Low Molecular Weight Heparin Market: Strategic Outlook for 2026 Decision‑Makers

As PW Consulting’s Senior Strategic Advisor and Chief Industry Analyst, I present an executive briefing designed to orient corporate leadership, corporate development teams, and portfolio managers preparing for critical decisions in 2026. This briefing distills the practical strategic implications from our full Low Molecular Weight Heparin (LMWH) Market research (base year 2025; historical window 2020–2025; forecast 2026–2032), and explains why the study should be a foundational input to near‑term investment, manufacturing and regulatory plans.

Low Molecular Weight Heparin Market

Why LMWH matters in 2026

LMWH remains a core class within anticoagulant therapies, combining clinical utility across acute and chronic indications with persistent commercial complexity. At a macro level the market exhibited steady expansion from approximately USD 4.5 Billion in 2020 to roughly USD 5.73 Billion in 2025. Our forecast projects the market will continue to grow through the 2026–2032 forecast window at a compound annual growth rate (CAGR) of 6.6%, reaching an estimated USD 8.82 Billion by 2032 (revenues presented in USD, unit: Billion). These headline dynamics embed both demand resilience and structurally shifting supply‑side and regulatory pressures that will shape competitive returns.

Low Molecular Weight Heparin Market

What this means for 2026 corporate decisions

- Investment timing and scale: A mid‑single digit CAGR and a multi‑billion-dollar addressable market justify selective capacity additions and targeted M&A, but returns are contingent on regulatory positioning and supply security. Capital deployed without addressing API risk and biosimilar comparability will underperform.

- Regulatory strategy is a commercial moat: Enoxaparin and other LMWH agents are treated under biologic/biosimilar pathways by major regulators, which raises the bar for generic entrants. Demonstrable comparability and immunogenicity evidence remain decisive in market access and labeling outcomes; regulatory engagement plans need to be budgeted and sequenced early.

- Supply‑chain resilience as a profit lever: The traditional porcine mucosa supply chain remains vulnerable to inspection, trade and animal‑health disruptions. Firms that vertically integrate or secure diversified API sources will convert supply reliability into pricing and market share advantages.

- Reimbursement and access dynamics: European biosimilar entry is altering payer mixes and reimbursement levels; companies should model worst‑case reimbursement scenarios into 2026 P&L planning and design mitigations (e.g., service bundles, differentiated formulations, or label expansions).

Report components that operationalize strategy

The full PW Consulting report is intentionally practical. It translates market sizing and trends into executable deliverables for leadership and functional teams, including (but not limited to):

Low Molecular Weight Heparin Market

- Market sizing and growth framework (historical 2020–2025 and forecast 2026–2032) with scenario stress tests calibrated to supply interruptions and reimbursement shocks;

- Regulatory pathway mapping and comparator evidence requirements for biosimilar approvals across major jurisdictions;

- Supply‑chain risk register and API sourcing playbook, including alternative raw material pathways and contingency inventory strategies;

- Manufacturing cost and capacity model (API and finished dose), enabling ROI calculations for greenfield versus brownfield investments;

- Commercial go‑to‑market playbooks for originator, biosimilar/generic and differentiated specialty LMWH launches;

- Payer engagement templates and reimbursement sensitivity analyses to quantify access risk by scenario;

- Deal origination shortlist and valuation framework for M&A or strategic partnerships (anonymized targets with commercial and technical fit scores);

- Executive risk dashboard and 12‑ to 36‑month implementation roadmap aligned to board decision milestones.

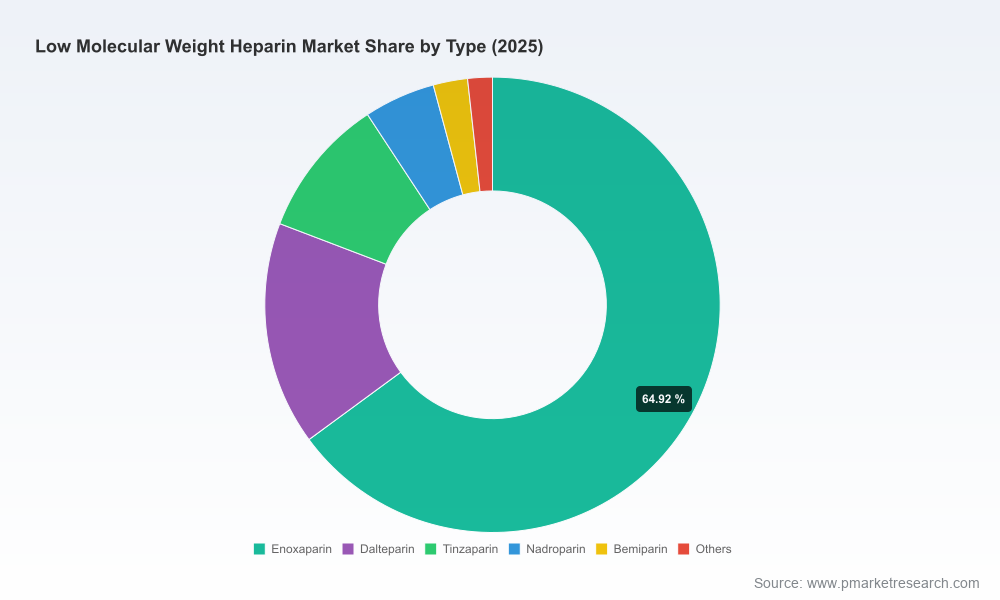

Note: This public briefing intentionally does not reproduce core segmented revenue tables (by region, product type or clinical application) — those detailed breakouts and workbook files are available exclusively in the paid report.

