Liquid Packaging Carton Market — A Strategic Preview for 2026 Decision-Makers

As global beverage and chilled-food manufacturers confront tightening recyclability regulations, shifting raw-material cost profiles, and mounting brand expectations for sustainability, the liquid packaging carton sector is at an inflection point. This preview synthesizes the critical, board-level implications from PW Consulting’s full Liquid Packaging Carton Market study (base year 2025, forecast 2026–2032). It is designed to demonstrate the study’s practical value for 2026 corporate strategy without disclosing the granular segment-level intelligence reserved for the full report.

Liquid Packaging Carton Market

Macro picture: growth trajectory you cannot ignore

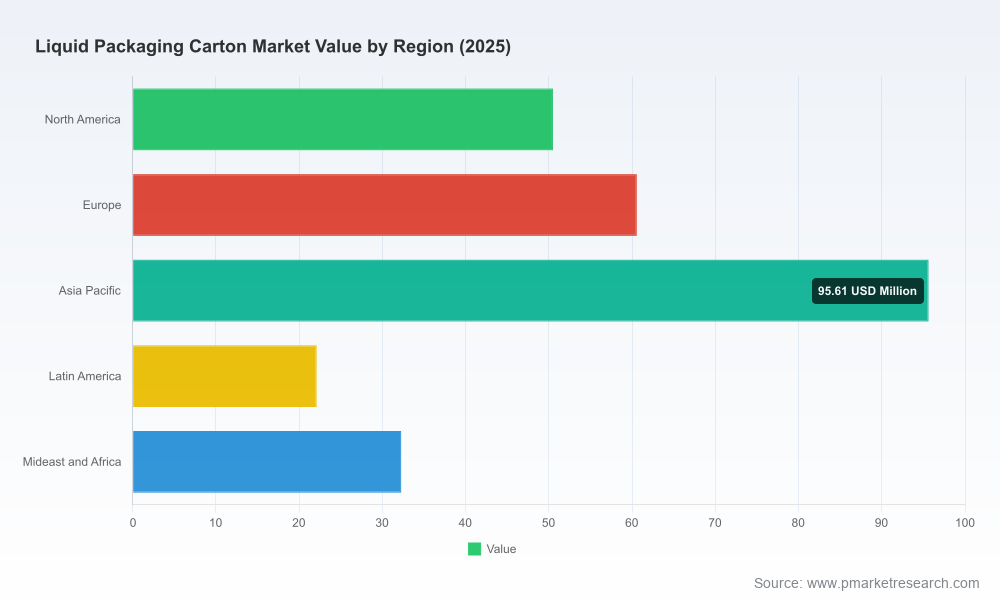

The addressable market for liquid packaging cartons shows steady, mid-single-digit expansion. From the report’s 2025 base estimate, the industry is projected to grow at a compound annual growth rate of 5.58% through the 2026–2032 forecast window. By the end of that horizon the market scale approaches the upper hundreds of millions in USD (reported in the study in revenue units). This pace reflects a combination of continued demand for aseptic and chilled carton formats, accelerated substitution away from single-use plastics in several regulated markets, and incremental value capture via premiumized and sustainable pack formats.

Liquid Packaging Carton Market

Why this study matters to 2026 executives

- Strategic clarity under regulatory pressure — Our analysis maps how evolving design-for-recycling guidelines and EU single-use plastics policies reshape product roadmaps, capital allocation, and supplier selection for both multinational brands and regional producers.

- Investment prioritization — The study translates market growth envelopes and technology trajectories into practical CAPEX and conversion-plant decision rules (when to expand, retrofit, or relocate capacity).

- M&A and partnership scouting — We identify where consolidation is most likely to create scale or capability advantages given the current competitive concentration and the emergence of new materials (e.g., paper-based barriers and alu-free options).

- Commercial levers and margin protection — The research provides pricing sensitivity models tied to raw-material drivers (paperboard, LDPE, aluminium) and logistics cost scenarios to defend margins through 2032.

Core dynamics reshaping the sector

Four interlocking themes dominate near-term strategic planning:

Liquid Packaging Carton Market

- Regulatory and recycling imperatives: Design-for-recycling criteria now target liquid cartons explicitly, pushing conversion technology and material science to prioritize structures that boost recyclability while preserving aseptic performance. This is forcing manufacturers to re-evaluate layer composition and supplier contracts.

- Material composition and substitution: Standard aseptic carton constructions remain multi-layered — primarily paperboard, with plastic and aluminium components — and incremental reductions in aluminium and plastics are becoming both a regulatory and brand priority. The practical implication is rising demand for alternative barrier technologies and for converters capable of integrating those barriers at scale.

- Product and format innovation: A wave of new 1-litre and alu-free formats is accelerating premiumization and sustainability positioning on retail shelves. These innovations create a two-speed market: incumbents moving to defend high-volume SKUs and challengers leveraging differentiated materials or filling capabilities to win share.

- Concentration and capability clustering: Market concentration is meaningful but not prohibitive to competition; leading suppliers capture a substantial portion of volume while regional and specialist converters retain strategic niches. This creates both partnership opportunities and pressure points for brands seeking backup capacity or localized supply.

