Fuel Additives Market 2026: Strategic Imperatives for CEO, CPO and Product Leaders

As PW Consulting’s Senior Strategy Advisor and Head Industry Analyst, I present a forward-looking primer that positions our full Fuel Additives Market study as an operational playbook for boardroom decisions in 2026. This brief synthesizes the market’s macro trajectory, competitive dynamics and regulatory inflection points to show where value will be created — and lost — over the coming planning cycle. It intentionally demonstrates analytical depth while reserving the granular regional, application and price-by-product datasets for the full report on our website.

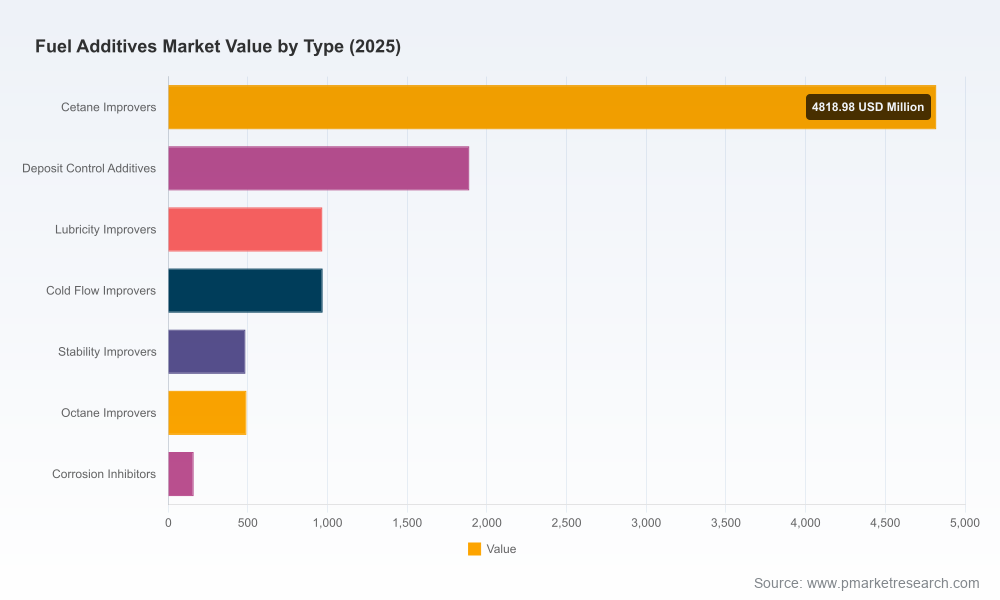

Fuel Additives Market

Where the market stands and where it is headed

Between 2020 and 2025 the global fuel additives market delivered robust expansion, moving from an early‑cycle baseline to a materially larger market by the 2025 base year. Our forecast through 2032 projects continued growth at a compound annual growth rate (CAGR) of 5.8% across the 2026–2032 horizon. By mid‑decade, that growth has created a market environment in which scale, certification and local service capability determine commercial outcomes as much as product chemistry.

Fuel Additives Market

Two structural features shape the outlook. First, performance and compatibility now sit on equal footing with cost: regulators and OEMs are imposing lower additive dosage floors and certification requirements, while fuels containing increasing proportions of bio‑blendstocks require tailored stability and lubricity solutions. Second, the competitive structure is moderately concentrated — leading suppliers hold a majority of market influence — which magnifies the effect of strategic moves such as product certification, regional capacity investments and alliance formation.

Fuel Additives Market

Why this report matters to 2026 decisions

- Speed: Executives need a 12–18 month execution playbook tied to the 2026 regulatory calendar, refinery planning cycles and channel contracting windows. This report maps those timeboxes to tactical actions.

- Risk‑adjusted investment: Capital allocation decisions for blending lines, local warehousing, and formulation R&D hinge on quantified demand scenarios. Our forecast and scenario suite translates strategic options into expected ROI bands under three plausible regulatory and raw‑material scenarios.

- Commercial positioning: With certification programmes (TOP TIER+ and analogous standards) becoming de‑facto market access gates, the study shows how first‑mover certification and a complementary channel strategy drive share gains without disproportionate marketing spend.

- Supply chain resilience: The market’s exposure to specific feedstock inputs and blending capacity bottlenecks is modelled to show where hedging, nearshoring and toll‑blending strategies materially reduce downside.

Competitive landscape — actionable synthesis

The market is shaped by a handful of global specialists, each bringing distinct capabilities that determine an incumbent’s playbook in 2026:

- Afton Chemical Corporation — recognized for gasoline performance additives and GDI‑oriented deposit control. Afton’s TOP TIER+‑approved launches position it to defend premium retail and OEM channels where performance claims translate to pricing power.

- Infineum International — a dual gasoline/diesel portfolio player that has been actively localizing production in high‑growth markets. Their recent capacity additions reflect a strategic bet on blended fuels and on‑shore supply to reduce lead times and logistics cost for regional blenders.

- Lubrizol Corporation — a broadly diversified additive house noted for cold‑flow and multifunctional packages. Lubrizol’s scale in customer testing and aftermarket service creates stickiness beyond price competition.

