Polyamide-imide Resin Market Size, Share, Trends, Growth Opportunities, Key Drivers and Competitive Outlook

Other |

2026-06-29 11:14:06

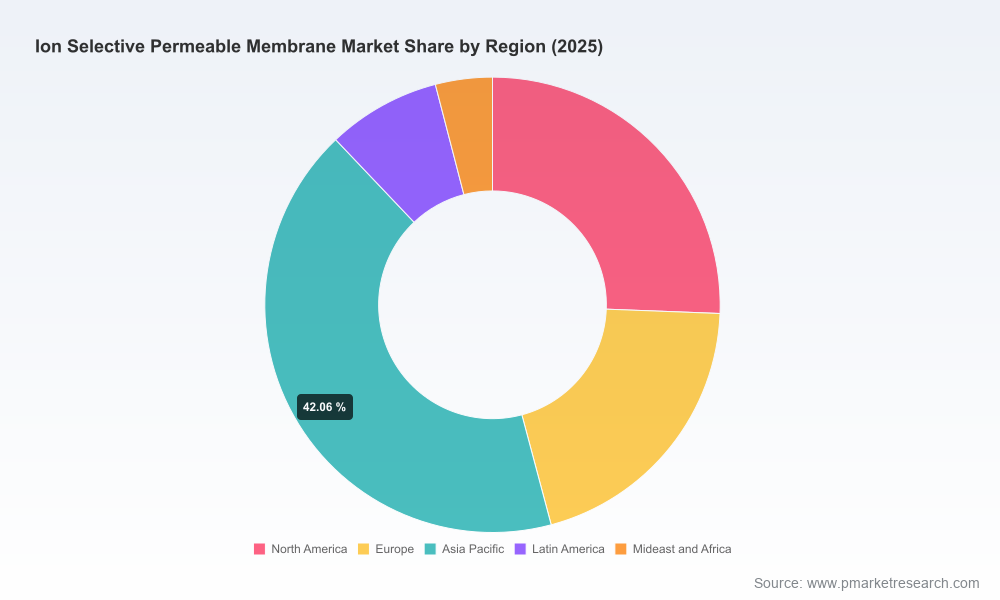

The ion selective permeable membrane market is at an inflection point. After steady expansion through the early 2020s, the market value rose from USD 163.15 Million in 2020 to USD 215.0 Million in 2025, and our base-case forecast shows continued acceleration into the next decade — reaching roughly USD 243.26 Million in 2026 and targeting USD 413.67 Million by 2032 at a compounded annual growth rate of 9.8%. For senior executives making capital allocation, product roadmap, and M&A decisions in 2026, this trajectory signals both opportunity and the imperative to move from pilot-to-scale with rigor.

Ion Selective Permeable Membrane Market

Comprehensive market sizing and a seven-year forecast model with configurable scenario runs for price, adoption, and raw-material stress tests.

Ion Selective Permeable Membrane Market

Technology & product maps that align membrane chemistries, form factors, and lifecycle trade-offs to specific industrial use-cases and operating envelopes.

Ion Selective Permeable Membrane Market

Supply-chain diagnostics that quantify sensitivity to critical feedstocks and identify single points of failure; includes cost-to-serve analysis and recommended hedging strategies.

Actionable go-to-market playbooks (pricing, channel, and service extensions) for incumbents, challengers, and OEM partners.

Competitive profiles and capability matrices for the leading vendors, including production footprints, IP posture, and near-term capacity changes.

Regulatory and standards matrix (including key compliance milestones) and an impact assessment tied to procurement and project timelines.

A tailored M&A screening tool that highlights value-at-risk by technology, region, and use-case, plus integration checklists for post-deal capture.

Three structural forces converge in 2026. First, accelerating decarbonization and electrification projects are expanding demand for membranes in large electrochemical systems (notably green hydrogen and advanced desalination). Second, resource-recovery and specialty-extraction use-cases — including lithium brine purification and high-recovery brine processing — are maturing from pilots to commercial deployments. Third, raw-material dynamics and evolving standards are increasing the cost and complexity of reliable supply.

These shifts are visible in recent industry moves: major manufacturers are adding capacity and modular production lines, with new facilities and expansions scheduled to come online in the 2025–2026 window. Leading suppliers have also introduced next-generation membrane chemistries designed for higher selectivity and durability, and industry awards and standards bodies are signaling rising expectations for lifecycle performance and materials engineering. Together, these actions compress commercial windows and raise the bar for go-to-market readiness in 2026.

The market exhibits material concentration at the top: the three largest players account for a clear majority of industry revenues, and the top five further increase that concentration. This structure creates a market dynamic where scale, validated reliability, and long-term supply commitments are significant competitive advantages. Yet, it also leaves tactical openings for focused entrants and tier-two players that can offer differentiated performance, cost, or integration services.

