Middle East and Africa Sports Betting market Size, Share, Trends, Key Drivers, Demand and Opportunity Analysis

Other |

2026-05-19 14:15:47

As organizations recalibrate operations for a post‑pandemic, security‑first environment, public address (PA) systems have moved from a niche technical procurement to a strategic infrastructure decision. This briefing distills the strategic value of PW Consulting’s latest PA Systems Market study (base year 2025, forecast 2026–2032) for senior executives, product leaders, systems integrators, and investors planning moves in 2026.

PA Systems Market

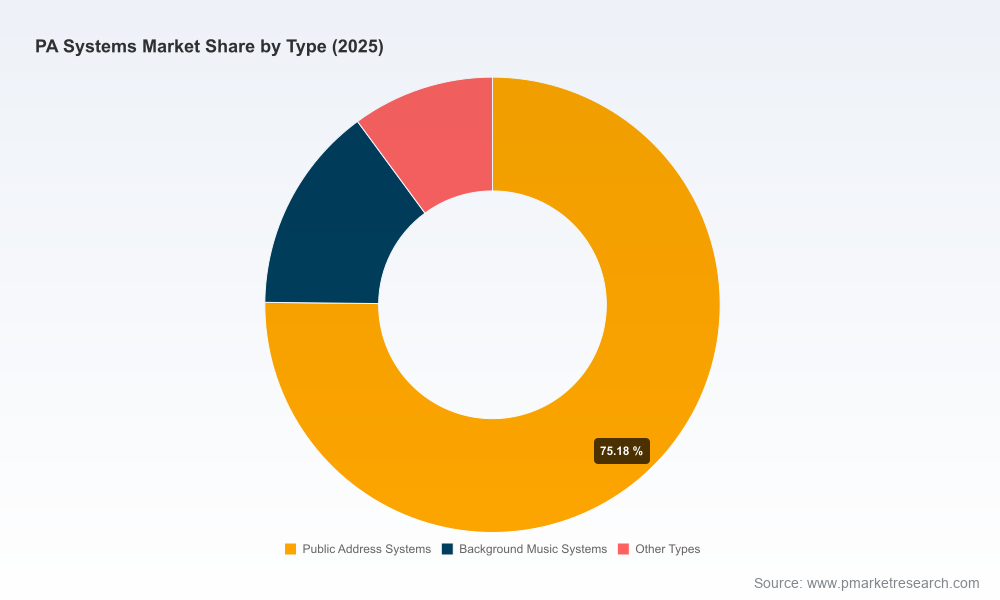

PA systems are now integral to safety, operations, and customer experience. Buyers demand solutions that simultaneously address voice evacuation, mass notification, background audio, and integration with building security and IP networks.

PA Systems Market

Market scale and trajectory provide a concrete planning envelope: the market expanded steadily from the early 2020s into 2025 and is projected to continue growing through 2032 at a projected CAGR of approximately 6.98% across the forecast period. PW Consulting quantifies this historical growth and the expected runway to 2032, providing the macro baseline needed for capacity, R&D, and M&A planning.

PA Systems Market

Concentration data indicates a fragmented supplier landscape (CR3 ~24.6%; CR5 ~26.2%), creating opportunities for mid‑market consolidation, vertical integration by integrators, and targeted product differentiation.

The report’s topline traces a steady expansion from the beginning of the decade into 2025, with projections showing sustained demand and a meaningful uplift through the end of the forecast horizon. For corporate planners, this is a clear signal: investment windows are open for product innovation, channel expansion, and scale play. The quantified forecast enables realistic scenario modeling—capacity sizing, break‑even analysis for new product lines, and revenue targets for strategic business units—without overreliance on anecdotal evidence.

Safety and compliance as a growth engine: Regulations and codes that govern voice evacuation and emergency communication are tightening in multiple jurisdictions. These mandates are raising baseline spend by public‑sector and commercial building owners, and drive preference for certified, auditable solutions. For vendors, certification roadmaps (EN 54‑16, NFPA‑aligned capabilities) should be prioritized in 2026 product roadmaps.

IP convergence and cybersecurity: Networked audio over IP is the default architecture for new installations. Buyers now demand not just audio fidelity but cybersecurity assurances—certifications and secure firmware update practices will be procurement gatekeepers in 2026. Vendors that can demonstrate FIPS and comparable credentials gain procurement advantage.

Integrator economics and channel shift: Systems integrators are consolidating roles—doing design, installation, commissioning, and managed services—shifting margin pools away from pure‑hardware suppliers toward hybrid service models. Manufacturers should evaluate service enablement and value‑added partner programs to protect downstream revenue.

Experience and operational use cases: Expect continued demand for solutions that blend emergency voice evacuation with routine communication and background music, delivered via flexible control software, cloud integration, and mobile operator interfaces. This trend privileges modular, software‑driven architectures in 2026 procurement decisions.

Modular IP audio platforms: Systems with open networking standards (Dante, AES67) and well documented APIs accelerate integrations with security, BMS, and unified comms platforms.

Edge processing and intelligibility analytics: On‑device speech processing that improves intelligibility in noisy environments reduces reliance on centralized compute and delivers measurable operational value—an attractive selling point for high‑noise venues.

