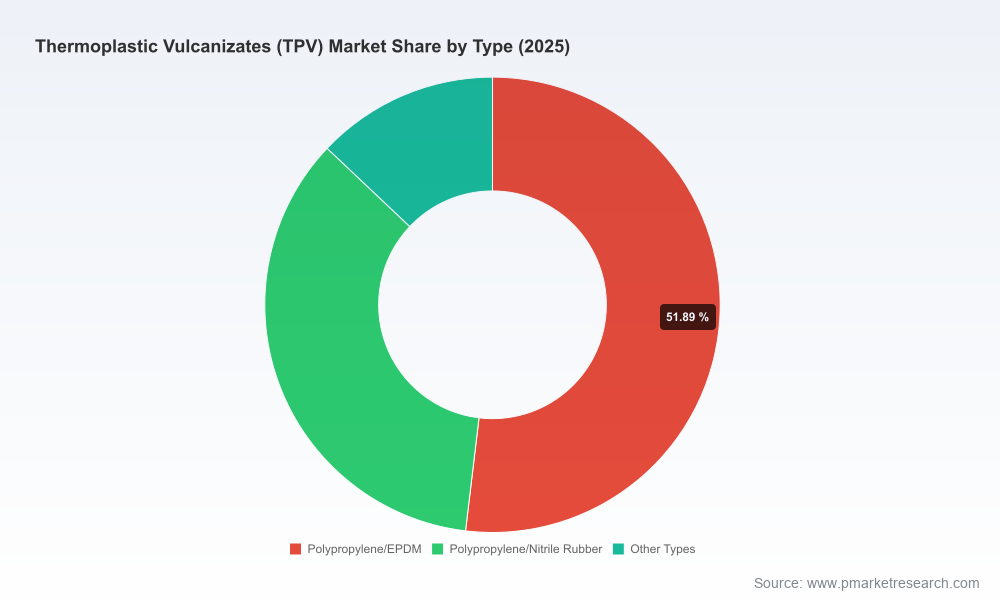

Thermoplastic Vulcanizates (TPV) Market

Why TPV matters now — a concise market snapshot

Thermoplastic Vulcanizates (TPV) sit at the intersection of elastomer performance and thermoplastic processing economics. From 2020 through our base year of 2025, the TPV market has shown steady expansion — rising from mid‑three‑digit figures in USD Million to approximately USD 210.5 Million in 2025 — reflecting resilient demand across automotive, industrial, medical and consumer channels. Our forecast through 2032 anticipates continued momentum with a compound annual growth rate (CAGR) of 7.9% across the 2026–2032 horizon, culminating in a market approaching USD 342.1 Million by 2032.

Thermoplastic Vulcanizates (TPV) Market

Two implications follow for 2026 planning: first, aggregate growth validates resource allocation for product development, capacity and go‑to‑market expansion; second, the growth profile is sufficiently concentrated in specific use‑cases that bespoke strategy (not broad, undirected investment) will deliver disproportionate returns. PW Consulting’s full report maps these inflection points and identifies the pockets of faster-than-average adoption — information we reserve for the full deliverable.

Thermoplastic Vulcanizates (TPV) Market

What this research delivers — practical, transaction‑ready intelligence

- Actionable market sizing and trend trajectories: base year (2025), historical series (2020–2025), and detailed forecast (2026–2032) denominated in USD Million, enabling precise ROI modeling for capacity and R&D investments.

- Demand‑side segmentation intelligence: supply chain exposure, application adoption curves (automotive, construction, medical, consumer and industrial), and material‑type dynamics to shape product roadmaps and commercial prioritization.

- Supply‑side diagnostics: feedstock dependency mapping, manufacturing footprint analysis, and cost sensitivity scenarios anchored to polypropylene and EPDM price vectors.

- Competitive playbooks: capability matrices for global incumbents, assessment of brand and technology moats, and go‑to‑market tactics that win in regulated and specification‑tight environments.

- Regulatory and sustainability checklists: practical compliance routes (including biocompatibility and food‑grade pathways), circular design considerations, and procurement levers for recycled content adoption.

- M&A and partnership templates: diligence red flags, integration playbooks for compounding elastomer portfolios, and frameworks for bolt‑on versus greenfield strategies.

Dynamics shaping 2026 decision frameworks

- Feedstock volatility and cost pass‑through: TPV production costs remain tightly coupled to polypropylene resin and EPDM rubber markets. Price swings in crude and natural gas propagate through to EPDM, while PP pricing governs much of compounding economics. Organizations must stress‑test commercial contracts and consider hedging, strategic offtakes, or vertical integration scenarios to protect margins.

- Regulatory directionality: Recent regulatory moves — most notably those mandating recyclable content in vehicles and stricter end‑of‑life requirements — create both compliance liabilities and product opportunities. TPV manufacturers who can demonstrate recyclability, circular content, or ease of disassembly will gain preferential access to OEM supply chains.

- Technical compliance and market access: Select TPV grades already meet ISO 10993‑5 biocompatibility and food‑grade standards, opening growth vectors in medical and food‑contact applications. These certifications are not trivial: they require controlled manufacturing, comprehensive documentation, and long lead times. Early commitment will accelerate certification-driven wins.

- Sustainability as a source of differentiation: The emergence of TPV grades incorporating recycled content or enabling lower life‑cycle footprints is shifting procurement criteria. Sustainability initiatives are no longer marketing add‑ons; they are procurement filters — as evidenced by product launches and public commitments from leading suppliers.

