US Rx Medical Food Market Demand Across Healthcare

Other |

2026-07-06 12:43:30

As the building blocks of modern dry-mix construction chemistry continue to evolve, Hydroxypropyl Starch Ether (HPS) has moved from a niche additive toward a core material influencing product performance, cost structure, and sustainability narratives across multiple end-markets. PW Consulting’s latest HPS Market study (base year 2025; historical 2020–2025; forecast 2026–2032) synthesizes commercial, technical, and regulatory intelligence to create a pragmatic playbook for strategic decision-making in 2026. The headline: the HPS market has demonstrated steady growth—expanding from roughly USD 152 million in 2020 to about USD 199 million in 2025—and is projected to reach nearly USD 289 million by 2032, corresponding to a mid-single-digit CAGR of 5.5% across the 2026–2032 forecast window. This trajectory reflects structural demand resilience coupled with evolving product specifications and supply-chain considerations.

Hydroxypropyl Starch Ether (HPS) Market

Actionable foresight for near-term capital allocation: The report translates market momentum into investment signals—when to accelerate capacity expansion, when to defer, and how to sequence CAPEX to capture high-margin segments without overexposing firms to cyclical inventory risk.

Hydroxypropyl Starch Ether (HPS) Market

Procurement and cost-risk playbook: Volatility in native starch prices and logistics premiums materially affects input cost. The study provides scenario-based raw-material sensitivity analysis that supports hedging, vertical integration, and supplier diversification strategies.

Hydroxypropyl Starch Ether (HPS) Market

Commercial and go-to-market alignment: As product formulations and performance expectations shift, procurement teams and product managers need coordinated plans. Our research includes go-to-market frameworks to align technical claims to distributor economics and applicator adoption cycles.

Regulatory and sustainability readiness: Construction chemistry is increasingly subject to indoor air quality standards and bio-based material incentives. The study frames regulatory scenarios and stepwise compliance strategies that preserve margin while improving market access.

This is not a catalog of numbers. It is an execution-oriented intelligence package for executives, commercial leaders, and product teams. Highlights include:

Transparent market sizing and trend diagnostics — historical performance (2020–2025) and a detailed forecast (2026–2032) with sensitivity bands tied to raw material and construction activity scenarios.

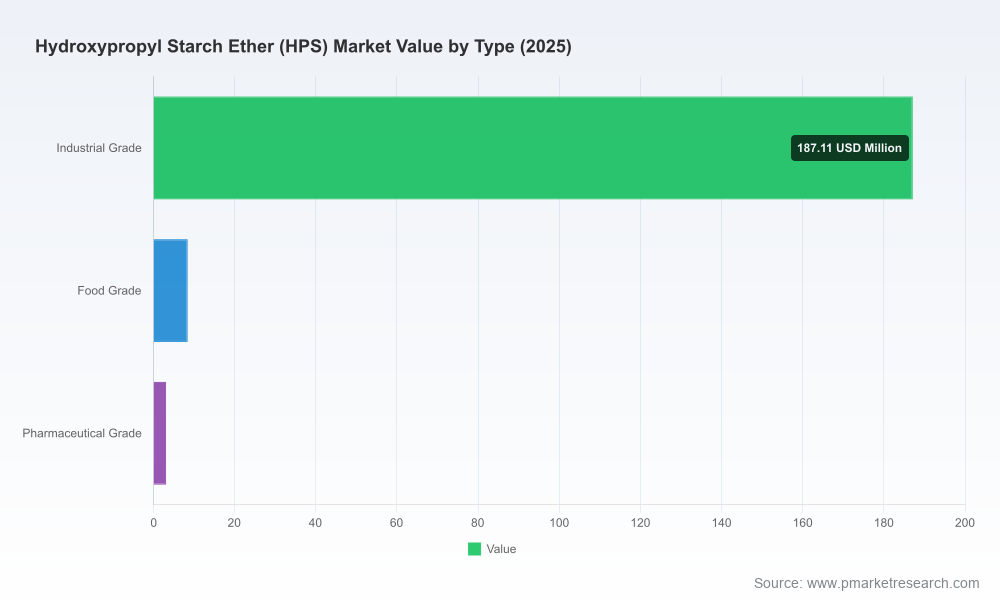

Demand segmentation logic — end-use drivers, formulation trends, and performance attributes that matter to formulators and applicators (note: the full report contains the granular regional, type, and application splits and their implications).

Supply-side mapping — manufacturer footprints, capacity typologies, and logistics chokepoints that determine lead times and negotiating leverage.

Price and margin modeling — an integrated cost-to-serve model that links feedstock prices, energy, labor, and freight to downstream pricing elasticity under different end-market scenarios.

Regulatory matrix and sustainability pathway — compliance timelines, certification implications, and potential premium positioning for bio-based or low-VOC formulations.

Commercial playbooks — product positioning, distributor economics, sample commercial contracts, and tender-response templates tailored for HPS suppliers and formulators.