Competitive landscape — strategic implications

The market structure is characterized by a mix of originator brands, established multinational generics/biosimilar players and regional suppliers. Market concentration metrics indicate that the three largest participants do not monopolize the space; a broader set of five major firms captures a meaningful share, leaving room for challengers that execute strategically (market concentration: CR3 and CR5 metrics are incorporated into the report’s competitive assessment). From a decision‑maker’s perspective, several company archetypes and recent strategic moves matter:

- Originator brand custodians (e.g., Sanofi): Brand incumbency yields durable clinical recognition and pricing flexibility in markets where originator labels retain preference among prescribers. Maintaining clinical engagement and lifecycle label strategy is critical to defend margins post‑patent.

- Large multispecialty pharmas with label stewardship (e.g., Pfizer): Recent pediatric label expansions underscore how targeted label enhancements can expand addressable populations and create differentiation that is hard for new entrants to match quickly. Regulatory‑driven label advantages translate into measurable access gains.

- Generics and biosimilar entrants with integrated supply chains (e.g., Amphastar, Teva): Firms that control API and finished dose production can compete on cost and speed to market, but must invest in comparability data packages to clear regulatory gates. For biosimilars, the technical evidence package is a non‑trivial fixed cost that changes the economics of market entry.

- Regionally anchored manufacturers (e.g., Laboratorios Farmaceuticos ROVI, Changzhou Qianhong, Aspen, Opocrin): Localized capacity expansions and API investments strengthen regional supply resilience and create viable export platforms. These moves also create acquisition targets or partners for global players seeking scale quickly.

Recent industry developments that will shape 2026 outcomes

- Label evolutions: Expanded pediatric labeling for established agents demonstrates a pathway to grow volumes and extend product lifecycles—companies should prioritize clinical development programs and post‑market evidence generation that target similar label expansions.

- Manufacturing expansion: Multiple manufacturers have invested in additional sodium heparin and API lines. These capacity commitments reduce immediacy of shortages in some corridors but also increase competitive supply when biosimilars launch.

- Regulatory posture: Major regulators increasingly classify certain LMWHs under biologic/biosimilar frameworks, requiring head‑to‑head comparability and immunogenicity assurance. The implication is higher upfront development cost and longer time to monetization for non‑originator entrants.

- Supply assurance requirements: Regulatory agencies have conducted extensive batch reviews and intensified inspections of porcine‑sourced heparin supply. Buyers and investors should assume periodic inspection events and implement buffer strategies accordingly.

Strategic imperatives and near‑term action checklist for 2026

- Prioritize a supply diversification plan: Evaluate vertical integration, long‑term API supply contracts, and geographic redundancy. Run a 12‑month stress test scenario in which a key porcine supply corridor is disrupted.

- Invest in evidence generation tied to label differentiation: Allocate resources to targeted clinical or real‑world evidence projects that can unlock new indications or populations and justify premium positioning.

- Build regulatory capital early: For biosimilar strategies, budget for comprehensive comparability and immunogenicity programs and initiate structured dialogues with regulators to de‑risk approval timelines.

- Model reimbursement scenarios aggressively: Use worst‑case reimbursement inputs to size downside risk and structure launch pricing, tender participation and payer contracting accordingly.

- Pursue selective partnerships and bolt‑on assets: Identify regional manufacturers with complementary API capacity or regulatory footholds as high‑conviction inorganic targets.

- Protect margin via service differentiation: Where price competition is inevitable, layer value‑added services (e.g., hospital support programs, digital adherence tools) that are harder to replicate and can sustain pricing.

Closing guidance — why the full report is a 2026 planning imperative

LMWH is no longer a simple branded‑versus‑generic story. Clinical life‑cycle management, biosimilar technical barriers, API provenance and payer dynamics intersect to create a market where strategic missteps are costly and well‑timed moves are highly lucrative. Our research converts those intersections into executable plans: granular regulatory checklists, quantified supply‑chain contingency costs, manufacturability scorecards and a transaction playbook calibrated to today’s valuations.

For any leadership team allocating capital, structuring an M&A pipeline, or designing a European/Global market entry for LMWH products in 2026, the full PW Consulting study is the operational intelligence layer that converts market forecasts (2026–2032; CAGR 6.6%) into defensible commercial decisions. Access to the complete segmentation datasets, per‑jurisdiction regulatory requirements, supplier scorecards and the interactive financial model is available on our report page.

Contact PW Consulting for the report download and a tailored briefing workshop to translate insights into your 2026 investment and operating plan.

For detailed analysis of this topic, please visit the official page:Low Molecular Weight Heparin Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com