Ceramic Ball Valve Market — Strategic Outlook for 2026 Decision-Making

As PW Consulting’s Senior Strategy Advisor and Chief Industry Analyst, I present a targeted executive introduction to our full Ceramic Ball Valve Market study. This briefing is written as a strategic “preview trailer”: it surfaces the analytical depth and decision-ready insights that underpin the full report, while intentionally withholding the granular segment tables and proprietary split data that corporate leaders and transaction teams rely upon. For 2026 planning cycles, this piece explains why the ceramic ball valve market matters, how it is likely to evolve, and which strategic moves will preserve and create value in the near-term.

Ceramic Ball Valve Market

Market Snapshot: The Big Picture (Base Year 2025 — Forecast to 2032)

Using 2025 as the base year, our modelling shows the ceramic ball valve market has moved from a small but steadily expanding niche into a mid-sized industrial market with durable, above-inflation growth. The market rose from USD 81.5 Million in 2020 to USD 102.2 Million in 2025, reflecting a combination of recovery dynamics and secular demand in severe-service applications. Looking ahead across the 2026–2032 forecast window, we project a compound annual growth rate (CAGR) of approximately 4.2%, producing a market near USD 135.7 Million by 2032. The 2026 near-term estimate is aligned with continued moderate growth as capital cycles in energy, chemicals, and power sectors normalize.

Ceramic Ball Valve Market

What these headline numbers communicate to executives: this is not a hypergrowth sector, but it is a resilient, technical market with attractive margins for differentiated players and predictable replacement and aftermarket revenue streams. The scale and growth profile support focused investment, targeted capacity expansions, and M&A plays—so long as strategy accounts for concentrated technical barriers and supply-side volatility.

Ceramic Ball Valve Market

Why 2026 Is a Strategic Inflection Point

- Capital allocation decisions: With mid-single-digit CAGR and steady aftermarket demand, 2026 is the year to decide between incremental capacity investments and capability-led M&A (e.g., ceramic processing, certification capability, or regional production sites).

- Supply-chain re-engineering: Raw material and logistics risks that crystallized in 2024–25 make 2026 the window to implement hedging, supplier diversification, and selective nearshoring.

- Commercial positioning: Competition is being driven by technical differentiation (material science, full-ceramic designs, or ceramic-lined composites). The commercial winners will be those that pair superior product reliability with services—installation, predictive maintenance, and certified aftermarket parts.

Key Dynamics Shaping 2026 Strategy

- Raw material dependency: High-end ceramic valve manufacture relies on critical ceramic feedstocks. Industry data shows significant import dependency for alumina inputs and elevated external dependency for aluminum ore—this exposes producers to price and availability swings. Procurement teams must adopt multi-year sourcing contracts, backward integration feasibility studies, and strategic inventory buffers.

- Trade and regulatory shocks: Recent tariff actions introduced in 2025 have increased trade-cost volatility for many suppliers. For companies selling across borders, pricing models and contract terms must be re-run under several tariff/timing scenarios to preserve margins.

- Geopolitical shipping risk: Disruptions in strategic sea lanes have already translated into measurable export revenue impacts in certain flows. Logistics risk assessments—covering rerouting, freight cost sensitivity, and expedited manufacturing alternatives—should be piloted in 2026.

- Compliance cost burdens: Certification requirements (CE, API and equivalents) materially raise unit production costs. For new product introductions and export strategies, the incremental cost of certification must be factored into NPV analyses and pricing strategies; conversely, certification can be a defensible pricing lever in tendered procurement.

- Technology and materials: Advances in zirconia-based ceramics and full-ceramic ball construction are shifting the performance frontier for purity, abrasion, and corrosion resistance. Product roadmaps must prioritize material R&D or strategic partnerships with material specialists to maintain premium positioning.

Segment & Product Considerations (High-Level, Non-Disclosed Splits)

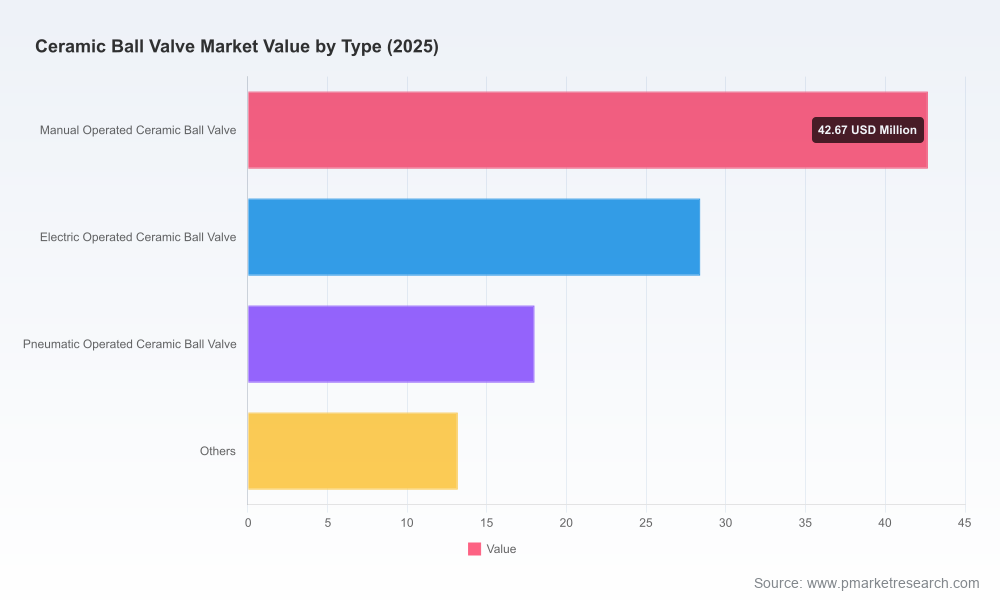

Our full study analyzes demand across regions, operation types (manual, electric, pneumatic, and others), and primary end-use sectors. We do not reproduce the split tables here, but key directional findings you should treat as planning inputs:

- Ceramic valve demand is driven both by new projects in heavy industry and by replacement/upgrade cycles in severe-service applications—creating a stable base demand and episodic upsides linked to commodity cycles.