- Chevron Oronite — strong in refinery‑grade additives and detergent packages; its integration with refinery customers allows faster route‑to‑market for formulation changes tied to crude slate adjustments.

- Innospec Inc. — specialization in diesel additives and multifunctional gasoline formulations creates opportunities in fleet and aviation segments where product performance drives procurement decisions.

- BASF SE — combining chemical R&D depth with a rapid product certification cadence; recent launches certified for new performance standards underscore the advantage of aligning R&D pipelines to anticipated regulatory test protocols.

Collectively, leading firms benefit from economies of scale in R&D and blending, distribution relationships with fuel marketers, and access to laboratory infrastructure for validation. Market concentration metrics indicate that the top three and five suppliers capture a dominant share of value, reinforcing the strategic importance of partnerships, targeted acquisitions and fast certification cycles for challengers and incumbents alike.

Regulatory and raw‑material dynamics that will drive decisions in 2026

- Renewable Fuel Standard updates and higher mandated volumes of renewable blending are already shifting demand composition. Companies must plan formulations for ethanol and renewable diesel compatibility to avoid market marginalization.

- EPA dosing criteria — such as lowest additive concentration (LAC) rules — and ongoing obligations like annual Form 3520‑13A submissions add compliance costs that favor players with centralized regulatory teams and digital compliance workflows.

- Recent enforcement discretion rulings on portable fuel container requirements alter product packaging and distribution timelines for some additive formats; procurement and legal teams should re‑assess shelf‑stock strategies and labelling timelines.

- Volatility in key feedstocks necessitates proactive sourcing strategies: toll‑blending agreements, backward integration, and multi‑sourcing are no longer optional for mid‑sized players seeking stable gross margins.

What the full study delivers — practical contents

The full PW Consulting Fuel Additives Market study is designed as an execution tool rather than a descriptive paper. Key deliverables include:

- Proprietary market model (2020–2032) with scenario toggles for regulatory, feedstock and OEM adoption variables that produce company‑level revenue impacts under three stress cases.

- Commercial playbooks for incumbents, regional challengers and new entrants: go‑to‑market roadmaps, sample commercial terms, margin waterfall analyses and channel activation templates.

- Regulatory compliance matrix and recommended timeline to meet certification standards (including test protocol alignment and sample submission checklists) to accelerate TOP TIER+ and equivalent approvals.

- Supplier and feedstock risk heatmap, with contract negotiation scripts and hedging options, plus a shortlist of toll‑blenders and contract manufacturers for rapid scale‑up.

- M&A screening toolkit: target scoring model, integration risk checklist and a prioritized list of bolt‑on capabilities that deliver immediate synergies in blending and regional distribution.

- Commercial analytics workbook: price elasticity proxies, channel segmentation KPIs, and distributor scorecards to optimize portfolio mix and incentive schemes.

Recommended 90‑ to 360‑day priorities for 2026

For executive teams that must act this year, our recommended priorities — sequenced by urgency and impact — are:

- 0–90 days: complete a rapid certification gap analysis against the new performance standards and queue critical submissions; secure short‑term feedstock cover via toll‑blending or hedged contracts; and perform a customer segmentation audit to identify high‑margin retail and fleet accounts.

- 90–180 days: accelerate local blending or partnership negotiations in growth geographies where lead times and logistics materially affect cost‑to‑serve; implement product labeling and packaging changes aligned with recent enforcement guidance; and pilot bio‑blend stable formulations with select customers.

- 180–360 days: prioritize either bolt‑on acquisitions that add blending capacity and channel reach or targeted R&D investments for formulations that address multi‑fuel compatibility. Use the scenario model to validate CAPEX and integration payback assumptions before committing.

How incumbents, challengers and niche players should differentiate

- Incumbents: focus on defending premium channels via accelerated certification, performance guarantees, and bundled service offerings (testing, compliance, on‑site blending).

- Challengers and regional players: leverage local blending capability, faster lead times, and price sensitivity to undercut incumbents on service‑adjusted cost while selectively pursuing certification for high‑value accounts.

- Niche innovators: target aviation and specialty diesel pockets where unique chemistries or low‑dosage solutions command premium pricing and lower competitive intensity.

Closing — what you can expect from the full report

Our full Fuel Additives Market study contains the granular datasets and commercial matrices that convert the strategic directions outlined above into measurable project plans. That includes the regional and application split tables, supplier share matrices, product‑level pricing curves and downloadable models that allow you to test “what‑if” scenarios tailored to your balance sheet and risk appetite. Those segment‑level datasets and the interactive model are intentionally gated to preserve intellectual value and to provide a structured advisory engagement tailored to your priorities.

In a market growing at a mid‑single‑digit CAGR and shaped by concentrated supplier power, regulatory milestones and shifting fuel chemistry, the differentiator for profitable growth will be the ability to couple chemistry with commercial execution — fast. PW Consulting’s study is designed to convert that need for speed into a prioritized, executable plan for 2026. To access the full dataset, scenario models and tailored advisory services, visit the report page or contact the PW Consulting industry team for a briefing.

For detailed analysis of this topic, please visit the official page:Fuel Additives Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com