Certifiable voice alarm (PAVA) stacks: For vendors targeting regulated building segments, design, test and certification workflows for EN 54‑16 and NFPA alignment must be baked into the 2026 product development lifecycle.

Managed services and software licensing: Recurring revenue models—cloud monitoring, health reporting, and predictive maintenance—change the economics of the installed base and create cross‑sell opportunities for integrators and manufacturers.

EN 54‑16 remains the mandatory European benchmark for voice evacuation PA systems; market access in many European public building segments requires compliance and traceable certification.

NFPA guidance (e.g., voice evacuation and speaker monitoring requirements) remains a design constraint in North America; compliance complexity increases the value of certified, pre‑tested system architectures for specifiers.

Cybersecurity expectations are formalizing. Certifications such as FIPS 140 and documented secure development practices reduce procurement friction for networked devices and should be included in product marketing and bid documentation.

The sector remains populated by a mix of OEMs focused on audio engineering, specialist safety solution providers, and global pro‑audio brands—each with distinct go‑to‑market approaches. Key players profiled in our study include:

TOA Electronics (Kobe, Japan) — a specialist manufacturer with strengths in IP‑based PA and intercom systems, offering a broad portfolio from amplifiers to stadium solutions. Their engineering heritage positions them strongly for integrated projects requiring system customization.

Axis Communications (Lund, Sweden) — provider of IP public address and network speakers with a security‑centric approach. Recent product activity expanded network audio design versatility (including Dante support and beam shaping) and reinforced their emphasis on cybersecurity best practices.

Guangzhou DSPPA Audio (Guangzhou, China) — a full‑line manufacturer with a focus on integrated voice alarm and PA products, appealing to large public procurement and OEM partnerships.

Valcom (United States) — a specialist in emergency paging and mass notification, strong in institutional channels such as schools and hospitals.

AFA Protective Systems (United States) — focused on custom design and installation for fire/life safety applications; their vertical integration into safety projects is a model for bundling services and hardware.

Zenitel (Norway) — known for PAVA systems compliant with EN 54‑16 and other safety certifications, targeting regulated building segments and transportation infrastructure.

JBL Professional (Harman, United States) and Yamaha Pro Audio (United States) — pro‑audio brands that bridge live sound and installed PA, recently updating portable and line‑array offerings to better serve event and mobile use cases.

Recent vendor moves (product announcements and updated product guides in late 2025 and early 2026) underscore a market pivot toward network audio flexibility, mobile‑friendly portable systems, and documentation that addresses buyer education—an important differentiator for vendors selling into less technical procurement channels.

For manufacturers: Prioritize certified voice‑alarm stacks, cybersecurity certifications, and modular IP architectures. Evaluate partnerships with system integrators to bundle services and secure recurring revenue streams.

For integrators and MSPs: Invest in cloud monitoring and managed‑service tooling to capture aftermarket revenue. Position expertise around compliance and testing to win specification‑led projects.

For institutional buyers (education, healthcare, transportation): Use standardized procurement specifications that demand compliance and cybersecurity evidence. Prioritize systems that reduce total cost of ownership through remote diagnostics and phased upgrades.

For investors and M&A teams: Fragmentation and mid‑market margins create opportunities for roll‑ups focused on regional integrators and niche OEMs with certification assets or software platforms that can be scaled across geographies.

Our full study is designed as an operational playbook for 2026 decision cycles. Highlights include:

Top‑down market sizing and growth scenarios calibrated to 2020–2025 history and a 2026–2032 forecast horizon, enabling rigorous financial planning and risk‑adjusted modelling.

Strategic segmentation frameworks (by product architecture, application profile, and channel) and buyer journey mapping that expose where margins and winning value propositions concentrate.

Competitive dossiers with capability matrices and capability gaps for leading vendors, plus real‑time monitoring of product launches, certifications and regulatory changes that matter in procurement cycles.

Playbooks for go‑to‑market, pricing strategies, partner programs, and technical certification roadmaps tailored to vendors, integrators and building owners.

Actionable M&A screening criteria and a curated list of acquisition targets based on capability adjacency, certification ownership, and service‑fit for roll‑up strategies.

Note: this briefing intentionally highlights directional insights and strategic implications while reserving detailed segment tables, regional splits, and vendor revenue breakdowns for the full report to preserve competitive integrity and provide subscribers with proprietary value.

In 2026, PA system decisions must be made at the intersection of safety compliance, networked architectures, and evolving business models. PW Consulting’s study provides the market magnitude, trend validation, and tactical playbooks to shape sensible product investments, channel strategies, and M&A moves. Use the modelled scenarios to stress test capital allocation, use the certification roadmaps to de‑risk procurement, and leverage the competitive dossiers to identify partnership or acquisition targets.

For teams preparing budgets, R&D prioritization, or transaction screens this year, the full report supplies the detailed segment metrics and executable templates you’ll need to convert insight into action. Contact the PW Consulting research desk or visit our report page to access the complete study and the underlying datasets.

For detailed analysis of this topic, please visit the official page:PA Systems Market

Lacy Lee

Senior Marketing Manager

[email protected]

00852-95632430

PW Consulting: www.pmarketresearch.com