Competitive landscape — what the market structure implies

PW Consulting’s study profiles the industry’s prominent players and distils the strategic takeaways for each category of participant. Key firms we analyze include global systems and material providers, regional converters, and integrated beverage-pack producers. Highlights actionable to 2026 strategy:

- Global systems leaders — Established players with broad technology platforms continue to invest in material science and aseptic filling innovation. Their R&D and co-development partnerships accelerate adoption of new barrier concepts and ensure compliance pathways for major brand customers.

- Regional champions and converters — Firms with local manufacturing footprints are executing focused investments to shorten lead times and provide localized sustainability credentials to manufacturers wanting region-specific claims.

- Material specialists and entrants — Newer entrants focused on alu-free and paper-based barrier systems are turning product launches into commercial momentum, forcing incumbents to accelerate their own timelines or partner with innovators.

Recent commercial developments exemplify these dynamics: strategic product launches by major suppliers introducing alu-free 1-litre formats, as well as targeted capacity investments in conversion and filling plants in North America and elsewhere. These moves underline the dual imperatives of material innovation and localized production capacity.

What the report contains — practical, decision-ready modules

The full PW Consulting study is organized into operationally useful modules tailored for executive use. Key deliverables include:

- Proprietary market-sizing and forecasting model (2020–2032), with scenario variants reflecting regulatory, material-cost, and demand shocks.

- Technology and materials roadmap that maps barrier options, recyclability performance, and likely adoption timetables.

- Supplier ecosystem atlas: profiles of global and regional converters, equipment suppliers, and raw-material vendors, with capability matrices and strategic fit scores.

- Commercial playbooks: go-to-market templates for brands, co-manufacturers, and converters (pricing frameworks, packaging-led SKU rationalization, promotional packaging strategies).

- Operational decision tools: CAPEX prioritization rules, plant-location scoring models, and supply-chain resilience checklists.

- Sustainability impact models that quantify recyclability improvements, life-cycle trade-offs, and communications risk for label claims.

- M&A watchlist and valuation heuristics—target profiles based on capability gaps (e.g., alu-free barrier IP, aseptic filling scale, regional converter footprints).

How to act in 2026 — role-specific recommendations

The study reframes market intelligence into immediate tactical actions by function:

- Chief Procurement Officer: renegotiate long-dated contracts with variable-index clauses tied to fibre and polymer indices; diversify supplier base to include alu-free barrier providers as a strategic hedge.

- Head of R&D / Packaging Innovation: accelerate co-development projects with material innovators; prioritize pilot runs for alu-free and paper-based barrier formats to validate shelf-life and filling compatibility.

- Head of Sustainability: align pack development roadmaps with regional design-for-recycling criteria; quantify trade-offs between pack lightweighting and recyclability in your corporate sustainability targets.

- Operations and Plant Leadership: use the report’s CAPEX rule set to decide between retrofitting existing lines for new materials versus investing in greenfield converting capacity closer to key markets.

- M&A and Corporate Development: use the study’s target profiles to prioritize acquisitions that fill capability gaps (e.g., regional conversion capacity, filling technology, barrier IP) and to time buy-side activity against market growth windows.

Risk framework and near-term headwinds

Strategic planning should integrate three principal near-term risks identified in the study:

- Regulatory mismatch risk: differing recycling and labelling standards across jurisdictions create potential market fragmentation; readiness to certify new formats across multiple programs is essential.

- Material supply volatility: fluctuations in pulp, polymer and aluminium markets can compress margins; firms lacking linked hedging strategies or flexible bill-of-materials face disproportionate exposure.

- Adoption and performance risk: new barrier technologies must clear food-safety and shelf-life hurdles; commercial rollouts without rigorous validation may damage brands and slow category adoption.

Why PW Consulting’s report is a must-have for 2026

Because the next 18–24 months will set the trajectory for conversion investments, material choices and go-to-market plays, executives require more than high-level forecasts — they need executable playbooks and validated supplier intelligence. Our study couples a robust market-growth view (5.58% CAGR through the forecast horizon) with scenario-tested operational tools and supplier-level insight. It converts market-size projection into discrete strategic decisions: where to invest, who to partner with, and how to defend margins while meeting rising sustainability requirements.

Next steps — how to access the full intelligence

This preview intentionally omits the detailed segmentation metrics and the granular supplier scoring that make the full report a practical decision tool. For access to the complete dataset, including the segmentation matrices, interactive forecasting model, supplier heatmaps, and the step-by-step strategic playbooks tailored to different corporate archetypes, please consult the PW Consulting report portal. The full study is instrumented to support board-level presentations and operational roadmaps that procurement, R&D, and corporate development teams can implement immediately.

PW Consulting stands ready to walk your leadership team through a targeted executive briefing of the findings and to workshop a 90-day action plan tailored to your role in the liquid packaging carton value chain.

For detailed analysis of this topic, please visit the official page:Liquid Packaging Carton Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com