MEGA a.s. (Czech Republic): Deep heritage in heterogeneous ion-exchange membranes and custom formats; strong in roll-to-roll and tubular manufacturing for electrodialysis applications.

DuPont (United States): Invested in nanofiltration and ion-exchange lines targeted at resource recovery; recognized for innovation through industry accolades.

Asahi Kasei (Japan): Broad portfolio including electrolysis cell components; recent capacity moves and material innovations have strengthened its positioning in alkaline electrolysis and chlor-alkali markets.

AGC Inc. (Japan): Advancing fluorinated membrane manufacturing with a new plant designed to support green hydrogen production at scale.

Solvay, FUMATECH, SnowPure, Saltworks, ASTOM, ResinTech, Dow, and Lanxess: Each brings specialized strengths — from ultra-high-purity membranes for pharma to reinforced membranes for heavy industrial electrolysis — creating a mix of capabilities across performance, cost, and service.

Strategically, incumbents with integrated value chains are using capacity expansions and differentiated chemistries to lock in large OEMs and utility-scale projects. Challenger vendors tend to target high-margin niches (ultra-pure, specialty separations, or hybrid system integration) or pursue partnership models with system integrators and brine-to-battery initiatives.

Raw-material concentration: Dependence on perfluorinated polymers drives cost exposure and creates a performance trade-off between selectivity and fouling sensitivity. Producers that secure feedstock supply or engineer substitute chemistries will obtain durable margin advantages.

Standards and certification: New standards for electrodialysis and membrane systems raise the bar for validated field performance. Compliance timelines should be incorporated into procurement lead times and product-release gate criteria.

Capex and capacity timing: Announced facility ramp-ups move the market from tightness to incremental oversupply in some subsegments; timing and geography of those ramps are decisive for pricing dynamics in 2026–2027.

Technology risk: Incremental improvements in fouling resistance and lifetime often deliver more commercial value than headline selectivity metrics. Commercial pilots should therefore prioritize lifecycle economics over single-run performance.

Secure upstream supply: Negotiate multi-year contracts with polymer suppliers, explore toll-manufacturing agreements, and diversify chemistry suppliers to mitigate feedstock shocks.

De-risk scale-up with modular capacity: Favor modular or regional production that can be expanded in phases; this reduces capital lock-up against uncertain near-term demand surges.

Commercialize service and performance guarantees: Offer outcome-based contracts (e.g., lifetime, throughput, fouling recovery) that align vendor incentives with customer OPEX priorities.

Invest in pilot economics: Allocate engineering resources to field-proven pilots that capture operational degradation data — these datasets unlock premium pricing and accelerate adoption.

Pursue strategic partnerships: For new entrants, partner with system integrators, specialty chemical firms, or niche OEMs to accelerate market access and validate materials in live systems.

Monitor standards and procurement cycles: Build regulatory-compliance roadmaps into product development to avoid late-stage rework and to gain early-adopter status on projects governed by modern standards.

Decision-makers should run at least three internal scenarios (base, accelerated adoption driven by hydrogen/desalination projects, and downside raw-material shock). For each scenario, track a compact set of KPIs that meaningfully drive valuation and operational choices:

Installed capacity utilization and time-to-commercial ramp for new facilities

Realized membrane lifetime and fouling-related replacement frequency

Average selling price and service-revenue mix

Supply-chain concentration (number of qualified polymer suppliers) and hedging coverage

Bid-to-win conversion rates for system OEMs and utilities

The market’s growth profile — roughly doubling over the coming six years at close to a 10% CAGR — makes selectively acquisitive strategies compelling. Buyers should prioritize targets that deliver one or more of the following: proprietary membrane chemistries with demonstrable lifetime gains, captive or validated supply agreements for risky feedstocks, strong OEM partnerships, and control of critical manufacturing processes that are hard to replicate. Post-deal integration should aim to capture synergies in upstream procurement, accelerate commercialization through combined sales channels, and preserve nimble R&D roadmaps.

For any executive or investor with exposure to electrolyzers, desalination, resource-recovery, or specialty separations, the choices made in 2026 will determine competitive positioning for the next decade. The market’s size and growth trajectory create attractive upside, but capture requires more than technology claims — it requires integrated supply planning, field-validated lifecycle performance, and a commercial model that converts technical advantage into repeatable revenue.

PW Consulting’s full Ion Selective Permeable Membrane Market study provides the granular segmentation, company-level benchmarking, downloadable financial models, and implementation playbooks that decision-makers need to convert the 2026 inflection into durable advantage. Access the complete intelligence pack on the PW Consulting report page to unlock segment-level forecasts, vendor scorecards, and executable roadmaps tailored to your strategic posture.

For detailed analysis of this topic, please visit the official page:Ion Selective Permeable Membrane Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com