Smartphone Camera Lens Market: Strategic Outlook for 2026 Decision-Making

Executive overview

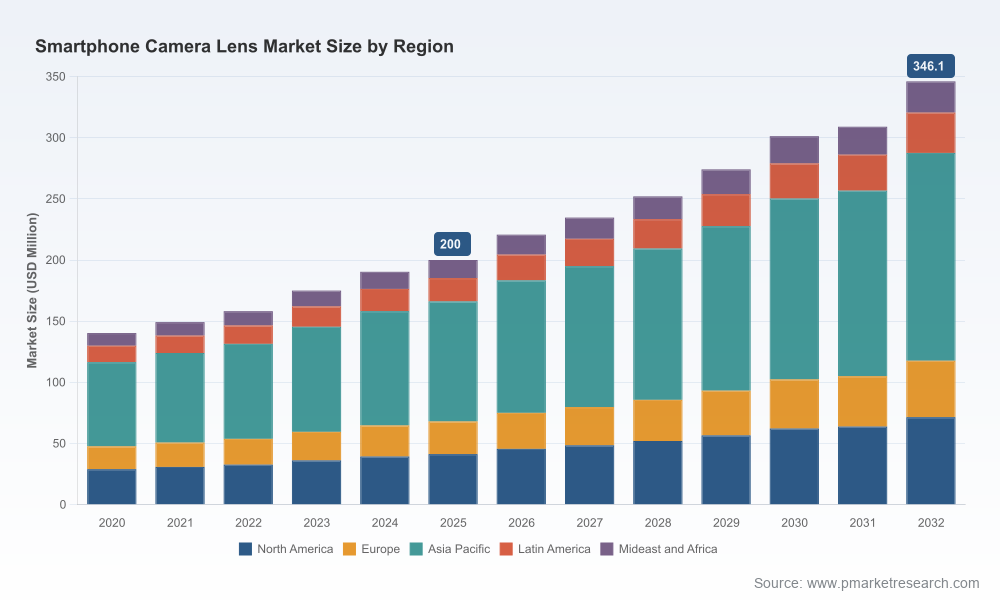

As global device makers and optics suppliers pivot to a profile of higher-resolution sensors, multi-camera arrays and emerging form-factors (foldables, under-display, XR-enabled handsets), the smartphone camera lens market is entering a decisive growth phase. Our PW Consulting analysis uses 2025 as the base year (historical window 2020–2025; forecast horizon 2026–2032) and projects the industry to expand at a compounded annual growth rate (CAGR) of 8.21% through the forecast period. After growing from roughly USD 140 million in 2020 to USD 200 million in 2025, the market is modeled to approach the mid-hundreds by 2032 under the central case.

Smartphone Camera Lens Market

This research is calibrated for 2026 corporate decision-making: procurement leaders, product planners, strategy teams and private equity investors will find signal-rich analysis that translates macro momentum into concrete operational choices. The analysis blends market sizing, technology adoption timelines, supplier economics, and competitive strategy into a compact playbook for steering product and supply-chain decisions in the year ahead.

Smartphone Camera Lens Market

Why this report matters for 2026

- Technology inflection requires faster decisions. The pace of transition from traditional plastic optics to hybrid assemblies and wafer-level glass (WLG) is accelerating. Component choices today determine optical performance, BOM structure and supplier relationships for multiple device generations.

- Supply-side consolidation and concentration create negotiation windows — and risks. The market shows mid-level concentration among tier‑one lens suppliers, creating asymmetric bargaining power in some subsegments while leaving niches for specialized entrants.

- Raw-material dependency is strategic. A small set of advanced resins and glass formulations underpin the latest compact optics; dominance among a few material providers amplifies single-source risk and price exposure unless proactively managed.

- Cross-domain demand opens new growth and risk vectors. Suppliers are moving capacity toward automotive and XR applications, which has implications for qualification cycles, pricing and capacity allocation for consumer-grade production.

- Regulatory and quality thresholds matter. Automotive-grade certification and other quality accreditations are being applied to higher-end mobile optics lines, shifting cost structures and capital requirements for manufacturers that want to remain competitive across end markets.

What the PW Consulting report delivers

This is not an academic review. The report is a practitioner’s dossier designed to be immediately actionable for 2026 planning cycles. Key deliverables include:

Smartphone Camera Lens Market

- Top-down and bottom-up market models (historical 2020–2025; forecast 2026–2032) with scenario variants (base, upside, downside) that stress-test sensor roadmap and handset ASP assumptions.

- Technology roadmaps mapping the adoption timing and cost inflection for plastic, glass, hybrid and wafer-level glass lenses — including expected OEM windows for periscope and multi-sensor arrays.

- Supplier economics and cost-to-serve matrices that illuminate margin pools, outsourcing trade-offs and the real drivers of gross-margin pressure across production footprints.

- Practical procurement playbooks — supplier scorecards, qualification timelines, capacity reservation strategies and hedging approaches for critical resins and glass families.

- Deal-oriented content: M&A target typologies, JV structures for capacity expansion, and integration risk matrices to evaluate tuck‑ins and strategic partnerships.

- Operational checklists and KPIs for quality certification (including automotive-grade production paths), environmental and labor-cost sensitivities, and factory automation levers.