Risk heatmaps and mitigation strategies — supply disruption, trade policy shifts, and substitution risks, with contingency options prioritized by cost and speed of execution.

Vendor and technology diligence — supplier scorecards, innovation benchmarking, and decision criteria for M&A or JV opportunities.

The HPS market exhibits a concentrated structure at the top: the three-largest suppliers account for a substantial portion of market volume, with the top-five concentration increasing only modestly beyond that. This concentration, combined with high technical entry barriers (formulation know-how, consistent starch sourcing, and quality control at scale), shapes pricing dynamics and strategic options for both incumbents and challengers.

Incumbent positioning: Established producers with a construction-centric product focus command relationship advantages with tile-adhesive and dry-mortar formulators. Their strengths include application-specific grades, validation history, and integrated quality protocols that reduce adoption friction for downstream manufacturers.

Challenger playbooks: New entrants and specialty players typically compete on differentiated service models (faster lead times, technical support), price, or narrow innovation pockets (e.g., tailored viscosity profiles or improved freeze–thaw stability). For challengers, targeted regional entry or strategic partnerships with formulators accelerates adoption without requiring full-scale production footprint immediately.

Pricing leverage and supplier negotiation: Given concentration metrics, large buyers can extract commercial concessions via volume commitments, co-development agreements, or multi-year offtake contracts; smaller buyers often trade on flexibility and local supply chain advantages.

The competitive landscape section profiles producers with substantial footprint and brand recognition in the HPS space. Profiles summarize positioning, core product claims, typical end-use focus, and geographic orientation:

Shijiazhuang Henggu (Matecel®): A supplier focused on construction-grade HPS, with an emphasis on dry-mix mortar and tile-adhesive applications. Known for validated formulations and customer technical support offerings.

Kima Chemical: Supplies HPS as a multifunctional additive (thickener, stabilizer, emulsifier) tailored for cementitious and gypsum-based products, emphasizing consistency in rheology performance.

WOTAIchem: Producer of HPS powders positioned for dry-mortar systems and construction additives, with capabilities across cellulose ethers and related products.

Shandong Landu (NOVA STAR™): Markets HPS across construction and specialty applications (food, pharma, personal care), combining broad product reach with a commercial approach aimed at multi-segment adoption.

These profiles are synthesized to highlight what matters for strategic choices—product claims, application validation, supply consistency, and support services—without disclosing the full proprietary segmentation data. Detailed competitive benchmarking, plant-level risk assessments, and supplier scorecards are available in the full study.

Prioritize integrated sourcing strategies: Short-term tactical buying reduces cost but increases vulnerability to feedstock swings. For industrial buyers, a blend of contracted volumes, regional dual sourcing, and selective vertical integration into starch processing can materially reduce EBITDA sensitivity.

Differentiate through application support: Technical service capabilities (lab support, on-site trials, formulation co-development) accelerate uptake and justify premium positioning versus commoditized supply offers.

Targeted capacity moves, not broad-scale rollouts: Given the market’s measured CAGR and concentrated supplier base, well-timed incremental capacity additions win share without triggering destructive price competition. Our scenario models identify the timing windows where marginal capacity is absorbed versus where it risks depressurizing margins.

Embed sustainability as a commercial lever: Certification and low-emissions claims are increasingly table stakes in institutional and export markets. Investing in traceability and green claims yields both price premiums and longer-term demand stability.

Prepare for regional differentiation: While demand drivers are broadly similar across construction-focused end-markets, local standards, installer preferences, and logistics shape adoption. Craft region-specific product and pricing blueprints rather than a monolithic global roll-out.

Use M&A and partnerships judiciously: Bolt-on acquisitions can accelerate access to validated grades, customer lists, or regional distribution. The full report flags acquisition-sized targets and JV archetypes evaluated on time-to-commercialization and synergies.

The study combines proprietary market modeling, supplier interviews, formulation testing summaries, and legal/regulatory mapping to produce recommendations that are both strategic and immediately implementable. For procurement teams, the report includes negotiation playbooks and contract templates structured around volume tiers, quality gates, and penalty clauses for non-conformance. For product teams, we provide a prioritized R&D roadmap that maps customer pain points to formulation experiments and expected time-to-market. For corporate development, we identify diligence checklists and value-creation levers for potential acquisitions.

This introduction is designed to show the analytical depth and practical orientation of PW Consulting’s HPS Market study while preserving the proprietary segmentation and supplier-level detail that underpin concrete commercial decisions. For the full data sets (regional and application splits, supplier scorecards, plant-level risk, and the complete scenario-forecast files), please consult the PW Consulting research portal or contact our client services team to obtain the comprehensive report and a tailored briefing that maps the findings to your organizational priorities for 2026.

For detailed analysis of this topic, please visit the official page:Hydroxypropyl Starch Ether (HPS) Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com