Competitive landscape — how incumbents are shaping the market

The TPV market exhibits moderate concentration: the top three and top five players combine to form meaningful, but not monopolistic, pools of influence. The market concentration profile suggests a fragmented but technologically sophisticated landscape where global brand names coexist with regional compounders and specialized TPE/TPV formulators. Below are high‑level strategic profiles of principal competitors addressed in our study:

- Teknor Apex Company (Pawtucket, RI, USA) — Known for Sarlink TPV grades and a truly global production footprint, Teknor Apex has invested in consistent quality and supply dispersion. Recent product activity targeted sustainability: a 2025 launch of wire & cable compounds with up to 50% recycled content is emblematic of a broader strategy to pair performance with circularity.

- Celanese Corporation (Irving, TX, USA) — Through ownership of the Santoprene trademark and a broad engineered materials portfolio, Celanese operates at scale with deep OEM relationships. Price adjustments announced in 2025 highlight how supply and feedstock economics translate into commercial action; buyers should expect periodic repricing cycles tied to underlying resin markets.

- KRAIBURG TPE GmbH & Co. KG (Amberg, Germany) — KRAIBURG competes on product breadth and technical customization, offering named series aimed at automotive, consumer and medical sectors. Their visibility at major trade shows reaffirms a market posture focused on specification leadership and localized customer engineering support.

- LyondellBasell Industries N.V. (Rotterdam, Netherlands) — LyondellBasell leverages polypropylene technology and cost‑competitive manufacturing to offer TPO and TPV compounds. Their strength lies in large‑scale processing know‑how and the ability to optimize cost structures for volume applications.

- ExxonMobil Chemical Company (Houston, TX, USA) — With access to high‑performance elastomer science and trademarked TPV offerings, ExxonMobil remains a supplier of choice for high‑specification applications in automotive, medical and infrastructure markets.

Strategic takeaways for 2026: incumbent moves fall into three playbooks — brand‑scale incumbency (large integrated players), specification leadership (technical TPE/TPV innovators), and value optimization (cost‑focused compound producers). Effective challengers will combine two playbooks: innovation in sustainable formulations plus scale‑efficient manufacturing partnerships.

Recent commercial signals and their strategic implications

- Teknor Apex’s Jan 2025 launch of recycled‑content wire & cable compounds signals that early adopters of circular TPV formulations can outposition competitors for applications where recycled content is now a procurement checkpoint.

- Celanese’s May 2025 price increases demonstrate how quickly feedstock pressures can be transmission mechanisms to OEMs and downstream suppliers; contract design and indexation clauses will be negotiation focal points in 2026.

- KRAIBURG’s participation at CHINAPLAS 2026 underscores the continuing importance of high‑touch engagement in Asia Pacific as a market expansion strategy. Local certification, localized blends and speed to approval matter more than aggregate product portfolios.

Where to focus investment and capability building in 2026

- Product portfolio rationalization: Prioritize TPV grades that answer the twin tests of regulatory compliance (e.g., recyclability or biocompatibility) and unit economics. Abandon or de‑emphasize low‑margin, specification‑commodity SKUs unless they tie to strategic customers.

- Supply chain resilience: Secure diversified feedstock sources, negotiate multi‑year supply agreements with indexation that limits volatility exposure, and evaluate tolling or JV models to mitigate capex risk while expanding capacity.

- Certification pipeline acceleration: Fast‑track medical and food‑contact approvals for qualified grades; the payoff is premium pricing and extended product life cycles in regulated segments.

- Sustainability go‑to‑market: Embed recycled content and closed‑loop use cases into commercial propositions. Certification and verified life‑cycle assessments materially reduce buyer friction in automotive and institutional procurement.

- M&A and partnerships: Target bolt‑on acquisitions that add specialty grades, regional footprint, or certification capabilities — not merely volumetric scale. Partnerships with compounders in target geographies can accelerate access without heavy capex.

How PW Consulting helps — the next step

For 2026, the right play combines disciplined financial modeling, pragmatic supply‑chain moves, and a clear product commercialization map tied to regulatory and sustainability milestones. PW Consulting’s full TPV Market report contains the granular segmentation, regional dynamics, product‑type matrices, and pricing scenarios required for transaction execution and contract negotiation. It also includes dashboards and downloadable datasets (USD Million denominated) that allow modelers to run bespoke sensitivity analyses for feedstock shocks, price escalations, and accelerated adoption scenarios.

This preview is intentionally selective: it demonstrates our analytical capabilities and the strategic pathways that will matter in 2026, while preserving the full segmentation tables and tactical recommendations as gated, high‑value deliverables. For executives preparing investment memoranda, supplier scorecards, or R&D roadmaps, the complete report is designed to be immediately actionable.

Concluding guidance

TPV presents a compelling growth story over the next decade with identifiable levers for superior returns. In 2026, success will not be defined by chasing broad market growth but by executing targeted plays: securing feedstock resilience, certifying and commercializing sustainably differentiated grades, and aligning with OEM and regulatory timelines. Organizations that move deliberately on these fronts can convert the market’s 7.9% projected CAGR into above‑market profit growth.

To access the full dataset, company scorecards, and executable recommendations tailored to your strategic objectives, contact PW Consulting for the complete Thermoplastic Vulcanizates (TPV) Market report and advisory engagement options.

For detailed analysis of this topic, please visit the official page:Thermoplastic Vulcanizates (TPV) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com