Competitive landscape — synthesis and implications

The market is anchored by a small number of established, vertically integrated suppliers and several strong regional specialists. Our competitiveness scoring and profiling in the report focus on capabilities that matter in 2026: optical design IP, manufacturing precision, module integration, quality systems and OEM relationships.

- Largan Precision — Long-standing strength in precision aspherical optics and deep OEM relationships. Recent public disclosures point to modest top-line expansion alongside margin pressures driven by outsourced components and currency moves. Strategic implication: Largan’s combination of design IP and OEM trust makes it a default partner for premium optics; negotiation teams should plan for rate discipline but also leverage Largan’s roadmap for flagship designs.

- Sunny Optical — Broad portfolio across hybrid and periscope assemblies, with aggressive capacity investments and a deep push into automotive-grade lenses. Strategic implication: Sunny’s scale and vertical breadth make it a corner-case supplier for large-volume programs; buyers should evaluate co-investment or volume-commitment models if they need preferential allocation.

- Samsung Electro-Mechanics — Integration advantage as a module-level supplier with in‑house actuators and PCBs. Strategic implication: For OEMs seeking platform-level integration and reduced coordination overhead, Samsung offers compelling bundled solutions but may command premium terms for tight integration.

- Genius Electronic Optical and AAC Technologies — Specialists pushing into advanced optics and WLG; AAC’s recent product launches signal vendor readiness to supply next-generation compact solutions. Strategic implication: These players are attractive for co-development arrangements and contingency sourcing to diversify supplier risk.

- Kantatsu and Sekonix — Niche strengths in micro-lens units, aspherics and targeted mobile/automotive applications. Strategic implication: High-precision niche suppliers are prime targets for OEMs and tier‑one integrators looking to secure differentiated optical features without shifting large volumes.

Market concentration metrics in our model indicate a moderate level of aggregation among top suppliers. That dynamic is creating both leverage for leading vendors and opportunity for specialized challengers to capture feature-driven pockets of demand.

Key industry dynamics to factor into 2026 decisions

- Materials and single-source risk: A narrow set of advanced polymers and glass compositions are critical to the newest compact optics. Buyers should quantify supplier lock-in and build contingencies into contracts and NPI timelines.

- Certification and cross-market qualification: Automotive-grade lines and XR qualification cycles significantly lengthen time-to-volume. Suppliers that invest in these capabilities will reprice their offering to reflect the extended qualification risk.

- Margin pressure and outsourcing trade-offs: The choice between maintaining higher in-house value add versus outsourcing to component specialists has immediate margin and operational implications. Our modeling shows outsourcing can depress gross margin in the near-term even as it lowers capital intensity.

- Capacity investment timing: Supplier capital plans matter — capacity expansions targeted at adjacent markets (e.g., automotive) will change allocation dynamics for consumer smartphone volumes. Early allocation agreements can secure supply but may require revenue guarantees or co-funding.

- Geopolitical and relationship capital: Long-established supplier–OEM relationships remain a competitive moat. New entrants must anticipate prolonged qualification cycles to penetrate flagship programs.

Actionable strategic recommendations for 2026

- Prioritize a dual-sourcing strategy for critical optics families and negotiate capacity reservation clauses tied to clear performance milestones.

- Invest selectively in co-development with suppliers of wafer-level glass and hybrid optics to accelerate in-house differentiation while sharing NPI risk.

- Build a materials-risk dashboard and contractual clauses for key resins and high-index glass to mitigate single-source exposure and price shock.

- Evaluate targeted minority investments or JVs with high-precision niche suppliers to secure capability for advanced periscope and micro‑lens assemblies.

- Embed certification timelines (automotive, XR) into product roadmaps and align procurement KPIs with supplier qualification stages to avoid launch bottlenecks.

- Model margin sensitivity to outsourcing and FX scenarios; use conservative gross‑margin assumptions when authorizing production shifts or vendor consolidations.

How to use the full PW Consulting report

This preview outlines the strategic frame; the full report contains the operational maps you need to implement the recommendations. It includes:

- Complete market tables and interactive scenario models (2020–2032) tailored to OEM, tier‑one supplier and component-supplier views.

- Supplier scorecards with capability heatmaps, manufacturing footprints and qualification timelines.

- Procurement templates, preferred‑supplier contracting language and an M&A playbook with candidate targets and valuation heuristics.

- Risk matrices and stress tests that quantify sensitivity to material price moves, FX shifts and capacity reallocation into adjacent markets.

Because this article serves as a strategic preview, granular segment and regional splits that underpin our full-market model are intentionally omitted here. Access to the full dataset and the downloadable Excel model is available on the PW Consulting website and will enable you to run bespoke scenarios against your program assumptions.

Closing

2026 will be a make-or-break year for organizations that supply or source smartphone camera optics. The combination of robust market growth, technology shifts and supplier consolidation creates openings for decisive action — whether that means locking supply through contractual commitments, investing in co-development, or pursuing tactical M&A. PW Consulting’s full report equips you with the data, supplier intelligence and implementation playbooks to convert market momentum into sustainable competitive advantage. To gain access to the full findings and downloadable tools, visit the PW Consulting research portal for the Smartphone Camera Lens Market.

For detailed analysis of this topic, please visit the official page:Smartphone Camera Lens Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com