- Electrification of actuation and integration with process control systems is a growing product trend that shifts value from pure hardware to systems capability—favoring companies with control-system partnerships or actuator expertise.

- Aftermarket and service revenue is disproportionately valuable: valves that reduce downtime and lower total cost of ownership command price premia and higher lifetime revenue per installation.

Competitive Landscape — Who Matters and Why

The market is characterized by a mix of specialized niche players and larger industrial valve groups. Market concentration metrics indicate pockets of consolidation at the top but substantial room for regional and technical specialists to compete: the top-three players account for roughly 30% of market value, while the top-five reach approximately 35%—a structure that rewards differentiation, regional agility, and aftermarket networks.

- Fujikin (Japan) — Known for fine-ceramic HiLife series using cerium-stabilised zirconia, Fujikin’s strength is ultra-high purity and abrasion resistance for semiconductor- and chemical-grade applications. Their R&D-led positioning is a defense against price competition.

- METSO (Finland) — Leverages systems integration into broader process control offerings. METSO’s advantage lies in selling valves as part of larger process solutions to mining and mineral processing customers.

- Velan Inc (Canada) — A credible global player moving into regional manufacturing footprints; recent plant activity in the Gulf demonstrates a strategy of proximity to large industrial investments and regional content optimization.

- GEFA Processtechnik (Germany) — Product integration (e.g., full-ceramic ball offerings) signals competitive emphasis on meeting the highest industrial abrasion and corrosion demands; GEFA’s catalog move in 2025 is an example of packaging specialty tech into mainstream offers.

- Nil-Cor, Samuel Industries, CERA SYSTEM and other specialised producers — Focus on severe-service niches (chemical, power, petrochemical) where material and design expertise mitigate price competition and enable aftermarket capture.

- Multiple China-based producers — Represent a broad supply base offering cost-competitive assemblies and scale manufacturing. Their role in global trade flows, and the implications of tariffs and certification costs, is a central strategic variable for buyers and incumbents alike.

Recent moves underscore these competitive dynamics: GEFA’s January 2025 catalog integration brings premium ceramic capability into a standard product lane; Allmech’s March 2025 expansion extends large-size, high-pressure offerings for mining; Velan’s 2025 Gulf facility milestone signals regionalisation of supply. Each illustrates how product, geography, and production strategy are being used to capture market share.

What the Full PW Consulting Study Delivers (Actionable Content)

The detailed report is built for commercial and technical leadership teams preparing 2026 plans. Highlights include:

- Validated market sizing (historical 2020–2025 and modeled 2026–2032 forecasts) and scenario variants tied to commodity cycles and trade friction assumptions.

- Supply-chain maps showing supplier concentration for critical ceramic feedstocks, lead-time sensitivity analyses, and cost-to-serve matrices.

- Certification cost modelling (CE/API and equivalents) demonstrating incremental unit-cost impacts and payback thresholds for export strategies.

- Win-loss analysis across product types and actuation strategies, with pricing power matrices and recommended commercial approaches (tendering, value-based pricing, service bundling).

- Competitive positioning profiles and an M&A target shortlist based on technology fit, geographic coverage, and aftermarket potential.

- Operational playbooks: options for capacity expansion, contract manufacturing use-cases, and nearshoring vs. centralized production decision-trees.

- Risk heat maps (logistics, raw material, regulatory) and a 90-day to 24-month prioritized mitigation plan for procurement and operations teams.

Recommended 2026 Actions — A Tactical Checklist

- Run a 12–24 month supply-risk simulation for alumina and zirconia inputs; quantify the P&L impact of 10–25% price shock scenarios and identify hedging or supplier development levers.

- Prioritise certification investments for product lines with cross-border sales potential; treat certification as a market-access and margin management tool rather than a compliance cost only.

- Evaluate regional manufacturing or toll-processing partnerships where logistics or tariffs materially impair competitiveness—use a break-even model that includes time-to-market advantages for aftermarket service.

- Pursue service-led product bundles and extended warranties to capture recurring, high-margin aftermarket revenue.

- Screen potential acquisitions for material technology IP (zirconia/ceramic processing), actuator/control-system integration, or established regional aftermarket networks.

Conclusion — Why PW Consulting’s Intelligence Matters for 2026

The ceramic ball valve market sits at the intersection of materials science, industrial process demands, and geopolitically sensitive supply chains. For 2026 planning, executives must combine modest top-line growth expectations with strategic moves that protect margin and create durable differentiation—through certification, regional supply positioning, or aftermarket service models. Our full report contains the granular split, supplier lists, cost models, and scenario outputs required to execute those moves with confidence.

To access the full dataset, split tables, and the executable 24-month playbook, consult the PW Consulting Ceramic Ball Valve Market report. The detailed intelligence—especially our region/type/application matrices and supplier scorecards—is purposefully held in the full study to inform high-stakes commercial and capital decisions. Contact our team to receive the complete analysis and a tailored briefing for your 2026 planning cycle.

For detailed analysis of this topic, please visit the official page:Ceramic Ball Valve Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com